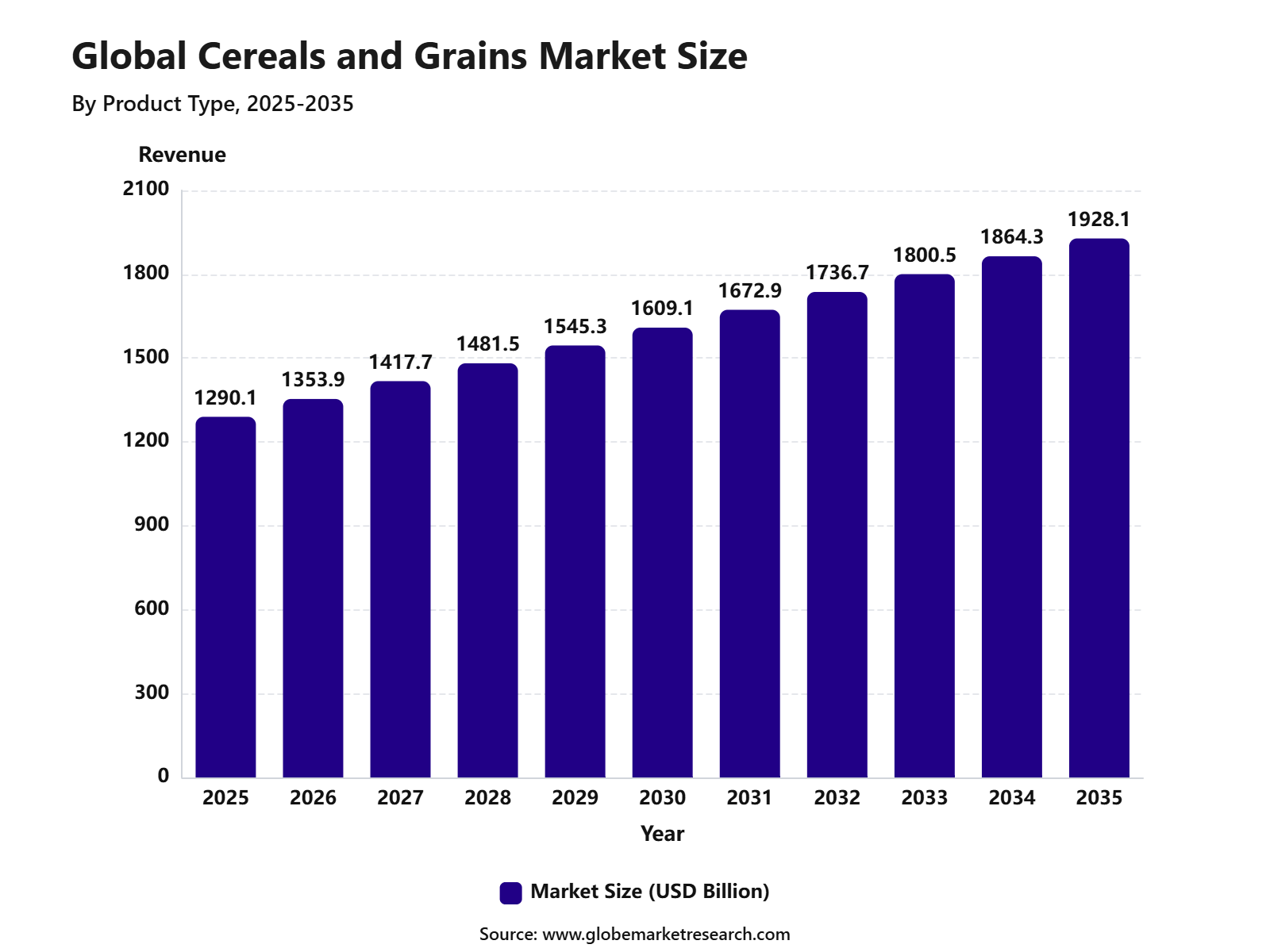

Revenue, 2025

$ 1,290.1 Bn

Forecast, 2035

$ 1,928.1 Bn

CAGR, 2025-2035

4.1%

Report Coverage

Global

Market Size and Forecast

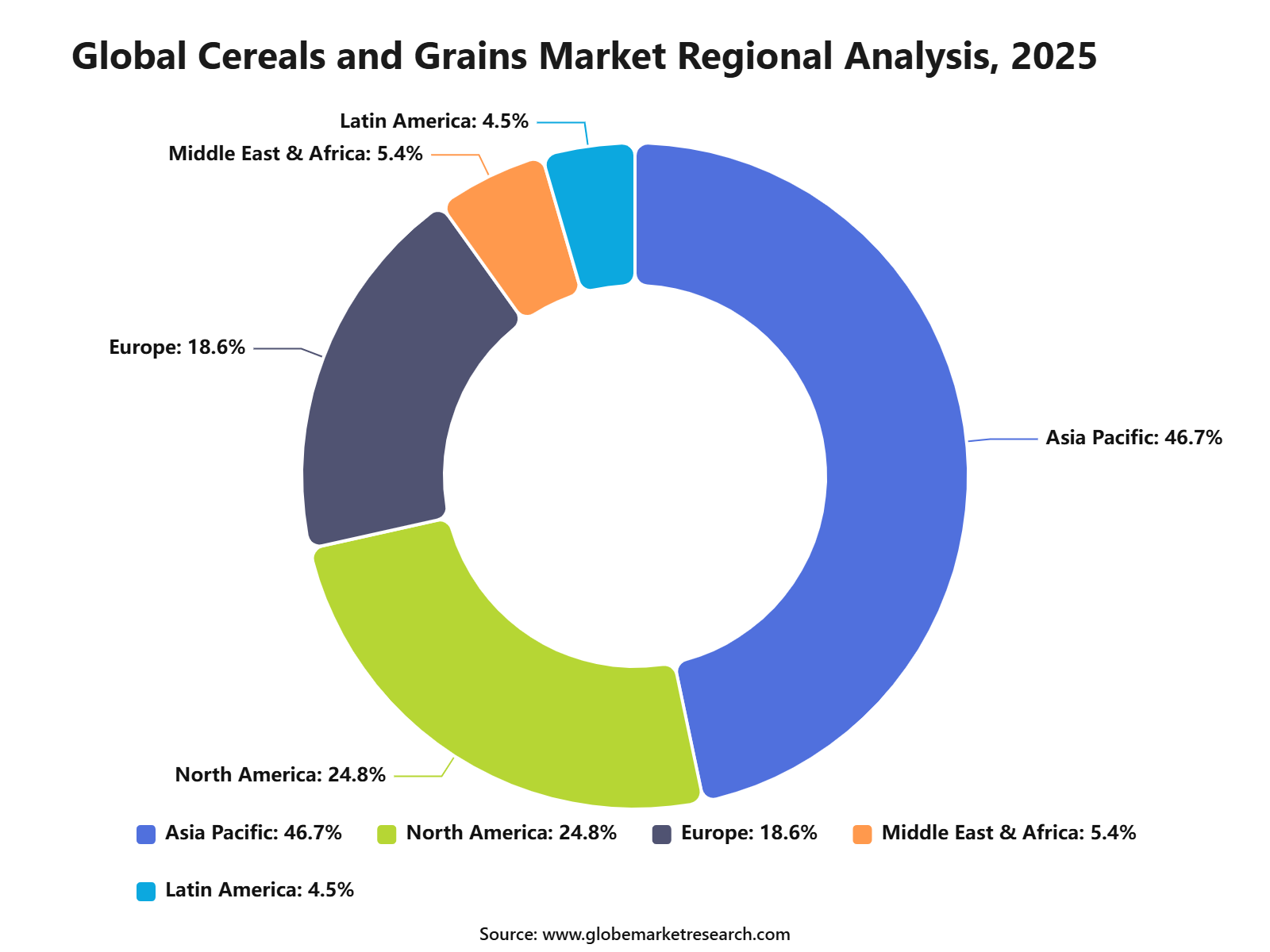

The Global Cereals and Grains Market reached USD 1,290.1 billion in 2025 and is expected to grow to USD 1,928.1 billion by 2035, registering a CAGR of 4.1% from 2025 to 2035. Asia Pacific held the largest regional share of 46.7% in 2025, supported by high rice, wheat, maize, and millet consumption across China, India, Southeast Asia, and other densely populated countries.

