Strategic Market Snapshot

Key Parameter | Report Details |

|---|---|

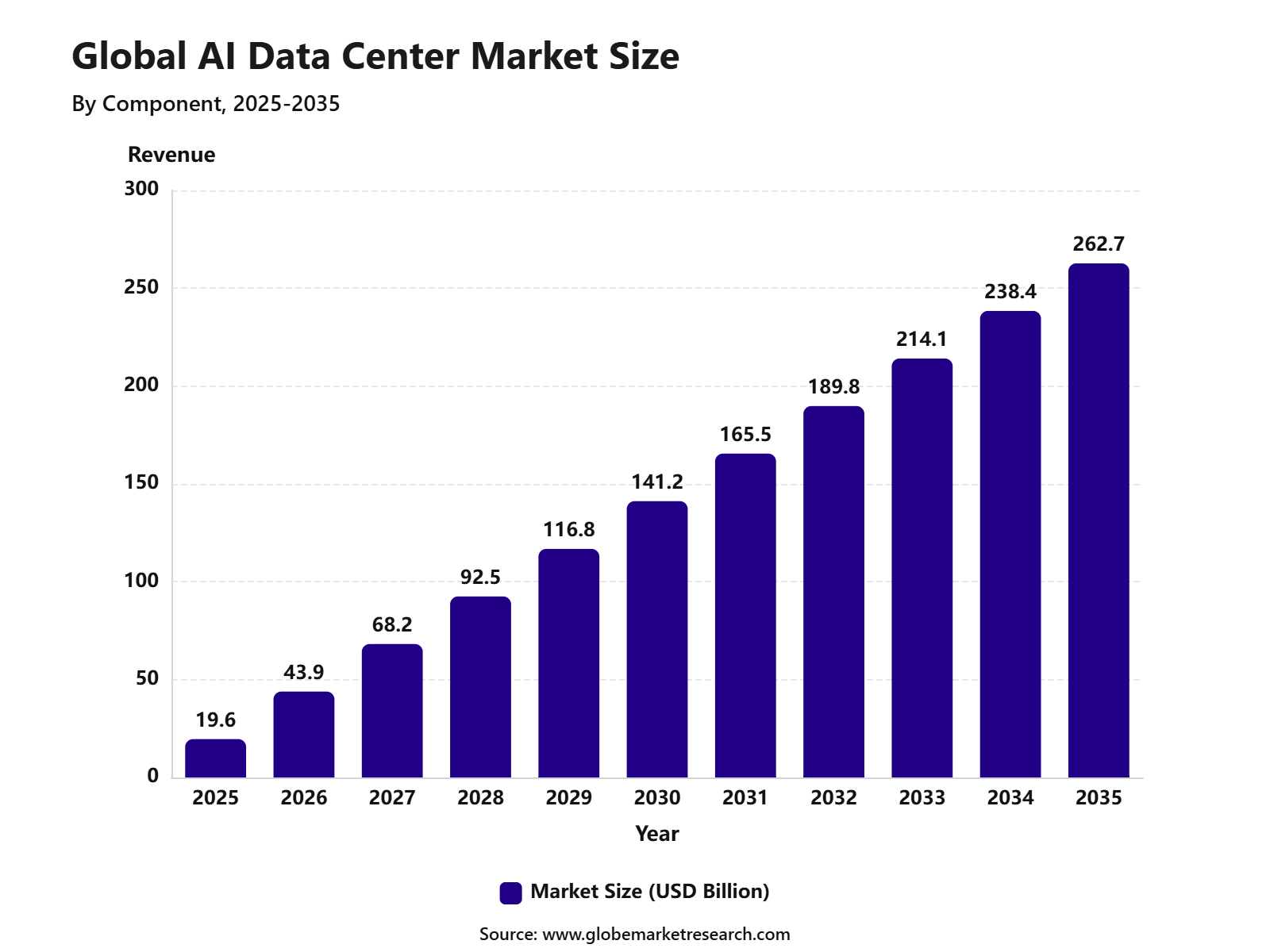

Market Revenue, 2025 | USD 19.6 Billion |

Projected Revenue, 2026 | USD 43.9 Billion |

Projected Revenue, 2035 | USD 262.7 Billion |

CAGR, 2025-2035 | 29.6% |

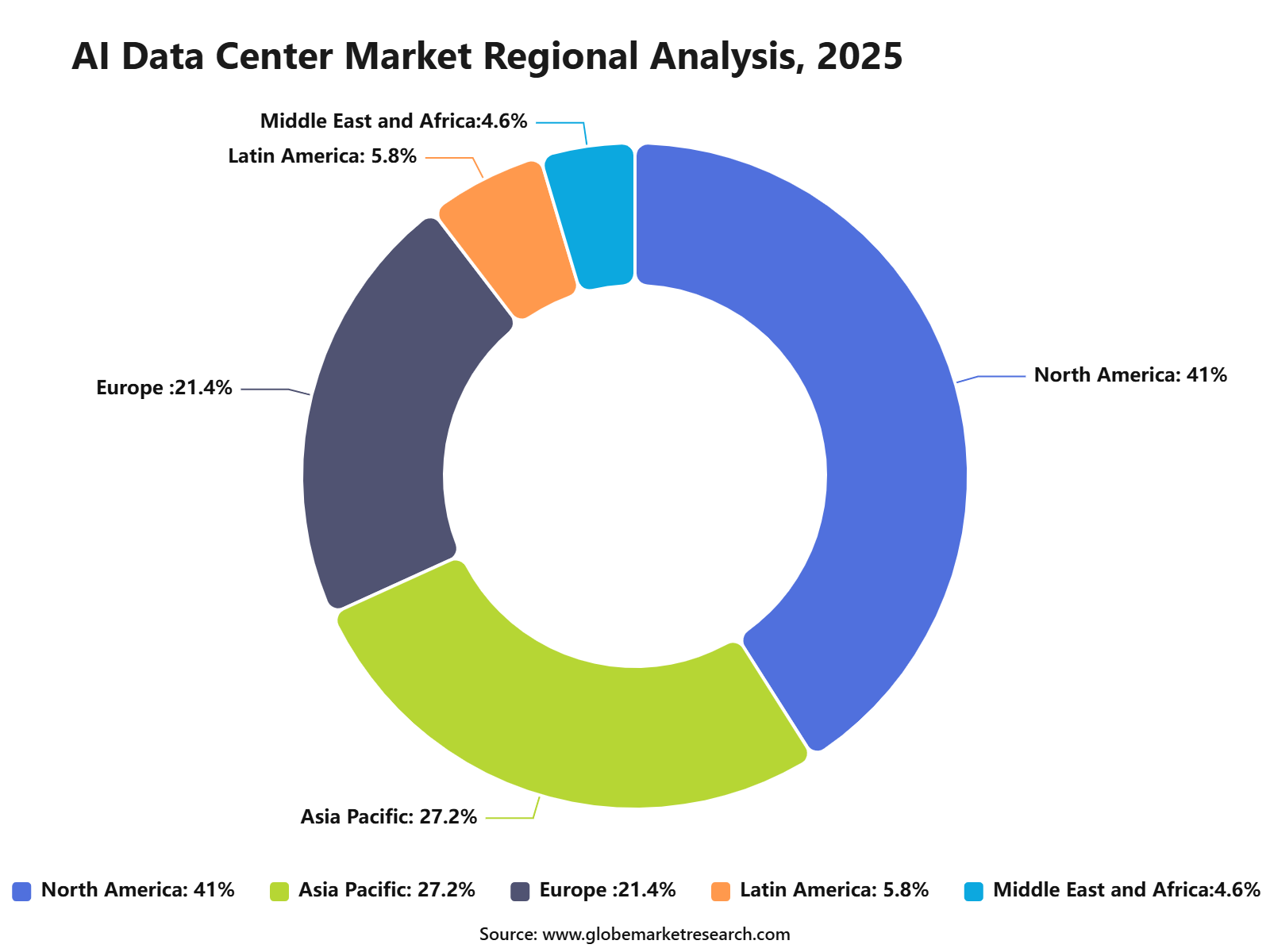

Largest Region | North America, 41.0% Share |

U.S. Market Revenue, 2025 | USD 6.3 Billion |

U.S. CAGR | 29.1% |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Market Overview

Based on findings published by Globe Market Research, the global AI data center market was valued at USD 19.6 billion in 2025 and is projected to grow from USD 24.8 billion in 2026 to USD 262.7 billion by 2035, registering a 29.6% CAGR from 2025 to 2035. North America led the market with 41% share in 2025, supported by strong hyperscale cloud infrastructure, high AI model training demand, advanced semiconductor access, and large-scale investments by technology companies.

