Strategic Market Snapshot

Key Parameter | Report Details |

|---|---|

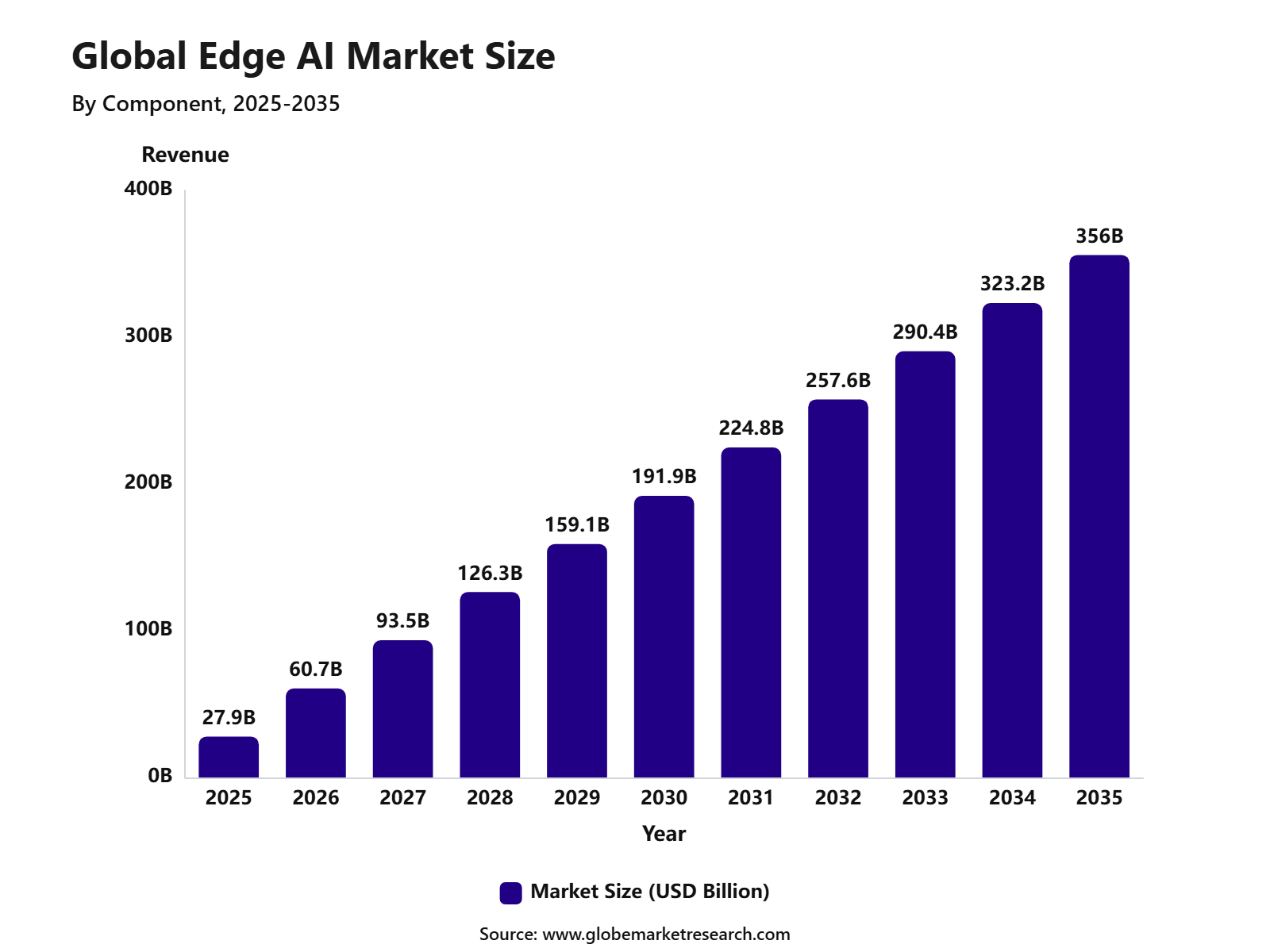

Market Revenue, 2025 | USD 27.9 Billion |

Projected Revenue, 2035 | USD 356.0 Billion |

CAGR, 2025-2035 | 29.0% |

Largest Region | North America, 40.0% Share |

U.S. Market Revenue, 2025 | USD 8.5 Billion |

U.S. CAGR | 28.5% |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Market Overview

