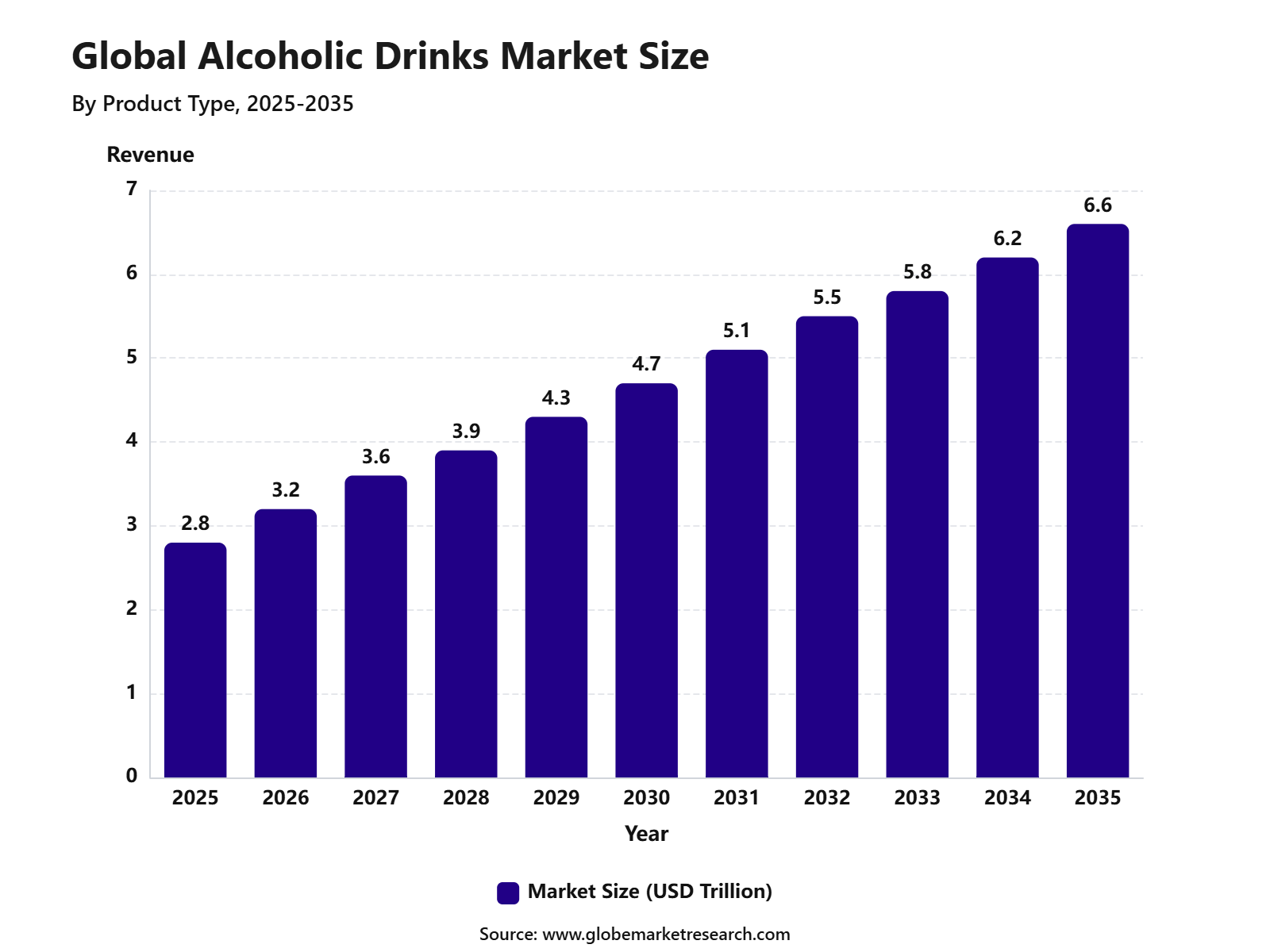

Revenue, 2025

$ 2.8 Tn

Forecast, 2035

$ 6.6 Tn

CAGR, 2025-2035

8.9%

Report Coverage

Global

Market Size and Forecast

The Global Alcoholic Drinks Market was valued at USD 2.8 trillion in 2025 and is projected to reach USD 6.6 trillion by 2035, growing at a CAGR of 8.9% from 2025 to 2035. The market growth can be attributed to rising consumer spending on premium alcoholic beverages, expanding social drinking culture, growth in flavored and craft alcohol products, and increasing demand across emerging economies.