AI data centers are specialized infrastructure facilities designed to support artificial intelligence workloads such as model training, inference, generative AI, high-performance computing, data processing, and enterprise AI applications. These facilities require GPUs, AI accelerators, high-density servers, storage systems, networking equipment, power systems, cooling infrastructure, and security architecture to handle large-scale compute demand.

The U.S. AI data center market was valued at USD 6.3 billion in 2025 and is projected to expand at a 29.1% CAGR from 2025 to 2035. Demand is being driven by AI model training, generative AI workloads, cloud AI services, enterprise automation, government workloads, financial institutions, healthcare companies, and large digital platforms.

Why the AI Data Center Market Is Growing

The growth of the AI data center market can be attributed to rising demand for generative AI training and inference workloads. This driver has an estimated positive impact of +3.4%, especially across North America, Europe, China, Japan, South Korea, and India. AI models require high-density compute, fast networking, large-scale storage, and advanced accelerators, which is increasing demand for AI-ready facilities.

Electricity demand is becoming one of the strongest external signals for market growth. The International Energy Agency projects that global electricity consumption from data centers will more than double to around 945 TWh by 2030, representing just under 3% of total global electricity consumption. AI is identified as the most important driver of this increase, alongside broader digital service demand.

Capacity demand is also visible in the North American data center market. CBRE reported that primary market supply reached a record 8,155 MW in H1 2025, up 43.4% year over year, while vacancy dropped to a record-low 1.6%. It also reported that 74.3% of under-construction capacity was already preleased, mainly by cloud and AI providers.

The market is therefore being shaped by three connected forces: AI compute demand, power availability, and capacity scarcity. Companies are not only buying data center space. They are securing megawatts, GPU access, cooling capacity, fiber connectivity, and future expansion rights.