According to Globe Market Research, the global Edge AI Market was valued at USD 27.9 billion in 2025 and is projected to reach USD 356 billion by 2035, growing at a 29% CAGR. North America accounted for around 40% share in 2025, supported by advanced AI infrastructure, semiconductor innovation, connected device adoption, edge computing platforms, and enterprise demand for low-latency intelligence.

Edge AI refers to the use of artificial intelligence directly on local devices such as smartphones, cameras, robots, wearables, smart sensors, vehicles, and industrial machines. Instead of sending all data to the cloud, Edge AI allows devices to process data closer to where it is created. This improves speed, privacy, reliability, and real-time decision-making.

The U.S. Edge AI Market was valued at approximately USD 8.5 billion in 2025 and is projected to grow at a 28.5% CAGR from 2025 to 2035. Growth is being supported by AI-enabled cameras, smart factories, autonomous vehicles, healthcare devices, retail analytics, surveillance systems, edge servers, and connected infrastructure.

Why is Edge AI Market Growing?

The growth of the Edge AI market can be attributed to rising demand for real-time AI processing, lower cloud dependency, stronger data privacy, and faster decisions at the device level. Rising demand for real-time AI processing has an estimated positive impact of +3.8%, while connected devices and IoT networks add +3.4% to market growth.

5G adoption is also supporting Edge AI deployment. Ericsson reported that global 5G subscriptions passed 3 billion in 2026, while 5G handled 48% of global mobile data traffic at the end of 2025 and is expected to carry 85% by 2031. This creates a stronger base for low-latency AI use cases in smart cities, vehicles, factories, healthcare, and connected consumer devices.

Industrial automation is another major driver. The International Federation of Robotics reported that 542,000 industrial robots were installed worldwide in 2024, with annual installations staying above 500,000 units for the fourth consecutive year. Asia accounted for 74% of new deployments, showing strong automation demand where Edge AI can support machine vision, defect detection, robot guidance, and predictive maintenance.

Enterprise AI adoption is creating a wider customer base. U.S. Census data from December 2025 to May 2026 showed overall business AI use between 17% and 20%, while 37% of firms with at least 250 employees reported using AI in business operations. This indicates stronger near-term adoption potential among large manufacturers, retailers, healthcare providers, telecom firms, automotive companies, and logistics operators.

Hardware Leads the Component Segment

Hardware led the Edge AI market with 56.8% share in 2025. This segment includes AI chips, processors, neural processing units, sensors, cameras, edge accelerators, embedded modules, and gateways that allow AI models to run locally on devices.

Hardware demand is being supported by smartphones, smart cameras, robots, wearables, vehicles, industrial machines, and connected consumer devices. These products need faster processing, lower power consumption, and local intelligence to support image recognition, voice control, security, navigation, and predictive maintenance.

AI chip innovation is becoming central to this segment. Edge devices require processors that can run AI models with low latency and lower energy use. This is why companies are investing in compact AI accelerators, embedded AI platforms, and efficient inference chips for industrial, automotive, healthcare, and consumer electronics applications.

Smartphones Hold the Largest Device Type Share

Smartphones accounted for 34.6% share of the Edge AI market in 2025. The segment is supported by on-device AI features such as camera enhancement, voice assistance, translation, biometric security, personalization, battery optimization, and generative AI functions.

Smartphones are important because they offer a high-volume route for Edge AI adoption. Consumers increasingly expect faster response, better privacy, offline AI capability, and real-time personalization. Processing more AI tasks on the device can reduce cloud dependency and improve user experience.