The Cereals and Grains Market refers to the production, processing, distribution, and consumption of staple crops such as maize, wheat, rice, barley, oats, sorghum, and other grains. These products are widely used in food processing, animal feed, bakery products, breakfast cereals, beverages, and industrial applications. Demand is strongly supported by population growth, rising food security needs, and increasing use of grains in packaged and convenience foods.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains steady as cereals and grains continue to form the base of global food supply chains. Growth can be attributed to higher demand for animal feed, expanding grain processing capacity, improved storage and logistics systems, and increasing adoption of whole grain and fortified grain-based products. The market is also being shaped by climate-resilient crop development, precision farming, and government support for staple food production.

Key Market Insights

Maize led the product type segment with 36.8% share, supported by its wide use in food processing, animal feed, starch production, and industrial applications.

Animal feed accounted for 45.6% share by application, driven by strong demand from poultry, livestock, aquaculture, and dairy farming sectors.

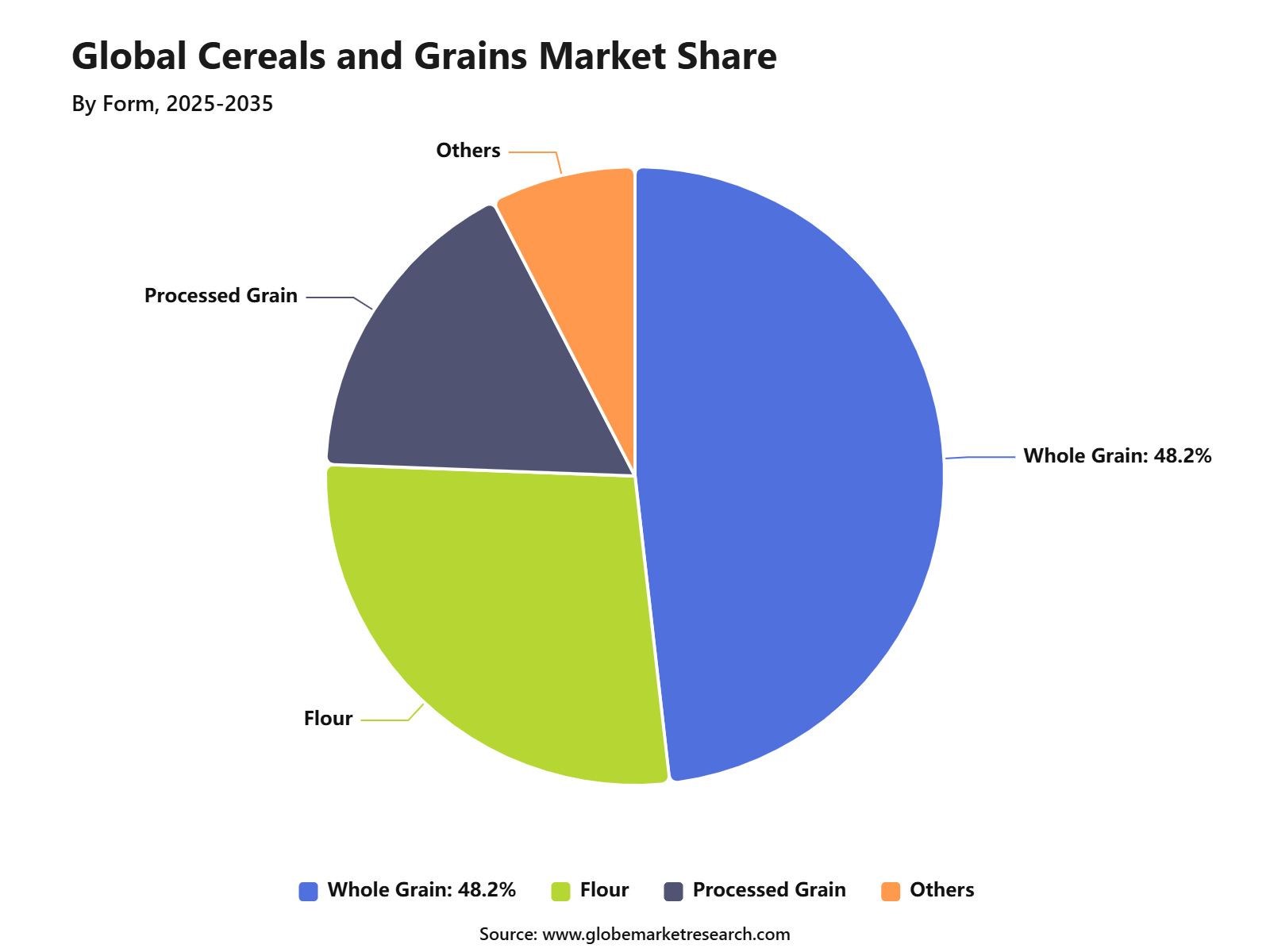

Whole grain held 48.2% share by form, supported by rising demand for less-processed grains, nutritional value, and broad use in staple food products.

Wholesalers and distributors captured 53.4% share by distribution channel, driven by bulk trading, strong supply networks, and large-scale procurement by food and feed manufacturers.

Asia Pacific led the cereals and grains market with 46.7% share, supported by large population, high staple grain consumption, strong agricultural production, and expanding food processing demand.

Go-To-Market-Strategy

The Cereals and Grains Market should be approached through a supply-secure and channel-diversified strategy in 2026, as grain demand is linked to food consumption, animal feed, milling, breakfast cereals, bakery, brewing, and packaged food manufacturing. FAO projects world cereal utilization to reach 2,969 million tonnes in 2026/27, with food consumption of cereals expected to rise 1.0% and feed use expected to grow 0.5% from 2025/26.