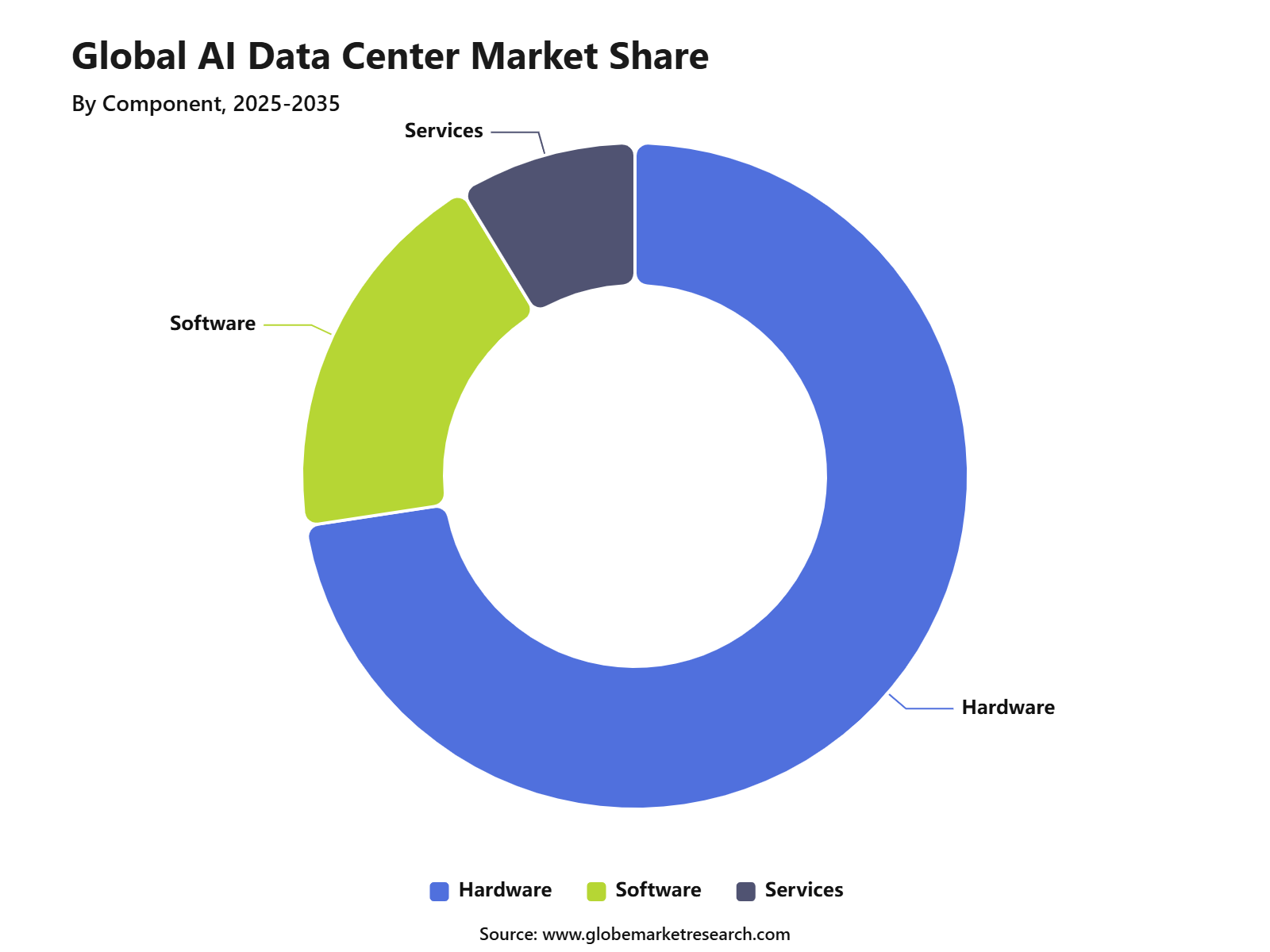

Hardware Leads the Component Segment

Hardware led the AI data center market with 72.6% share in 2025. Demand was supported by GPUs, AI accelerators, servers, storage systems, networking equipment, power distribution systems, cooling infrastructure, and security hardware. AI workloads need much higher compute density than traditional enterprise workloads, which keeps hardware as the largest spending area.

The strength of hardware demand is also visible in chip supplier revenue. NVIDIA reported record first-quarter fiscal 2027 revenue of USD 81.6 billion, up 85% year over year, while its data center revenue reached USD 75.2 billion, up 92% year over year. This shows how strongly AI infrastructure spending is flowing into GPUs, accelerators, networking, and server supply chains.

Hardware demand is expected to remain strong because model training and inference require continuous investment in faster chips, high-bandwidth memory, rack-scale systems, storage clusters, and liquid cooling. AI data center operators are also upgrading electrical systems and thermal management because rack power density is rising quickly.