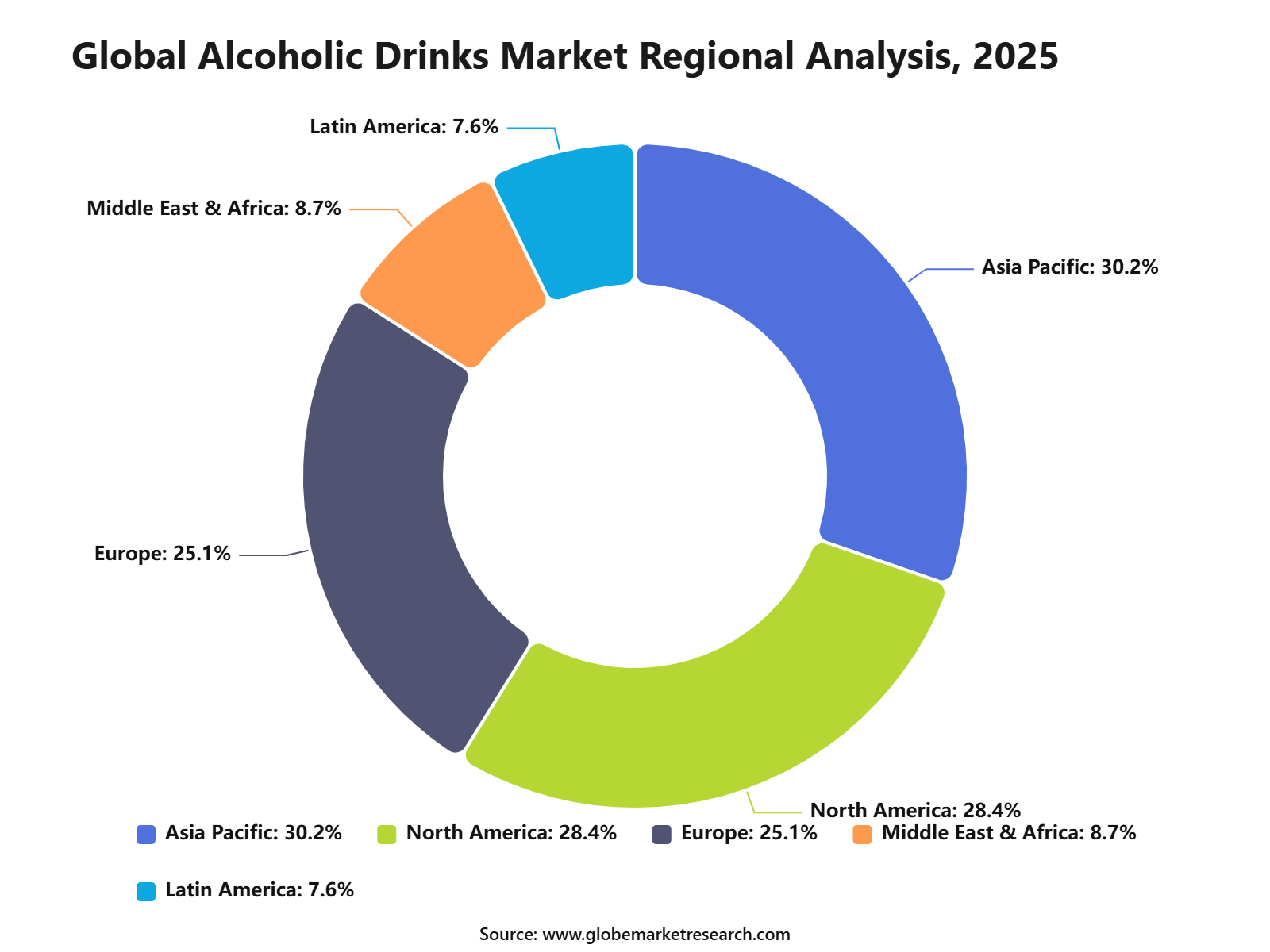

Asia Pacific held the largest regional share of 30.2% in 2025, valued at approximately USD 0.85 trillion. The region’s dominance can be linked to its large consumer base, rising disposable income, rapid urbanization, and strong demand for beer, spirits, wine, and ready-to-drink alcoholic beverages across countries such as China, India, Japan, South Korea, and Southeast Asian markets.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Beer led the product type segment with 45.8% share, supported by wide consumer acceptance, strong availability, affordable pricing, and high consumption across social and recreational occasions.

Male consumers accounted for 73.9% share by end user, driven by higher consumption frequency, brand loyalty, and strong demand across beer, spirits, and premium alcoholic beverages.

