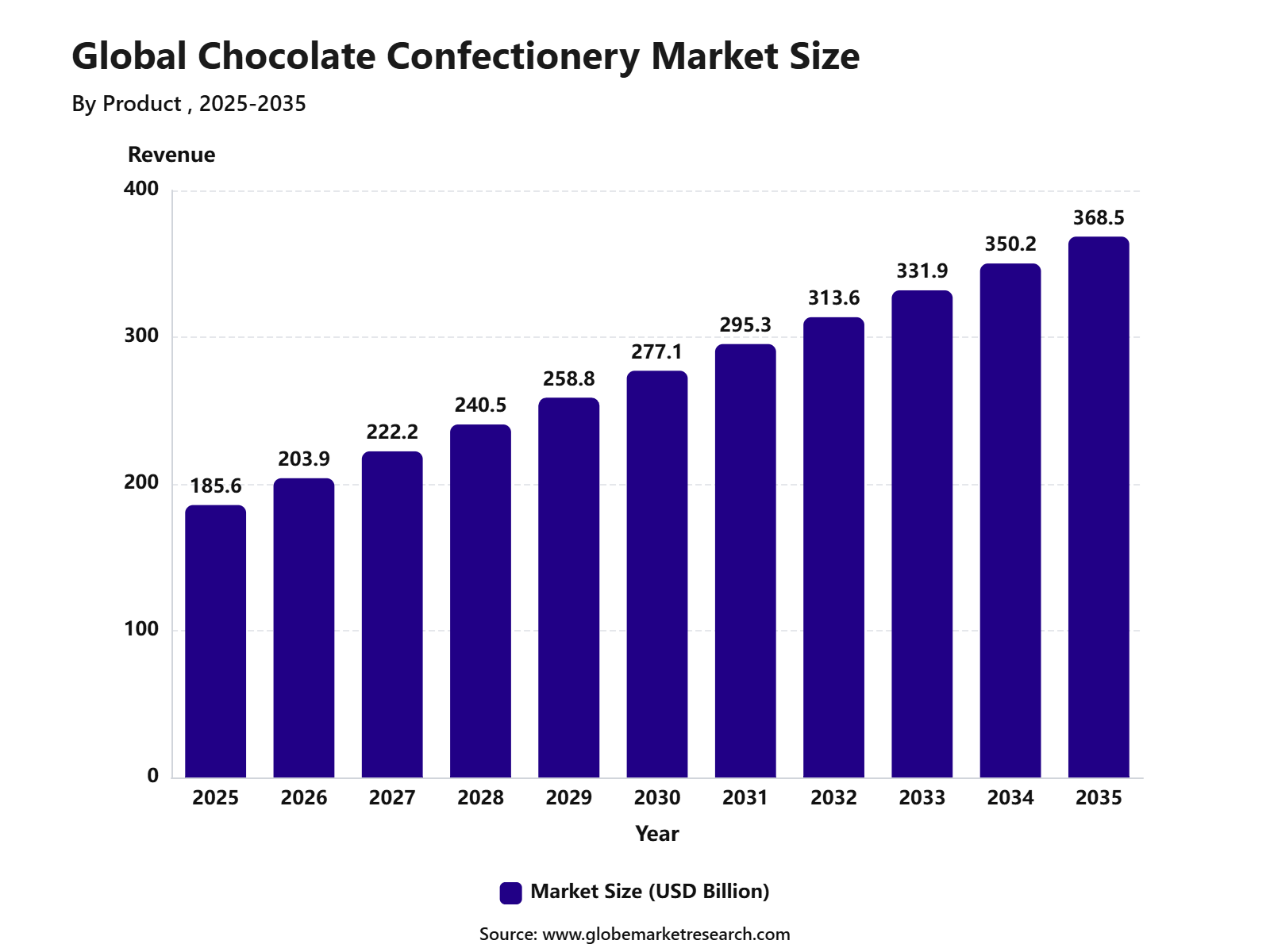

Revenue, 2025

$ 185.6 Bn

Forecast, 2035

$ 368.5 Bn

CAGR, 2025-2035

7.1%

Report Coverage

Global

Market Size and Forecast

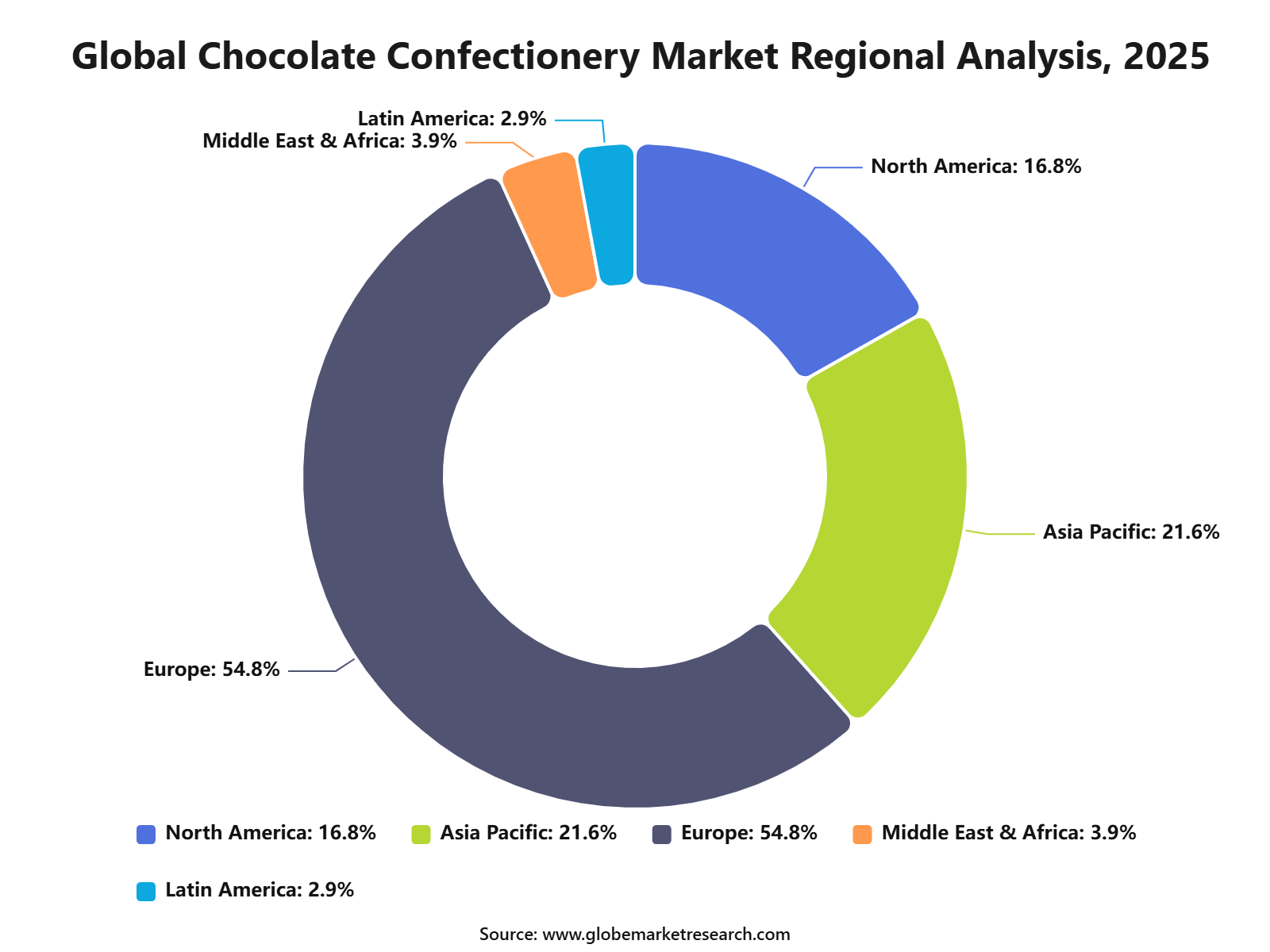

The Global Chocolate Confectionery Market was valued at USD 185.6 billion in 2025 and is projected to reach USD 368.5 billion by 2035, growing at a CAGR of 7.1% from 2025 to 2035. Europe held the largest regional share of 54.8% in 2025, supported by high chocolate consumption, strong premium confectionery demand, established cocoa processing capacity, and wide availability of branded and artisanal chocolate products.

Chocolate confectionery includes chocolate bars, boxed chocolates, truffles, pralines, chocolate-coated products, chips, bites, and seasonal chocolate items. The growth of the market can be attributed to rising demand for premium chocolates, gifting products, clean-label ingredients, dark chocolate, and innovative flavors. Increasing consumer preference for indulgent snacks and portion-controlled confectionery is also supporting steady market expansion.