The opportunity is also expanding into wearables and smart sensors. Edge AI can help watches, earbuds, fitness bands, health monitors, and home devices process voice, movement, biometric, and environmental data locally. This supports better responsiveness and stronger privacy for consumer-facing AI products.

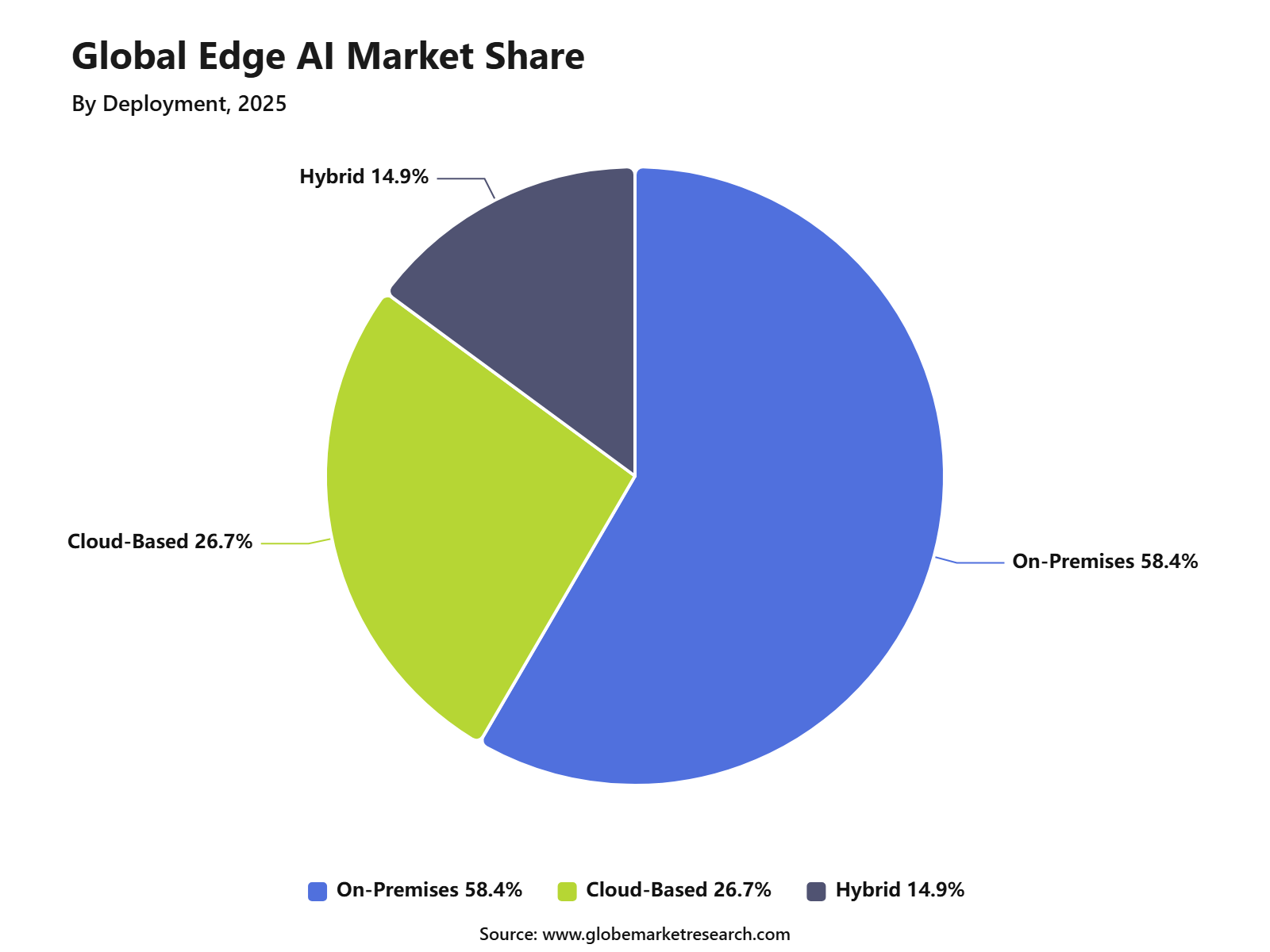

On-Premises Deployment Leads Due to Data Control

On-premises deployment held the largest share at 58.4% in 2025. Enterprises prefer this model because sensitive data from cameras, machines, sensors, vehicles, and connected devices can be processed locally without depending fully on external cloud systems.