Servers Remain the Leading Infrastructure Segment

Servers accounted for 41.8% share by infrastructure in 2025. AI servers are critical because they host GPUs, tensor processors, accelerators, memory, storage, and interconnects needed for model training, inference, analytics, and high-performance computing.

AI-ready servers are different from standard enterprise servers. They are built for dense GPU clusters, high-speed networking, advanced memory systems, efficient thermal control, and continuous workload performance. This is why server platforms from NVIDIA, Dell, HPE, Super Micro, Lenovo, and other vendors are becoming central to AI infrastructure planning.

Dell Technologies expanded its AI infrastructure portfolio in March 2026 through Dell AI Data Platform with NVIDIA, focused on data orchestration, storage performance, and enterprise AI workloads. HPE also introduced NVIDIA-powered AI infrastructure in March 2026, including servers, turnkey systems, services, and software designed for secure and scalable production AI.

The server segment will remain important because AI workload growth is still compute-constrained. Providers that can deliver high-density, energy-efficient, liquid-cooling-ready, and fast-deployable server infrastructure are likely to gain stronger demand.

Hyperscale Data Centers Lead by Data Center Type

Hyperscale data centers held 48.3% share in 2025. These facilities are designed for large cloud providers, AI model developers, technology platforms, and enterprises that need massive compute, storage, networking, and power capacity.

The hyperscale model is well suited to AI because training large models requires large clusters of accelerators working together. These facilities support high power density, automation, large-scale cooling systems, fast internal networking, and strong physical security. They also allow cloud providers to deliver AI infrastructure to enterprise customers through flexible service models.

Microsoft’s cloud results show how cloud AI demand is supporting this segment. In Q3 FY2026, Microsoft Cloud revenue reached USD 54.5 billion, up 29%, while Azure and other cloud services revenue increased 40%. Microsoft also stated that customer demand across workloads and geographies continued to exceed available capacity.

Hyperscale growth is expected to remain strong, but site selection is becoming more difficult. Power access, grid interconnection, cooling design, water availability, land approvals, and local regulation are now central to hyperscale development decisions.

Cloud-Based Deployment Holds the Largest Share

Cloud-based deployment accounted for 56.9% share in 2025. Cloud deployment is preferred because it allows companies to access AI compute, storage, model development tools, and inference infrastructure without building full private data centers.

This model is attractive for enterprises that need fast access to GPUs and managed AI platforms. Cloud-based AI data centers support model training, inference, analytics, automation, software development, and AI-as-a-service offerings. They also reduce upfront infrastructure burden for companies that do not want to own hardware directly.

Cloud demand is also being supported by generative AI applications across customer service, software development, marketing, legal operations, cybersecurity, search, and productivity tools. As more companies move AI pilots into production, cloud providers are expected to continue expanding AI-ready capacity.

However, cloud-based deployment does not remove all constraints. Capacity shortages, GPU availability, data sovereignty, cloud cost control, and latency remain important buyer concerns. This is creating demand for hybrid models that combine cloud scalability with private or colocated AI infrastructure.

Generative AI Leads the Technology Segment

Generative AI led the technology segment with 34.7% share in 2025. The segment is supported by large language models, image generation, code generation, enterprise copilots, synthetic data, search systems, AI agents, and automation tools.

Generative AI workloads are infrastructure-intensive because they require strong compute, fast storage, high-bandwidth networking, and advanced cooling. Training large models creates heavy cluster demand, while inference at scale creates continuous demand for low-latency processing and efficient serving infrastructure.

NVIDIA launched the Rubin platform in January 2026, describing it as a six-chip platform for next-generation AI supercomputing. The company later announced the Vera Rubin platform at GTC 2026, positioning it around agentic AI and large-scale AI factory infrastructure.

This trend shows that AI data center design is moving from general-purpose compute to full-stack AI factory architecture. Compute, networking, storage, security, memory, and cooling are being designed together to support larger and more complex AI systems.