In retail, brands can gain stronger visibility through fortified cereals, whole-grain products, ready-to-cook grains, organic grains, and regional staples such as rice, wheat, corn, oats, millet, and barley. Since FAO reported that the Cereal Price Index reached 114.3 points in May 2026, up 2.6% from April and 4.9% year-on-year, pricing, pack size, and long-term procurement contracts are expected to remain central to market competitiveness.

Risk Factors & Market Barriers

The major risk factor in the Cereals and Grains Market is production volatility caused by weather, drought, fertilizer prices, geopolitical disruptions, and changing trade flows. USDA’s May 2026 WASDE reported that the first survey-based U.S. 2026/27 winter wheat production forecast was down 25% from the previous year, mainly due to lower output expectations. This indicates that even mature grain-producing regions remain exposed to climate and yield risks, which can affect supply reliability and price movement.

Market barriers also include high storage costs, transport bottlenecks, import dependency, food safety standards, and government intervention in grain exports or stockholding. World Bank commodity reporting in 2026 highlighted pressure from energy and fertilizer costs, which directly affects grain production economics because farming, drying, storage, and logistics are energy-intensive. These risks can increase working capital needs for grain traders, millers, and processors, especially when prices move quickly across wheat, maize, rice, and coarse grains.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities across the Cereals and Grains Market are spread across staple food, feed, food processing, and packaged consumer products. Wheat and rice continue to support large-volume food demand, while maize remains important for animal feed, starch, ethanol, and industrial use. India’s rice stocks reached 68.43 million tonnes as of June 1, 2026, while wheat stocks reached 53.41 million tonnes, showing strong buffer availability in one of the world’s largest grain-producing and consuming markets.