The market outlook remains positive as manufacturers focus on healthier formulations, sustainable cocoa sourcing, sugar-reduced products, and premium packaging. Europe is expected to maintain its leading position due to strong chocolate culture, high per capita consumption, well-developed retail channels, and rising demand for ethically sourced and high-quality cocoa-based products.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Chocolate bars led the product segment with 34.7% share , supported by strong consumer preference for convenient, portioned, and impulse-purchase chocolate formats.

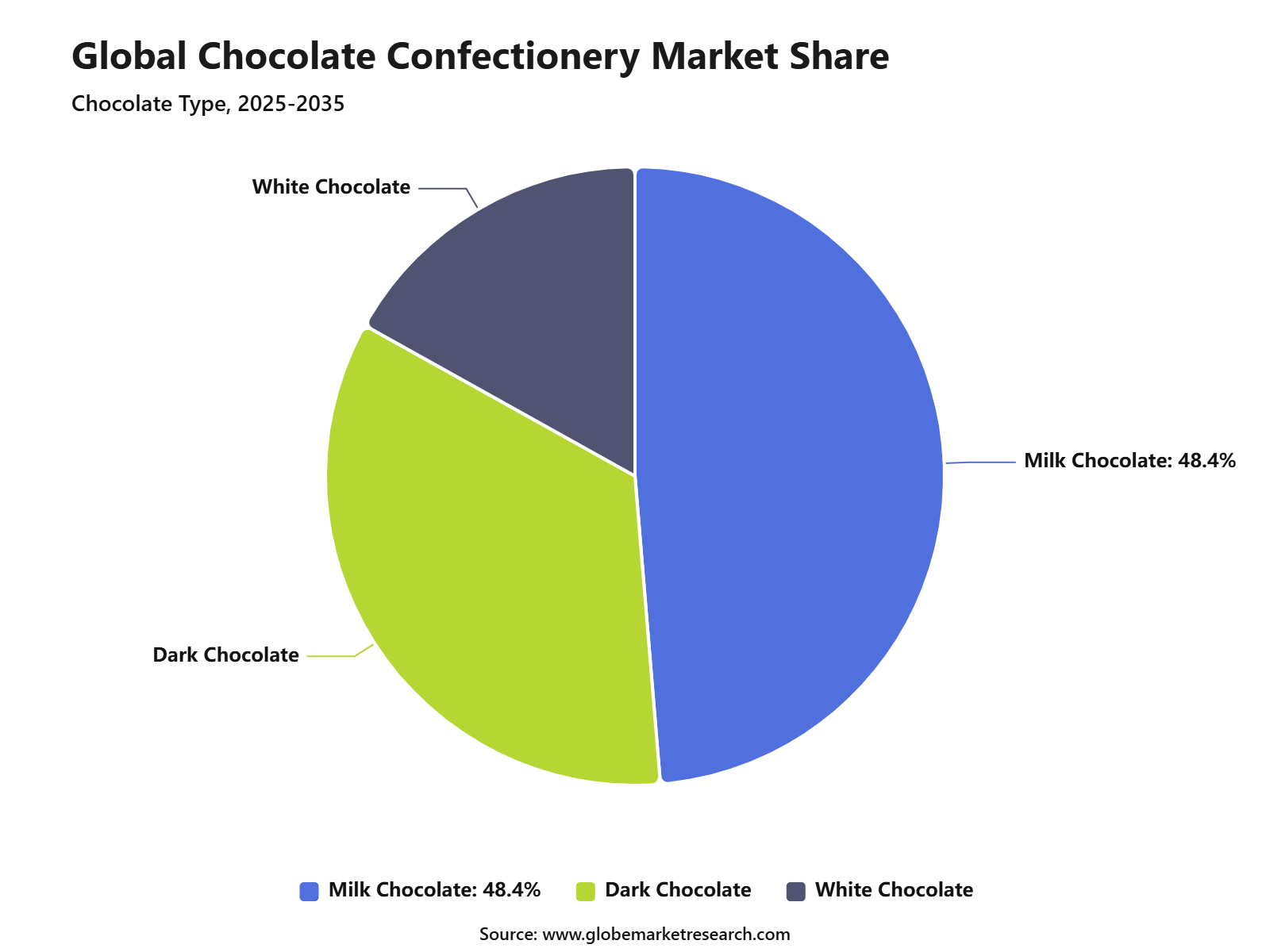

Milk chocolate accounted for 48.4% share by chocolate type, driven by its smooth taste, broad consumer acceptance, and strong use across bars, boxed chocolates, and snack products.

Supermarkets and hypermarkets held 44.4% share by distribution channel, supported by wide product availability, promotional pricing, seasonal displays, and high consumer footfall.