AI Model Training Is the Leading Application

AI model training accounted for 38.5% share by application in 2025. Training large models requires very high compute power, large datasets, advanced accelerators, fast storage, and high-bandwidth networking. This segment is being driven by large language models, multimodal AI, scientific computing, recommendation engines, autonomous systems, enterprise-specific models, and domain-focused AI platforms.

Companies are investing in training infrastructure to improve model accuracy, business relevance, and competitive advantage. AI model training is expected to remain a high-value application because it supports the foundation of generative AI platforms. However, rising power consumption and hardware costs are forcing companies to improve training efficiency, model optimization, workload scheduling, and chip utilization.

Inference demand is also rising quickly as AI moves into daily business operations. Over time, the market is expected to become more balanced between training infrastructure and inference infrastructure, especially as AI agents, copilots, voice AI, and real-time applications scale.

IT and Telecommunications Lead End-Use Demand

IT and telecommunications led the end-use vertical with 32.4% share in 2025. Demand is being supported by cloud service expansion, network automation, cybersecurity, data traffic growth, edge AI deployment, and AI-powered enterprise services.

Telecom companies are using AI for network optimization, outage prediction, traffic management, fraud detection, and customer service automation. IT companies are using AI data centers to support software platforms, enterprise applications, cloud AI services, analytics, and managed AI infrastructure.

The segment is also closely linked with edge AI and low-latency applications. As telecom networks support connected devices, autonomous systems, industrial automation, and smart cities, more AI workloads are expected to move closer to users and devices.

BFSI, healthcare, retail, manufacturing, government, media, and energy are also expected to expand AI data center demand. These industries are moving from AI experimentation to production use cases that require reliable compute, security, compliance, and regional hosting.

North America Leads the AI Data Center Market

North America held 41% share of the AI data center market in 2025. The region benefits from major cloud providers, advanced colocation infrastructure, AI chip suppliers, enterprise AI adoption, and large-scale investments by technology companies.

The U.S. remains the main contributor because it has a strong base of hyperscale data centers, AI model developers, venture-backed AI companies, cloud platforms, and semiconductor ecosystem strength. The country is expected to remain a leading market as demand grows for advanced servers, liquid cooling, high-density racks, and reliable power systems.

Power availability is becoming a decisive factor in North America. The IEA states that the United States and China are expected to account for nearly 80% of global data center electricity consumption growth to 2030. In the U.S., data center electricity consumption is projected to increase by around 240 TWh from the 2024 level by 2030.

Asia Pacific is also becoming a major growth region as India, China, Japan, South Korea, Singapore, and Southeast Asia invest in cloud regions, sovereign AI, AI factories, and digital infrastructure. Meta’s June 2026 partnership with Reliance for an AI-enabled data center in Jamnagar, India, shows how global platforms are building capacity closer to large user bases.

Analyst Perspective

What Opportunities Are Emerging?

The biggest opportunity is in AI-ready colocation and hyperscale capacity. Cloud providers, AI companies, and enterprises need high-density space with confirmed power, cooling, connectivity, and deployment timelines.

Liquid cooling is another strong opportunity. As GPUs and accelerator clusters increase rack power density, traditional air cooling becomes less suitable for many AI workloads. Providers that offer direct-to-chip cooling, immersion cooling, and advanced heat management can gain stronger market relevance.

Energy-secured AI infrastructure is also becoming a major opportunity. Renewable power, microgrids, battery storage, on-site generation, and power purchase agreements will become more important as electricity demand grows and grid approvals become harder.

What Risks Should Companies Be Aware Of?

The main risk is power constraint. AI data center demand may grow faster than grid capacity, which can delay projects, raise energy costs, and increase local opposition.

Hardware supply risk is also important. GPU shortages, memory constraints, networking equipment delays, and transformer supply pressure can slow construction schedules and reduce revenue visibility.