Across regions, Asia Pacific is expected to remain a major demand center due to high rice and wheat consumption, large populations, and expanding packaged food demand. North America and Europe remain strong in wheat, corn, oats, breakfast cereals, animal feed, and processed grain products. Revenue growth can be strengthened through premium grain blends, fortified staples, organic cereals, millet-based products, and private-label packaged grains, as consumers are seeking affordable nutrition, convenience, and better shelf life.

Financial Impact

The financial impact of the Cereals and Grains Market in 2026 will depend on price control, sourcing flexibility, and inventory management. Grain processors can face margin pressure when raw grain prices rise faster than finished product pricing. World Bank data indicated that grain prices rose by 5.0% in the first quarter of 2026 compared with the previous quarter, led by a 9.0% rise in wheat and a 4.0% rise in maize, which shows the need for hedging, multi-origin sourcing, and long-term supplier contracts.

Companies can improve profitability through value-added processing, branded packaging, fortified grain products, and efficient logistics. Bulk grain sales usually carry lower margins, while processed flour, breakfast cereals, instant grain mixes, specialty rice, and ready-to-cook products provide better unit economics. The market outlook remains positive, but financial performance will be stronger for players that manage commodity volatility, reduce wastage, improve storage efficiency, and align product formats with price-sensitive consumer demand.

Product Type Analysis

Maize led the Cereals and Grains Market with 36.8% share, supported by its wide use in food, animal feed, starch, sweeteners, ethanol, and industrial processing. It is one of the most versatile grain crops because it serves both human consumption and large-scale commercial applications.

The growth of this segment can be attributed to strong demand from feed manufacturers, food processors, and bio-based industrial users. Maize is widely used in poultry feed, livestock feed, corn flour, breakfast cereals, snacks, syrups, and processed food ingredients.

Maize is expected to remain a leading product type due to its high yield potential, broad cultivation base, and strong role in feed and industrial value chains. Demand is likely to remain supported by livestock production, packaged food growth, grain processing, and rising use of maize-based ingredients.

Application Analysis

Animal feed accounted for 45.6% share of the Cereals and Grains Market, making it the leading application segment. Cereals and grains are key feed ingredients because they provide energy, carbohydrates, and essential nutrients for poultry, cattle, pigs, aquaculture, and other livestock. The growth of this segment is being driven by rising demand for meat, dairy, eggs, and animal protein products.

Feed manufacturers use maize, wheat, barley, sorghum, oats, and other grains to produce balanced feed formulations for commercial livestock production. Animal feed is expected to remain the dominant application as livestock farming becomes more organized and feed efficiency becomes a priority. Demand will be supported by poultry production, dairy expansion, aquaculture growth, and the need for cost-effective grain-based feed ingredients.

Form Analysis

Whole grain held 48.2% share, supported by strong demand from food processing, milling, feed production, and direct grain consumption. Whole grains are valued because they retain the bran, germ, and endosperm, making them important for both nutrition-focused food products and raw material processing. The segment is supported by growing consumer interest in fiber-rich, minimally processed, and healthier grain-based foods.

Whole grain products are used in bread, cereals, flour, snacks, bakery products, ready meals, and traditional staple foods. Whole grain demand is expected to remain strong as consumers continue to seek healthier carbohydrate options and food manufacturers expand whole grain product lines. Growth will also be supported by clean-label food trends, fortified grain products, and wider use of whole grains in bakery and breakfast categories.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFDistribution Channel Analysis

Wholesalers and distributors led the distribution channel segment with 53.4% share, supported by their role in bulk grain movement, storage, aggregation, and supply to food processors, feed manufacturers, retailers, and industrial buyers. This channel is important because cereals and grains are traded in large volumes across regional and international supply chains.

The growth of this segment can be linked to the need for efficient procurement, warehousing, quality grading, and logistics management. Wholesalers and distributors help connect farmers, grain elevators, mills, feed plants, exporters, and food manufacturers with stable supply.