This deployment model is important for manufacturing, healthcare, banking, automotive, retail, defense, and smart infrastructure. In these sectors, latency, data privacy, security, uptime, and compliance are critical. Local processing allows faster decisions and reduces the risk of sending sensitive operational data across networks.

Cloud and hybrid deployment will still grow, especially where model training, analytics, dashboards, and fleet management are needed. However, Edge AI adoption will remain strongest where local control, real-time response, and data sovereignty are clear business requirements.

Machine Learning Leads by Technology

Machine learning represented 39.7% share of the Edge AI market in 2025. It is widely used in predictive analytics, object detection, speech recognition, anomaly detection, quality inspection, and automated decision-making.

Machine learning is important because edge devices must act quickly on real-world signals. A smart camera may need to detect an object instantly. A robot may need to adjust movement in real time. A healthcare device may need to identify abnormal readings without waiting for cloud processing.

Computer vision, natural language processing, and generative AI are also gaining relevance. Computer vision is used in surveillance, retail analytics, quality inspection, autonomous vehicles, and healthcare imaging. Natural language processing supports on-device voice assistants and translation. Generative AI is expected to support local content creation, summaries, copilots, and personal assistants as device chips become more powerful.

Consumer Electronics Remain the Leading End-Use Industry

Consumer electronics accounted for 27.9% share, making it the leading end-use industry in the Edge AI market. Demand is being supported by AI-enabled smartphones, smart speakers, wearables, laptops, smart home cameras, televisions, appliances, and connected home devices.

Consumers want devices that respond faster, protect privacy, and deliver personalized features without constant cloud access. Edge AI supports real-time photo enhancement, voice control, gesture recognition, security alerts, health tracking, and smart home automation.

The commercial opportunity is strong because consumer electronics companies can use Edge AI as a product differentiator. Better camera intelligence, on-device voice AI, private personalization, and offline AI features can improve user experience and support premium device positioning.