Sustainability and permitting risks should also be managed carefully. AI data centers may face tighter rules around energy reporting, water use, emissions, land use, noise, and community impact.

What Decisions Should Clients Make Next?

Clients should first decide whether they need cloud AI capacity, AI-ready colocation, private AI infrastructure, or a hybrid model. The right choice depends on workload sensitivity, capital budget, latency, data sovereignty, security, and scale.

Second, clients should evaluate power strategy before site selection. Grid access, utility timelines, renewable procurement, cooling water availability, backup power, and expansion rights should be reviewed before committing capital.

Finally, clients should select partners based on deployment speed, power availability, cooling readiness, GPU ecosystem access, cybersecurity, compliance, and long-term service capability. In this market, available megawatts and operational reliability may matter as much as real estate location.

Recent Developments

In January 2026, NVIDIA launched the Rubin platform, a six-chip architecture designed to support next-generation AI supercomputers and large-scale AI data center infrastructure. The platform was positioned around building, deploying, and securing large AI systems more efficiently.

In March 2026, Dell Technologies expanded Dell AI Data Platform with NVIDIA, adding data orchestration and storage innovations for enterprise AI and demanding agentic AI workloads. This supports the broader shift toward integrated AI infrastructure stacks.

In March 2026, HPE introduced new AI infrastructure with NVIDIA, including servers, turnkey systems, services, and software powered by NVIDIA Blackwell and Rubin acceleration. The launch focused on secure, scalable, production-ready AI deployments.

In June 2026, Meta partnered with Reliance Industries for an AI-enabled data center in Jamnagar, India. Reliance said it would develop a 168 MW facility within two years, with an option to scale, while Meta described the project as part of its global infrastructure expansion.

Competitive Landscape

The AI data center market is highly competitive, with semiconductor companies, server manufacturers, cloud providers, networking vendors, colocation operators, power management companies, cooling specialists, and digital infrastructure providers competing across the value chain.

Competition is expected to increase as AI workloads require tighter integration between chips, servers, networking, storage, cooling, power, cloud platforms, and security. Semiconductor companies are moving deeper into rack-scale systems, while cloud and colocation providers are securing power and land for future AI capacity.

Top Key Companies

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Broadcom Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise Company

Super Micro Computer, Inc.

Cisco Systems, Inc.

Arista Networks, Inc.

Juniper Networks, Inc.

Lenovo Group Limited

IBM Corporation

Oracle Corporation

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

Meta Platforms, Inc.

Equinix, Inc.

Digital Realty Trust, Inc.

NTT Global Data Centers

Schneider Electric SE

Vertiv Holdings Co.

Eaton Corporation plc

ABB Ltd.

Legrand SA

Johnson Controls International plc

Fujitsu Limited

Huawei Technologies Co., Ltd.

NEC Corporation

Siemens AG

The strongest providers will be those that can combine compute performance with deployment reliability. Buyers will prioritize GPU availability, power access, liquid cooling readiness, security, uptime, and the ability to scale AI workloads without long delays.

Market leadership will not be decided by hardware alone. Companies that can deliver full-stack AI infrastructure, including chips, servers, networking, cooling, power systems, cloud platforms, and managed services, are expected to gain stronger long-term positioning.

Conclusion

The AI data center market is entering a strong growth phase as generative AI, AI model training, inference, cloud AI services, and enterprise AI adoption increase demand for high-density infrastructure. Growth is being supported by hardware investment, GPU servers, hyperscale capacity, cloud-based deployment, generative AI workloads, and North American infrastructure expansion.

Future growth will be led by AI-ready hardware, servers, hyperscale data centers, cloud AI infrastructure, liquid cooling, renewable power integration, GPU-ready colocation, and edge AI data centers. The outlook remains positive, but success will depend on power availability, cooling design, chip supply, capital access, cybersecurity, and regulatory readiness.

Explore Information and Technology Trending Reports Here: https://www.globemarketresearch.com/industry/information-and-technology