Wholesalers and distributors are expected to remain important because grain markets depend on scale, storage capacity, and reliable movement from production areas to demand centers. Demand will also be supported by modern grain handling systems, digital commodity trading, bulk logistics, and growing processed food and feed industries.

Regional Analysis

Asia Pacific led the Cereals and Grains Market with 46.7% share, supported by a large population base, high food grain consumption, strong livestock feed demand, and major cereal production across China, India, Southeast Asia, Pakistan, Japan, and Australia. The region has strong demand for rice, wheat, maize, barley, and other grains across food, feed, and industrial applications.

The growth of Asia Pacific is being supported by rising urbanization, higher animal protein consumption, expanding food processing, and growing demand for packaged grain-based products. The region also remains central to rice and wheat consumption, while maize demand is being supported by livestock and poultry feed industries.

Asia Pacific is expected to remain the leading regional market due to its scale of consumption, agricultural production base, and growing grain processing capacity. Opportunities are likely to remain strong in maize, whole grains, animal feed, grain milling, breakfast cereals, bakery ingredients, and bulk grain distribution.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +1.6% | Asia Pacific, 46.7% share in 2025 | Leads production and demand. |

North America grain export strength | +0.8% | U.S. and Canada | Supports global supply. |

Europe whole grain demand | +0.6% | Germany, France, UK, Italy | Drives health-focused use. |

Latin America maize and feed growth | +0.5% | Brazil, Argentina, Mexico | Supports feed demand. |

Middle East and Africa food security demand | +0.5% | GCC, Egypt, Nigeria, South Africa | Builds import demand. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maize remains leading product type | +1.0% | Asia Pacific, Americas, Africa | Supports high-volume demand. |

Animal feed remains key application | +0.9% | Asia Pacific, North America, Europe | Drives bulk usage. |

Whole grain consumption growth | +0.7% | Europe, North America, urban Asia | Supports health positioning. |

Wholesaler and distributor channel strength | +0.6% | Global | Supports large-scale movement. |

Digital grain trading platforms | +0.4% | Developed and emerging markets | Improves market access. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Grain Producers and Agribusinesses | +0.9% | Global | Expands crop supply. |

Animal Feed Companies | +0.8% | Asia Pacific, Americas, Europe | Drives bulk grain use. |

Food Processing Companies | +0.7% | Global | Builds value-added demand. |

Storage and Logistics Investors | +0.6% | Asia Pacific, Africa, Latin America | Improves supply efficiency. |

Commodity Traders and Distributors | +0.5% | Global | Strengthens market flow. |

Segment Covered in the Report

By Product Type

Wheat

Rice

Maize

Barley

Oats

Sorghum

Others

By Application

Food and Beverage

Animal Feed

Biofuel

Industrial Use

Others

By Form

Whole Grain

Flour

Processed Grain

Others

By Distribution Channel

Direct Sales

Wholesalers and Distributors

Retail

Online

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for staple food crops | +1.1% | Asia Pacific, Africa, Middle East | Drives grain consumption. |

Growth in animal feed applications | +0.9% | Asia Pacific, North America, Europe | Supports bulk grain demand. |

Increasing population and food security needs | +0.8% | India, China, Africa, Southeast Asia | Expands cereal production. |

Rising use of maize and wheat in processed foods | +0.6% | Global | Supports value-added demand. |

Expansion of organized grain trade | +0.5% | Asia Pacific, North America, Europe | Improves market supply. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Climate variability and crop yield risk | -0.7% | Global farming regions | Affects production stability. |

Volatility in grain prices | -0.6% | Global | Creates buyer uncertainty. |

High fertilizer and input costs | -0.5% | Asia Pacific, Africa, Latin America | Pressures farmer margins. |

Storage and post-harvest losses | -0.4% | Emerging markets | Reduces usable supply. |