Europe led the chocolate confectionery market with 54.8% share, supported by strong chocolate consumption, established confectionery brands, premium product demand, and mature retail networks

Go-to-Market Strategy

The Chocolate Confectionery Market needs a product-format-led go-to-market strategy because consumers buy chocolate differently across bars, boxed chocolates, countlines, truffles, seasonal packs, gifting products, and bite-size formats. Brands should position products around taste, cocoa quality, texture, portion control, gifting appeal, premium ingredients, and seasonal demand. Cocoa cost remains a central sales factor because Reuters reported that cocoa prices nearly tripled to above USD 12,000 per metric ton in 2024 before falling sharply from late-2024 records. This volatility has forced brands to manage pricing, pack sizes, recipes, and promotional calendars more carefully.

Sales economics are strongest when companies balance real chocolate positioning with margin protection. Reuters reported in May 2026 that cocoa futures had fallen nearly 70% from late-2024 records, encouraging some chocolate makers to return to higher cocoa content after earlier use of wafers, fillers, smaller bars, and chocolate alternatives. However, cocoa price changes can take around 10 months to reach retail shelves because manufacturers hedge purchases and hold inventories. This means consumer prices may remain sticky even when raw cocoa costs decline.

Risk Factors & Market Barriers

The main risk factor is cocoa supply volatility. ICCO’s May 2026 bulletin estimated 2024/25 world cocoa production at 4.723 million tonnes and grindings at 4.628 million tonnes , with a revised global surplus of 48,000 tonnes . Although this shows some supply improvement after the severe 2023/24 deficit, the stocks-to-grindings ratio remained at 28.5%, which means the market is still sensitive to weather, disease, and supply disruption.

Climate risk is also a major barrier. Reuters reported in June 2026 that a strong El Niño pattern could develop in the second half of 2026, and cocoa is one of the tropical commodities most exposed to this risk. Every strong El Niño in the past 55 years has negatively affected cocoa crops, while recent West African weather stress and crop disease contributed to the price surge seen in 2024. This creates cost uncertainty for chocolate brands, especially those with high cocoa-content products.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for chocolate confectionery is spread across milk chocolate, dark chocolate, white chocolate, boxed chocolates, chocolate bars, chips and bites, truffles, seasonal packs, gifting products, premium chocolates, private label products, and chocolate-coated snacks. Seasonal demand remains especially important during Valentine’s Day, Easter, Halloween, Christmas, weddings, and festive gifting periods. Premium and gifting formats can support stronger margins because consumers often pay more for presentation, brand trust, cocoa origin, and special ingredients.

Revenue opportunities are also strengthening around real chocolate reformulation and premiumization. Reuters reported that lower cocoa prices are encouraging some companies to move back toward real chocolate after earlier cost-driven use of cocoa-light alternatives. Brazil’s 2026 rule requiring products labeled as dark chocolate to contain at least 35% cocoa solids also reflects a broader regulatory and consumer push toward clearer chocolate identity.

Financial Impact

The financial impact can improve when cocoa prices soften, but the benefit is not immediate. Chocolate makers often buy cocoa through hedging contracts and hold inventories, so lower bean prices can take months to improve production costs. Reuters reported that supermarkets and buyers had been pressuring chocolate makers to lower prices since mid-2025, while some manufacturers had already started trimming selected chocolate prices in Europe.

Financial risk remains linked to cocoa volatility, sugar prices, dairy costs, packaging, labor, energy, freight, and promotional spending. Companies with strong sourcing contracts, flexible recipes, premium brands, and clear labeling are better placed to protect margins. The strongest financial resilience is expected from brands that combine cocoa supply security, responsible sourcing, product innovation, and disciplined pricing instead of depending only on short-term commodity cost movements.

Product Analysis

Chocolate bars led the Chocolate Confectionery Market with 34.7% share , supported by strong consumer preference for convenient, portioned, and ready-to-eat confectionery products. Chocolate bars are widely purchased for personal consumption, gifting, impulse buying, travel snacking, and seasonal occasions. The growth of this segment can be attributed to broad product availability across supermarkets, convenience stores, online platforms, and specialty retailers.

Demand is also supported by innovation in flavors, fillings, textures, portion sizes, premium cocoa blends, and healthier-positioned variants. Chocolate bars are expected to remain the leading product type because they offer strong brand recall, easy shelf placement, and frequent repeat purchases. Manufacturers are likely to focus on premium bars, reduced-sugar options, sustainable cocoa sourcing, and smaller pack formats to meet changing consumer preferences.