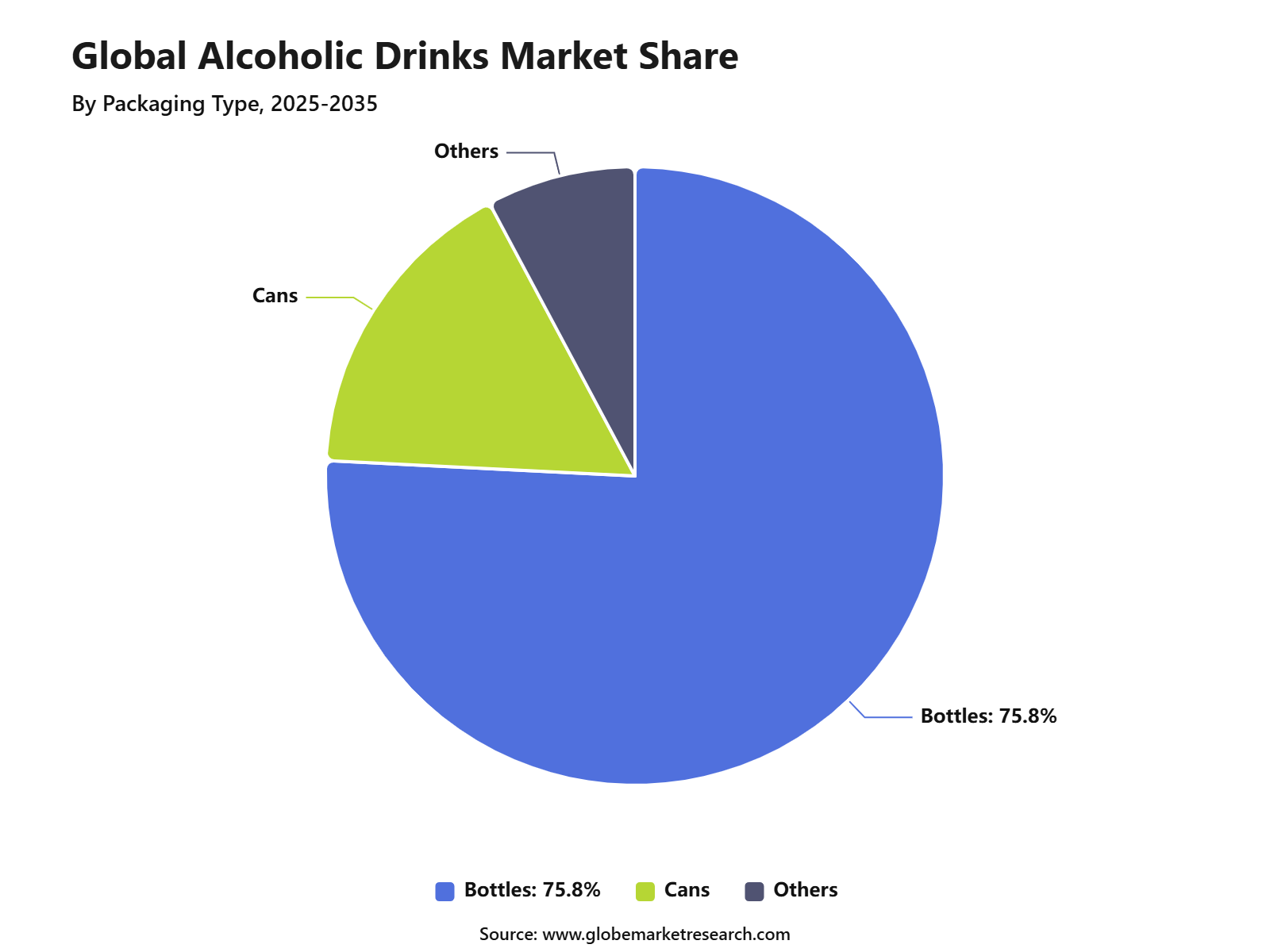

Bottles dominated the packaging type segment with 75.8% share, supported by product safety, longer shelf life, premium presentation, and strong use across beer, wine, and spirits.

On-trade channels held 52.1% share, driven by strong sales through bars, restaurants, pubs, hotels, clubs, and event venues.

Asia Pacific accounted for 30.2% share of the alcoholic drinks market, supported by large consumer populations, rising disposable income, urban nightlife growth, and expanding premium beverage demand.

Go-to-Market and Sales Economics

The Alcoholic Drinks Market needs a category-led and occasion-led go-to-market strategy. Brands should position beer, wine, spirits, cider, ready-to-drink cocktails, premium drinks, craft beverages, low-alcohol products, and alcohol-free alternatives according to consumer occasion, price point, retail channel, and regulation. In the U.S., spirits supplier sales reached USD 36.4 billion in 2025, down 2.2%, while volumes increased 1.9% to 318.1 million 9-liter cases. This shows that value pressure remains present, even where consumption volume is more stable.

Sales economics are strongest when brands combine distribution reach with premium packaging, brand trust, on-trade visibility, retail shelf space, and repeat purchase. Beer remains highly volume-driven, while spirits and wine often depend more on brand image, gifting, premiumization, and hospitality placement. In 2025, overall U.S. beer production and imports declined 5.7%, while craft brewer volume sales declined 4%, showing that beer suppliers need stronger channel planning, pricing discipline, and product innovation to protect profitability.

Risk Factors & Market Barriers

The main risk factor is changing consumer behavior. Younger consumers are drinking more selectively, health awareness is rising, and consumers are comparing alcohol with low-alcohol, alcohol-free, functional, and premium non-alcoholic beverages. Global wine shows this pressure clearly, as OIV estimated 2025 world wine consumption at 208 million hectolitres, down 2.7% from 2024 and the lowest level since 1957.

Cost pressure is another major barrier. Alcohol companies face higher costs for packaging, glass, aluminum, energy, freight, labor, compliance, and imported inputs. Beer and craft alcohol businesses are especially exposed because they often operate with high fixed costs and local distribution limits. Brewers Association data showed total craft production of 22,034,000 barrels in 2025, down 4%, with 60% of breweries reporting declines, which highlights the pressure on smaller producers.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across beer, wine, spirits, cider, ready-to-drink cocktails, hard seltzers, premium spirits, craft beverages, duty-free retail, restaurants, bars, hotels, events, e-commerce, and direct-to-consumer channels where allowed. Spirits remain attractive where brands can use premium packaging, cocktail culture, gifting, and controlled distribution to protect value. Wine remains important in restaurants, tourism, gifting, and premium retail, although volume demand is under pressure.