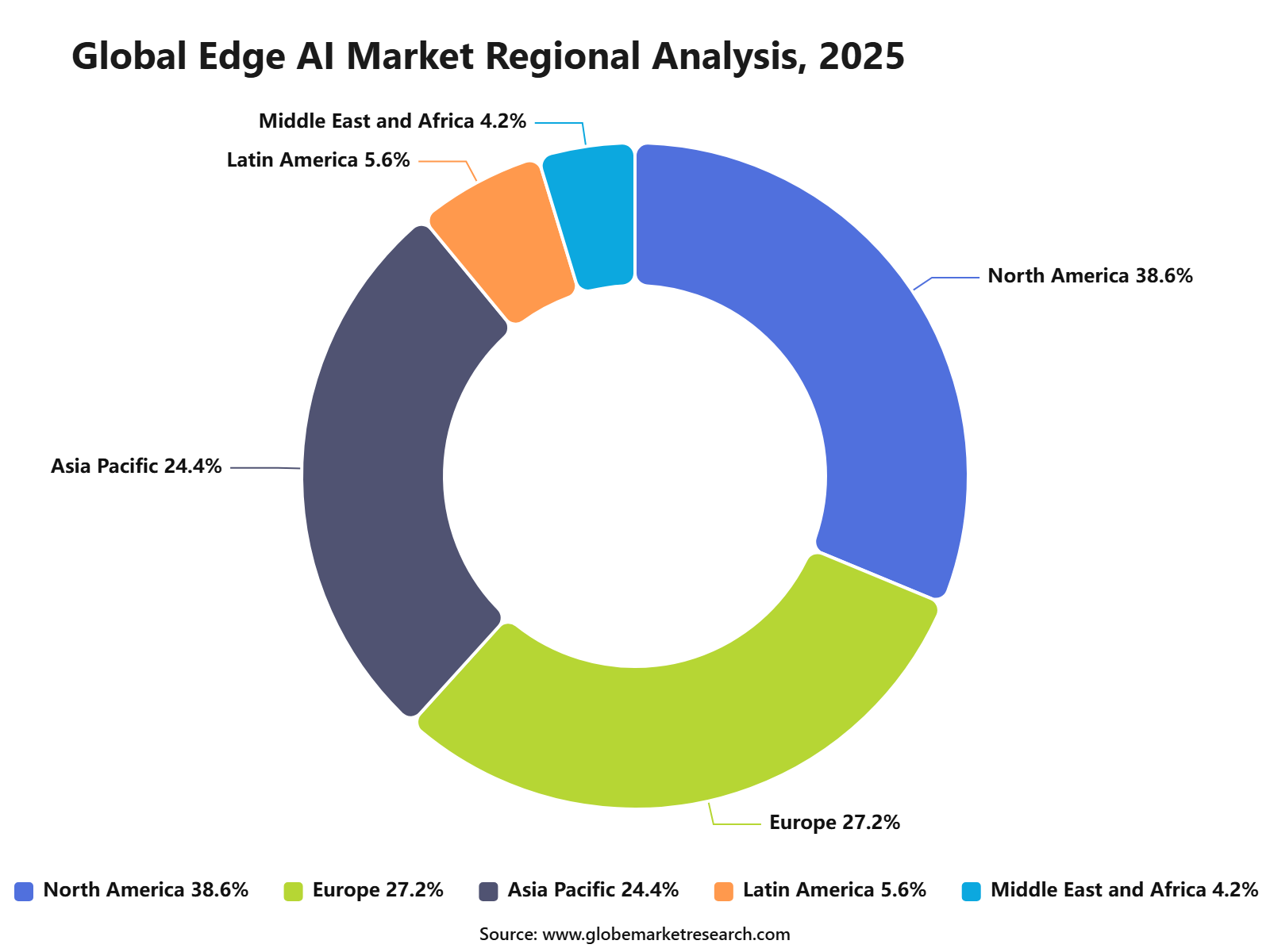

North America Leads the Edge AI Market

North America led the Edge AI market with 38.6% share in 2025. The region benefits from strong AI infrastructure, advanced semiconductor development, high connected device adoption, cloud-edge platforms, and early enterprise use of edge computing.

The U.S. remains the key contributor due to its strong technology ecosystem, AI hardware companies, cloud providers, enterprise software firms, and industrial automation demand. The U.S. Edge AI market reached about USD 8.5 billion in 2025, supported by manufacturing, automotive, healthcare, retail, surveillance, and smart infrastructure use cases.

Asia Pacific is also an important growth region due to strong electronics manufacturing, robotics adoption, smartphone production, smart city projects, and industrial automation. China, South Korea, Japan, India, and Southeast Asia are expected to remain important markets for edge AI chips, cameras, sensors, and connected devices.

Risk Factors and Market Barriers

The largest restraint is the high cost of AI chips and edge hardware, with an estimated negative impact of -2.6%. This can slow adoption among smaller enterprises, price-sensitive manufacturers, and emerging markets where upfront device cost remains a barrier.

Limited processing power in small edge devices is another barrier, with an estimated negative impact of -2.2%. Compact devices such as wearables, sensors, cameras, and battery-powered systems may struggle to run advanced AI models without affecting energy use, heat, or performance.

Integration complexity with existing systems has an estimated negative impact of -2.0%. Many enterprises operate older machines, fragmented software, legacy cameras, separate data systems, and mixed hardware platforms. This can increase deployment cost and slow large-scale implementation.

Cybersecurity risk is also important because Edge AI expands the number of distributed endpoints. If smart cameras, gateways, industrial robots, or connected vehicles are not properly protected, attackers may target device identities, models, data flows, or software updates.

Analyst Perspective

What Opportunities Are Emerging?