Chocolate Type Analysis

Milk chocolate accounted for 48.4% share, making it the leading chocolate type in the Chocolate Confectionery Market. Its dominance is supported by a smooth taste, creamy texture, wider consumer acceptance, and strong popularity across children, young adults, and family buyers. The segment benefits from high use in bars, boxed chocolates, molded chocolates, coated snacks, seasonal confectionery, and gifting products.

Milk chocolate is also preferred because it supports a wide range of inclusions such as nuts, caramel, wafers, biscuits, fruits, and nougat. Milk chocolate is expected to maintain strong demand due to its mainstream taste profile and strong retail visibility. However, rising cocoa costs, sugar-reduction trends, and demand for cleaner labels are encouraging producers to improve recipes, portion control, and ingredient transparency.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

Supermarkets and hypermarkets held 44.4% share , supported by high footfall, strong shelf visibility, wide product variety, and frequent consumer purchases. These stores remain important for chocolate confectionery because shoppers often buy chocolate during regular grocery trips and seasonal shopping periods. The growth of this channel can be linked to organized retail expansion, promotional offers, multipack sales, seasonal displays, and private-label product availability.

Supermarkets and hypermarkets also allow consumers to compare brands, pack sizes, prices, and flavors before purchase. This channel is expected to remain strong because chocolate confectionery is highly dependent on impulse buying and attractive in-store placement. Retailers are likely to continue using checkout displays, festive promotions, bundled packs, and premium shelves to drive chocolate sales.

Regional Analysis

Europe led the Chocolate Confectionery Market with 54.8% share , supported by strong chocolate consumption, mature confectionery manufacturing, premium chocolate culture, and high demand for seasonal and gifting products. Countries such as Germany, Switzerland, Belgium, France, the United Kingdom, Italy, and the Netherlands remain important contributors to regional demand.

The region’s dominance is supported by a long-established chocolate industry, strong retail penetration, and consumer preference for premium, milk, dark, filled, and artisanal chocolate products. Europe also remains a major center for chocolate innovation, with demand shaped by sustainability, cocoa sourcing, reduced sugar, and premiumization trends.

Europe is expected to remain the leading regional market as consumers continue to purchase chocolate across daily snacking, gifting, holidays, and special occasions. Future growth opportunities are likely to be seen in premium bars, sustainable cocoa products, healthier formulations, plant-based chocolate, and seasonal confectionery launches.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Europe market leadership | +2.3% | Europe, 54.8% share in 2025 | Leads premium consumption. |

North America premium chocolate demand | +1.3% | U.S. and Canada | Supports high-value sales. |

Asia Pacific rising confectionery consumption | +1.4% | China, India, Japan, South Korea | Builds volume growth. |

Latin America cocoa-linked demand | +0.8% | Brazil, Mexico, Colombia | Supports gradual expansion. |

Middle East and Africa gifting demand | +0.7% | UAE, Saudi Arabia, South Africa | Shows niche growth. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Premium and artisanal chocolate growth | +1.7% | Europe, North America | Supports higher margins. |

Milk chocolate category strength | +1.4% | Global | Drives mass consumption. |

Chocolate bars as leading format | +1.3% | Europe, Asia Pacific, North America | Supports daily purchases. |

Sustainable and traceable cocoa | +1.0% | Europe, North America | Improves brand credibility. |

Functional and reduced-sugar chocolates | +0.9% | Developed markets | Supports health positioning. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Confectionery Manufacturers | +1.5% | Global | Expands product portfolios. |

+1.3% | Europe, North America, Asia Pacific | Supports category growth. | |

Private Equity Firms | +1.0% | Europe, North America, Asia Pacific | Enables brand scaling. |

Sustainable Sourcing Investors | +0.9% | Europe and cocoa supply regions | Improves cocoa traceability. |

Retail and E-commerce Investors | +0.8% | Global | Strengthens sales channels. |

Segment covered in the Report

By Product

Chocolate Bars

Boxed Chocolates

Chips and Bites

Truffles and Cups

By Chocolate Type

Milk Chocolate

Dark Chocolate

White Chocolate

By Distribution Channel

Supermarkets and Hypermarkets

Convenience Stores

Specialty Stores and Chocolatiers

Online and E-commerce

Others

By Region

North America

Asia Pacific

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for premium chocolates | +1.9% | Europe, North America, Asia Pacific | Supports high-value sales. |

Growing gifting and festive consumption | +1.6% | Europe, Asia Pacific, Middle East | Drives seasonal demand. |