Ready-to-drink formats and moderation-led products are becoming more relevant because they match convenience, portion control, and younger consumer preferences. NielsenIQ reported that beverage alcohol remained under pressure in 2025, with dollar declines across beer, wine, and spirits mainly due to volume softness, while RTDs remained one of the more reliable growth engines and accounted for over 12% of total alcohol dollars. This shows that revenue growth is shifting toward convenience-led formats rather than only traditional bottles.

Financial Impact

The financial impact can be positive for companies with strong brands, efficient distribution, diversified categories, and pricing power. Premium spirits, cocktail-ready products, RTDs, gifting packs, and hospitality-linked sales can support better margins than undifferentiated low-price products. However, weak volume trends mean that companies must control promotional spending, inventory, working capital, and route-to-market costs carefully.

Financial risk remains linked to tariffs, excise taxes, health regulation, volume decline, packaging cost, and changing consumer preferences. Diageo warned in 2025 of an annual tariff impact of USD 200 million, up from an earlier estimate of USD 150 million, while also expanding its cost-saving target to USD 625 million. The strongest financial resilience is expected from alcohol companies that diversify across categories, manage tariff exposure, invest in compliant marketing, and build premium and moderation-led products without depending only on volume growth.

Product Type Analysis

Beer led the Alcoholic Drinks Market with 45.8% share, supported by its wide consumer base, lower alcohol content compared with spirits, broad price availability, and strong presence across retail and on-trade channels. Beer remains one of the most consumed alcoholic beverage categories due to its use in social occasions, sporting events, restaurants, bars, festivals, and casual drinking occasions. The growth of this segment can be attributed to product variety, including lager, ale, craft beer, flavored beer, premium beer, and low-alcohol beer.

Brewers are also focusing on packaging innovation, regional flavors, and premium product lines to attract younger consumers and urban drinkers. Beer is expected to maintain its leading position as brands expand into premium, craft, and no-alcohol or low-alcohol variants. However, moderation trends, higher excise duties, and public health regulations may influence category growth in some mature and regulated markets.

End User Analysis

Male consumers accounted for 73.9% share of the Alcoholic Drinks Market, supported by higher consumption frequency across beer, spirits, and on-trade drinking occasions. Male consumers remain a key target group for alcoholic beverage brands due to strong participation in social drinking, sports-linked promotions, nightlife, and premium beverage categories. The segment is supported by brand positioning around taste, strength, heritage, craft production, and social identity.

Beer and spirits brands often use event sponsorships, sports partnerships, music events, and digital campaigns to reach male consumers across both mature and emerging markets. Demand from male consumers is expected to remain strong, but purchasing behavior is becoming more selective. Health awareness, responsible drinking campaigns, and interest in lower-alcohol options are encouraging brands to introduce lighter, premium, and functional-positioned beverage alternatives.

Packaging Type Analysis

Bottles led the packaging type segment with 75.8% share, supported by their strong use across beer, wine, spirits, cider, and ready-to-drink alcoholic beverages. Glass bottles remain preferred for many alcoholic drinks because they protect product quality, support premium presentation, and maintain taste stability. The growth of this segment is linked to consumer preference for trusted and familiar packaging formats.

Bottles are widely used across retail shelves, restaurants, bars, hotels, and duty-free channels because they support brand visibility, portion control, and premium shelf appeal. Bottled alcoholic drinks are expected to remain dominant, especially across beer, spirits, and wine categories. However, cans, pouches, and lightweight packaging formats are gaining attention due to convenience, portability, lower transport weight, and sustainability-related packaging goals.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

On-trade channels accounted for 52.1% share, supported by demand from bars, pubs, restaurants, hotels, clubs, resorts, and event venues. This channel remains important because alcoholic drinks are strongly linked with social experiences, dining, entertainment, nightlife, tourism, and hospitality. The growth of on-trade sales can be attributed to premium consumption behavior and higher spending per serving compared with off-trade retail purchases.