The biggest opportunity is in AI-enabled devices. Smartphones, wearables, smart cameras, robots, sensors, and connected vehicles need local AI processing to deliver faster and more private user experiences.

Industrial automation is another strong opportunity. Edge AI can help manufacturers improve quality inspection, predictive maintenance, safety monitoring, robotics, and real-time production analytics.

Healthcare, smart cities, retail analytics, and autonomous systems are also emerging as high-value areas. These sectors need local intelligence because cloud-only AI can create latency, bandwidth, privacy, or reliability issues.

What Risks Should Companies Be Aware Of?

The main risk is hardware cost. AI chips, edge accelerators, cameras, gateways, and embedded modules can increase project costs, especially in smaller companies and price-sensitive regions.

Power and performance limits are also important. Edge AI systems must balance model accuracy with low energy use, heat control, and device size. This challenge has an estimated negative impact of -2.4%.

Security risk should also be watched carefully. Edge AI creates many distributed endpoints, and each device can become a possible attack point if identity, encryption, access control, and update management are weak.

What Decisions Should Clients Make Next?

Clients should first identify where real-time local processing creates measurable value. The best starting points are video analytics, predictive maintenance, smart cameras, industrial inspection, connected vehicles, healthcare monitoring, and retail operations.

Second, companies should decide whether on-premises, cloud-based, or hybrid deployment is best suited to their data and latency needs. Regulated and mission-critical use cases may need stronger local control, while broad analytics may still benefit from cloud support.

Finally, clients should select vendors based on hardware performance, software integration, cybersecurity controls, model update support, energy efficiency, and industry experience. The best Edge AI partners should reduce operational friction while improving speed, privacy, and reliability.

Recent Developments

In March 2026, Advanced Micro Devices expanded its Ryzen AI Embedded P100 Series for edge AI applications. The platform offers up to 80 TOPS and ROCm support for industrial, robotics, and embedded AI systems.

In April 2026, Google updated its Gemini Nano developer documentation for Android on-device AI. Gemini Nano runs through Android’s AICore system service and uses device hardware to support low-latency inference on compatible Android devices.

In March 2025, Samsung showcased its mobile AI strategy at MWC 2025, covering Galaxy AI, the Galaxy S25 series, new Galaxy A devices, software-centric networks, and Project Moohan. The company positioned on-device AI as a core feature across smartphones, tablets, wearables, and connected devices.

In January 2025, Cisco launched AI Defense to help enterprises secure AI applications across development, deployment, and runtime environments. The solution supports Edge AI adoption by addressing visibility, validation, model protection, and security risks as AI moves closer to enterprise networks and connected devices.

Competitive Landscape

The Edge AI market is competitive, with semiconductor companies, cloud providers, AI software firms, device makers, networking companies, and industrial automation providers competing across hardware, software, platforms, and services. Key companies include:

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Qualcomm Incorporated

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

IBM Corporation

Cisco Systems, Inc.

Samsung Electronics Co., Ltd.

Other Key Players

Competition is expected to increase as AI moves from centralized cloud systems to distributed devices. Companies are competing on AI chip efficiency, inference performance, device compatibility, cybersecurity, developer tools, cloud-edge integration, and ecosystem partnerships.

The strongest providers will be those that combine efficient hardware with reliable software, model lifecycle management, security, and integration support. In this market, performance alone will not be enough. Buyers will also expect energy efficiency, deployment support, compliance readiness, and long-term device management.

Conclusion

The Edge AI market is entering a strong growth phase as AI moves closer to devices, machines, cameras, vehicles, sensors, and connected infrastructure. Growth is being supported by real-time AI processing, 5G networks, industrial automation, AI-enabled consumer electronics, privacy needs, and reduced cloud dependency.

Future growth will be led by edge AI hardware, smartphones, on-premises deployment, machine learning, consumer electronics, smart cameras, autonomous vehicles, healthcare diagnostics, and industrial edge systems. Companies that combine speed, privacy, security, energy efficiency, and reliable integration will be better positioned in this market.