Expansion of modern retail channels | +1.3% | Global | Improves product availability. |

Increasing demand for milk chocolate | +1.2% | Europe, North America, Asia Pacific | Supports mass-market growth. |

Product innovation in flavors and formats | +1.0% | Global | Expands consumer interest. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Cocoa price volatility | -1.0% | Global | Pressures production cost. |

Rising health concerns over sugar | -0.9% | North America, Europe, urban Asia | Limits frequent consumption. |

High cost of premium ingredients | -0.7% | Europe, North America | Affects margins. |

Supply chain risk in cocoa sourcing | -0.6% | Africa-linked global supply | Impacts availability. |

Competition from healthier snacks | -0.5% | Developed markets | Slows demand growth. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in dark chocolate products | +1.5% | Europe, North America, Japan | Supports health-focused demand. |

Expansion of sugar-free chocolates | +1.2% | U.S., Europe, urban Asia | Opens better-for-you segment. |

Premium boxed chocolate demand | +1.1% | Europe, Middle East, Asia Pacific | Supports gifting sales. |

E-commerce chocolate sales growth | +1.0% | Global | Expands direct reach. |

Sustainable cocoa sourcing | +0.9% | Europe, North America | Builds brand trust. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining affordable pricing | -0.8% | Global mass market | Affects volume sales. |

Climate impact on cocoa production | -0.7% | Cocoa-producing regions | Raises sourcing risk. |

Managing product shelf life | -0.6% | Warm climate markets | Increases storage needs. |

Regulatory pressure on sugar content | -0.5% | Europe, North America | Requires reformulation. |

Counterfeit and low-quality products | -0.4% | Emerging markets | Reduces brand confidence. |

Recent Developments

In May 2026, cocoa supply conditions improved compared with the previous season. The International Cocoa Organization revised global cocoa production to 4.723 million tonnes, up 8.3%, while grindings were estimated at 4.628 million tonnes , down 3.8% . The cocoa balance moved from a 492,000-tonne deficit in 2023/24 to a 48,000-tonne surplus in 2024/25, indicating some easing in raw material pressure.

In March 2026, the U.S. chocolate confectionery category remained the largest part of the confectionery industry. Chocolate generated USD 28.4 billion , accounting for 51.7% of total U.S. confectionery sales, while non-chocolate candy generated USD 22.5 billion and gum generated USD 4.1 billion . This shows that chocolate continues to be the core revenue driver in confectionery retail.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 185.6 Billion |

Forecast Revenue (2035) | USD 368.5 Billion |

CAGR (2025-2035) | 7.1% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product (Chocolate Bars, Boxed Chocolates, Chips and Bites, Truffles and Cups), By Chocolate Type (Milk Chocolate, Dark Chocolate, White Chocolate), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores and Chocolatiers, Online and E-commerce, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Barry Callebaut, Nestlé S.A., Ferrero SpA, The Hershey Company, Mars, Incorporated, Mondelez International, Chocoladefabriken Lindt & Sprüngli AG, CEMOI Group, Lake Champlain Chocolates, LOTTE |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Barry Callebaut

Nestlé S.A.

Ferrero SpA

The Hershey Company

Mars, Incorporated

Mars, Incorporated

Chocoladefabriken Lindt & Sprüngli AG

CEMOI Group

Lake Champlain Chocolates

LOTTE

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Dairy Products Market to Exceed USD 919.1 Billion by 2035

Global Dairy Products Market Size, Share Analysis By Product (Milk, Cheese, Yogurt, Butter, Cream, Others), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online, Others) , By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Meat and Poultry Market to Exceed USD 568.2 Billion by 2035

Global Meat and Poultry Market Size, Share Analysis By Type (Flavoured Meat and Poultry, Unflavoured White Meat and Poultry), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Convenience Stores, Online Retail), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Alcoholic Drinks Market to Cross USD 6.6 Trillion by 2035

Global Alcoholic Drinks Market Size By Product Type (Beer, Wine, Spirits, Others), By End User (Male, Female), By Packaging Type (Bottles, Cans, Others), By Distribution Channel(On-Trade, Off-Trade), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bottled Water Market to Cross USD 896.0 Billion by 2035

Global Bottled Water Market Size By Product (Spring Water, Purified Water, Mineral Water, Sparkling Water, Others), By Packaging Type (PET, Cans, Others), By Packaging Size (Small, Medium, Bulk), By Price Range (Mass, Premium), By Distribution Channel (On-Trade, Off-Trade), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035