Consumers often choose cocktails, draft beer, wine, premium spirits, and curated beverage menus when drinking in hospitality settings. On-trade demand is expected to remain strong as travel, dining, events, and nightlife activity continue to recover. Beverage companies are likely to focus on bartender programs, premium product placement, branded experiences, and exclusive on-premise offerings to strengthen channel performance.

Regional Analysis

Asia Pacific led the Alcoholic Drinks Market with 30.2% share, supported by a large consumer base, rising urbanization, growing middle-class spending, and strong demand across beer, spirits, and ready-to-drink beverages. China, India, Japan, South Korea, Australia, and Southeast Asian countries remain major contributors to regional consumption. The region’s growth is supported by changing drinking occasions, modern retail expansion, premiumization, and strong foodservice activity.

India and Southeast Asia are becoming important growth markets, while China is shifting toward more casual and value-focused consumption patterns. Asia Pacific is expected to remain a key market as brands expand local flavors, premium beer, whisky, ready-to-drink products, and no-alcohol or low-alcohol alternatives. At the same time, tax changes, health regulations, and responsible drinking policies will continue to shape market development.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +2.6% | Asia Pacific, 30.2% share in 2025 | Leads consumption growth. |

Europe premium beverage demand | +1.8% | UK, Germany, France, Italy, Spain | Supports high-value sales. |

North America craft and RTD growth | +1.6% | U.S. and Canada | Drives innovation demand. |

Latin America beer consumption strength | +1.2% | Brazil, Mexico, Chile, Argentina | Supports volume sales. |

Middle East and Africa selective demand | +0.7% | South Africa, UAE, selected markets | Shows controlled growth. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Beer remains leading product type | +2.1% | Asia Pacific, Europe, Latin America | Drives volume sales. |

Premiumization of spirits and wine | +1.8% | North America, Europe, Asia Pacific | Improves revenue value. |

Growth of low-alcohol beverages | +1.3% | Europe, U.S., Japan, Australia | Supports moderation trend. |

Ready-to-drink alcoholic beverages | +1.5% | U.S., Asia Pacific, Europe | Expands convenience formats. |

Experiential drinking and nightlife growth | +1.2% | Urban global markets | Supports on-trade demand. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Beverage Manufacturers | +2.1% | Global | Expands product portfolios. |

Retail and Distribution Investors | +1.6% | Asia Pacific, Europe, North America | Strengthens sales channels. |

Private Equity Firms | +1.3% | North America, Europe, Asia Pacific | Supports brand scaling. |

Hospitality and On-Trade Operators | +1.2% | Global urban markets | Drives social consumption. |

Packaging and Logistics Investors | +1.0% | Global | Improves supply efficiency. |

Segment covered in the Report

By Product Type

Beer

Wine

Spirits

Others

By End User

Male

Female

By Packaging Type

Bottles

Cans

Others

By Distribution Channel

On-Trade

Off-Trade

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising social drinking culture | +2.4% | Asia Pacific, Europe, North America | Drives consumption growth. |

Growth in premium alcoholic beverages | +2.0% | U.S., Europe, Japan, China, India | Supports higher spending. |

Expansion of on-trade channels | +1.7% | Urban markets globally | Boosts bar and restaurant sales. |

Increasing demand for beer and spirits | +1.5% | Asia Pacific, Latin America, Europe | Expands core product sales. |

Wider availability through retail and e-commerce | +1.3% | Global | Improves market access. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Strict alcohol regulations | -1.2% | U.S., Europe, Asia Pacific, Middle East | Limits market expansion. |

Rising health concerns | -1.0% | North America, Europe, urban Asia | Reduces frequent consumption. |

High taxation and excise duties | -0.9% | India, Europe, Australia, Latin America | Raises product pricing. |

Advertising restrictions | -0.7% | Global regulated markets | Limits brand promotion. |