Trade restrictions and export controls | -0.3% | Global grain trade routes | Disrupts market flow. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in maize-based applications | +1.0% | Asia Pacific, North America, Latin America | Drives feed and food use. |

Expansion of animal feed production | +0.8% | China, India, Brazil, U.S. | Supports grain consumption. |

Demand for whole grain products | +0.7% | North America, Europe, urban Asia | Builds health-focused demand. |

Investment in grain storage infrastructure | +0.6% | Asia Pacific, Africa, Middle East | Reduces supply losses. |

Growth in food processing industries | +0.5% | Asia Pacific, Latin America | Expands industrial usage. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing weather-related supply shocks | -0.6% | Global | Impacts crop availability. |

Maintaining grain quality during storage | -0.5% | Emerging and humid regions | Requires better storage. |

Balancing food and feed demand | -0.4% | Asia Pacific, North America | Affects price stability. |

Soil degradation and water stress | -0.4% | Asia Pacific, Africa, Latin America | Limits yield growth. |

Logistics bottlenecks in grain movement | -0.3% | Export and import markets | Delays supply delivery. |

Recent Developments

June 2026: COFCO International signed an agreement with Thailand’s Thanakorn Vegetable Oil Products to expand trade in certified sustainable soybeans and soy-based products. The partnership includes the use of traceability systems, satellite monitoring, and digital tools to improve supply chain transparency.

April 2026: Olam Group completed the sale of a 44.58% stake in Olam Agri to SALIC, the food and agriculture investment arm of Saudi Arabia’s Public Investment Fund. The transaction was valued at about USD 1.88 billion, with an implied full equity valuation of USD 4.00 billion for Olam Agri.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 1,290.1 Billion |

Forecast Revenue (2035) | USD 1,928.1 Billion |

CAGR (2025-2035) | 4.1% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Product Type (Wheat, Rice, Maize, Barley, Oats, Sorghum, Others), By Application (Food and Beverage, Animal Feed, Biofuel, Industrial Use, Others), By Form (Whole Grain, Flour, Processed Grain, Others), By Distribution Channel (Direct Sales, Wholesalers and Distributors, Retail, Online) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Cargill, Incorporated, Archer Daniels Midland Company, Bunge Global SA, Louis Dreyfus Company, COFCO International, CHS Inc., Olam Agri, Viterra, Richardson International, GrainCorp |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Cargill, Incorporated

Archer Daniels Midland Company

Bunge Global SA

Louis Dreyfus Company

COFCO International

CHS Inc.

Olam Agri

Viterra

Richardson International

GrainCorp

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Food and Beverages

Snack Food Market Size to hit USD 1,157.5 Bn by 2035

Global Snack Food Market Size, Share Analysis By Product Type (Chips and Crisps, Nuts and Seeds, Biscuits and Cookies, Popcorn, Meat Snacks, Others), By Category (Conventional Snacks, Healthy Snacks), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Specialty Stores, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Canned Food Market Size to Exceed USD 233.8 Billion by 2035

Global Canned Food Market Size, Share Analysis By Product Type (Canned Seafood, Canned Meat, Canned Fruits and Vegetables, Canned Ready Meals, Others), By Type (Conventional, Organic), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Frozen Food Market Size to Exceed USD 596.6 Billion by 2035

Global Frozen Food Market Size, Share Analysis By Product (Frozen Desserts, Frozen Meals, Meat/Poultry/Seafood, Fruits and Vegetables, Snacks, Baked Goods), By Freezing Technology (Blast Freezing, Belt Freezing, Individual Quick Freezing, Others), By Distribution Channel (Foodservice, Retail), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Ready-to-Eat Food Market to Exceed USD 846.5 Billion by 2035

Global Ready-to-Eat Food Market Size, Share Analysis By Product Type (Meat/Poultry, Vegetarian, Cereal-Based, Others), By Packaging (Frozen/Chilled, Canned, Retort, Others), By Distribution Channel (Hypermarkets, Convenience Stores, Online, Others), By End User (Residential, Foodservice, Institutional), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035