Growing low-alcohol and alcohol-free shift | -0.6% | Europe, North America, Japan | Affects traditional demand. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Premium and craft beverage expansion | +2.2% | North America, Europe, Asia Pacific | Builds high-value growth. |

Growth in ready-to-drink cocktails | +1.8% | U.S., Japan, Australia, Europe | Supports convenience demand. |

Rising demand from emerging economies | +1.6% | India, China, Southeast Asia, Latin America | Expands consumer base. |

Alcohol e-commerce and delivery growth | +1.4% | U.S., Europe, Asia Pacific | Improves purchase convenience. |

Flavor innovation in alcoholic drinks | +1.2% | Global | Attracts younger consumers. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Compliance with changing alcohol laws | -1.0% | Global | Raises operating burden. |

Responsible drinking pressure | -0.9% | North America, Europe, Asia Pacific | Limits aggressive marketing. |

Raw material price volatility | -0.8% | Global beverage producers | Pressures production cost. |

Counterfeit and illicit alcohol trade | -0.7% | Emerging markets | Reduces formal sales. |

Brand differentiation in mature markets | -0.6% | Europe, North America | Limits pricing power. |

Recent Developments

In February 2026, Anheuser-Busch completed the acquisition of an 85% stake in BeatBox, a fast-growing ready-to-drink alcohol brand, for up to about USD 490 million. The agreement includes a path to 100% ownership after five years under a predetermined pricing formula. The deal strengthens Anheuser-Busch’s Beyond Beer portfolio, which includes Cutwater Spirits and NÜTRL Vodka Seltzer.

In February 2026, E. & J. Gallo Winery agreed to acquire 100% of Four Roses Distillery from Kirin Holdings. The transfer price was up to approximately JPY 120.0 billion, equal to USD 775 million, including about USD 50 million in possible contingent consideration tied to post-transfer net revenue targets. The deal highlights continued investor interest in premium U.S. bourbon assets.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 2.8 Trillion |

Forecast Revenue (2035) | USD 6.6 Trillion |

CAGR (2025-2035) | 8.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product Type (Beer, Wine, Spirits, Others), By End User (Male, Female), By Packaging Type (Bottles, Cans, Others), By Distribution Channel (On-Trade, Off-Trade) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Anheuser-Busch InBev SA/NV, Heineken Holding NV, Diageo PLC, Constellation Brands Inc., Pernod Ricard SA, Bacardi Limited, Suntory Holdings Limited, Molson Coors Beverage Company, Asahi Group Holdings Ltd., Carlsberg A/S |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Anheuser-Busch InBev SA/NV

Heineken Holding NV

Diageo PLC

Constellation Brands Inc.

Pernod Ricard SA

Bacardi Limited

Suntory Holdings Limited

Molson Coors Beverage Company

Asahi Group Holdings Ltd.

Carlsberg A/S

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Dairy Products Market to Exceed USD 919.1 Billion by 2035

Global Dairy Products Market Size, Share Analysis By Product (Milk, Cheese, Yogurt, Butter, Cream, Others), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others) , By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Meat and Poultry Market to Exceed USD 568.2 Billion by 2035

Global Meat and Poultry Market Size, Share Analysis By Type (Flavoured Meat and Poultry, Unflavoured White Meat and Poultry), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bottled Water Market to Cross USD 896.0 Billion by 2035

Global Bottled Water Market Size By Product (Spring Water, Purified Water, Mineral Water, Sparkling Water, Others), By Packaging Type (PET, Cans, Others), By Packaging Size (Small, Medium, Bulk), By Price Range (Mass, Premium), By Distribution Channel (On-Trade, Off-Trade), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Chocolate Confectionery Market to hit USD 368.5 Billion by 2035

Global Chocolate Confectionery Market Size By Product (Chocolate Bars, Boxed Chocolates, Chips and Bites, Truffles and Cups), By Chocolate Type (Milk Chocolate, Dark Chocolate, White Chocolate), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores and Chocolatiers, Online and E-commerce, Others) , By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035