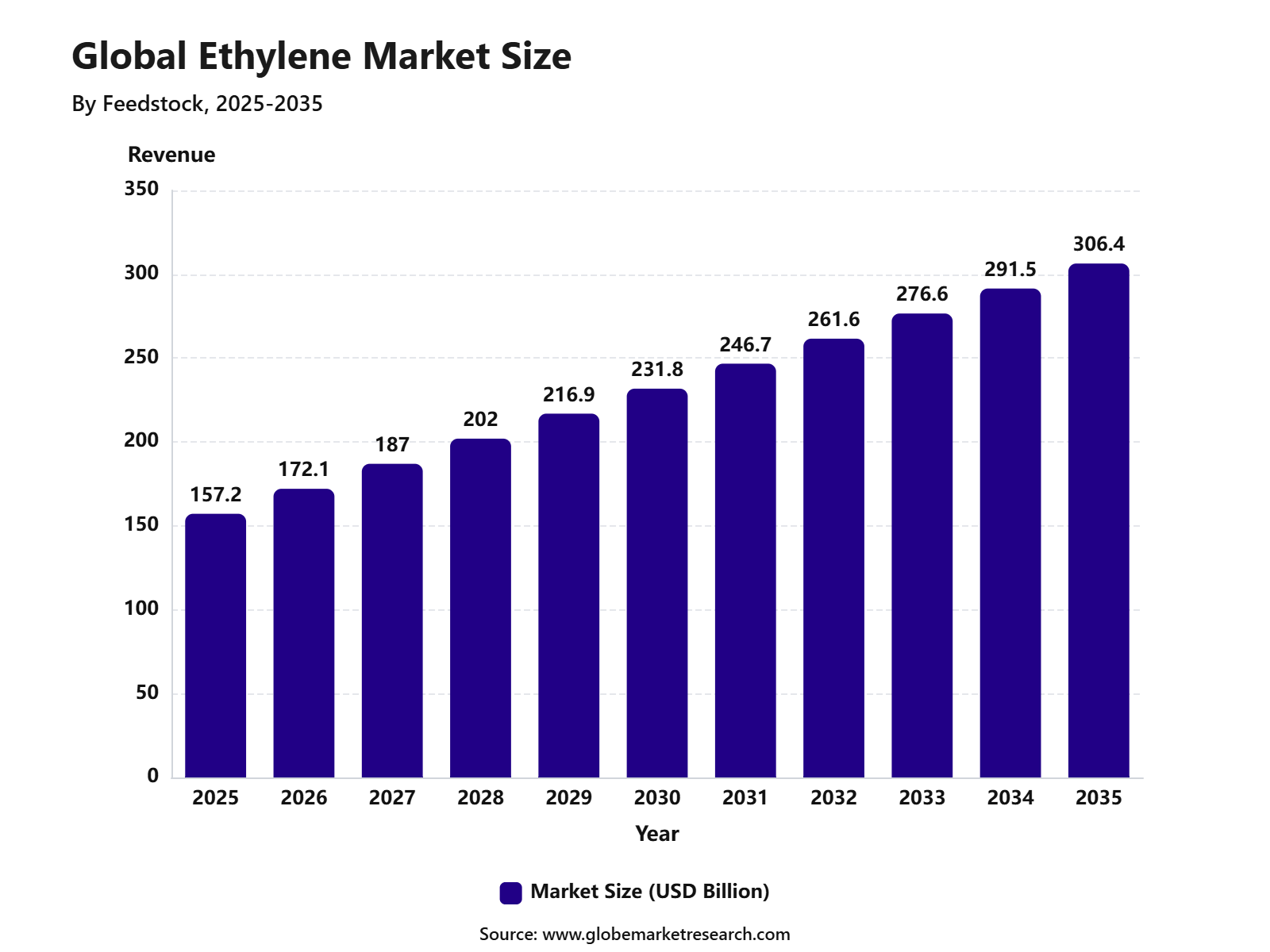

Revenue, 2025

$ 157.2 Bn

Forecast, 2035

$ 306.4 Bn

CAGR, 2025-2035

6.9%

Report Coverage

Global

Market Size and Forecast

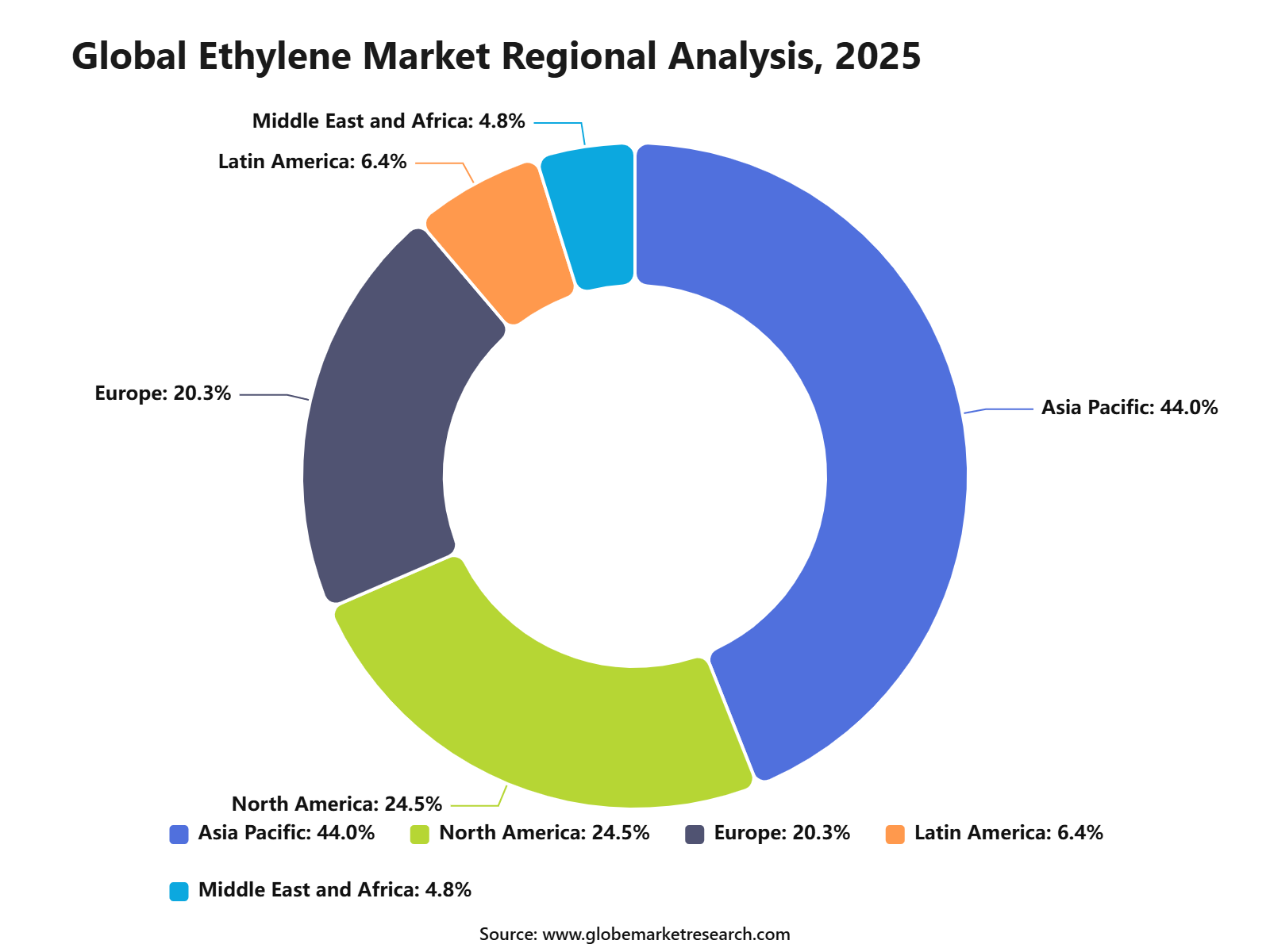

The Global Ethylene Market was worth USD 157.2 billion in 2025 and is expected to reach USD 306.4 billion by 2035, growing at a CAGR of 6.9% from 2025 to 2035. Asia Pacific held the largest regional share of 44.0% in 2025, supported by strong petrochemical production, high demand for plastics, large manufacturing capacity, and expanding consumption across packaging, construction, automotive, textiles, and consumer goods industries.

The Ethylene Market includes the production and use of ethylene as a key petrochemical building block for several downstream products. It is mainly used to produce polyethylene, ethylene oxide, ethylene dichloride, ethylbenzene, alpha olefins, and other chemical intermediates. The market is closely linked with crude oil, natural gas liquids, steam crackers, refinery integration, polymer manufacturing, and end-use industries that rely on lightweight and durable plastic materials.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains steady as ethylene demand continues to rise across packaging, infrastructure, transportation, and industrial applications. Growth can be attributed to increasing use of polyethylene in films, containers, pipes, wires, cables, and molded products. The expansion of petrochemical complexes, rising demand for flexible packaging, and higher consumption of ethylene-based derivatives are expected to support long-term market growth.

Key Market Insights

Naphtha led the feedstock segment with 44.1% share, supported by its wide use in steam cracking, strong availability across refining systems, and suitability for large-scale ethylene production.

Polyethylene accounted for 62.5% share by derivative, driven by strong demand in films, containers, pipes, molded products, and other plastic applications.

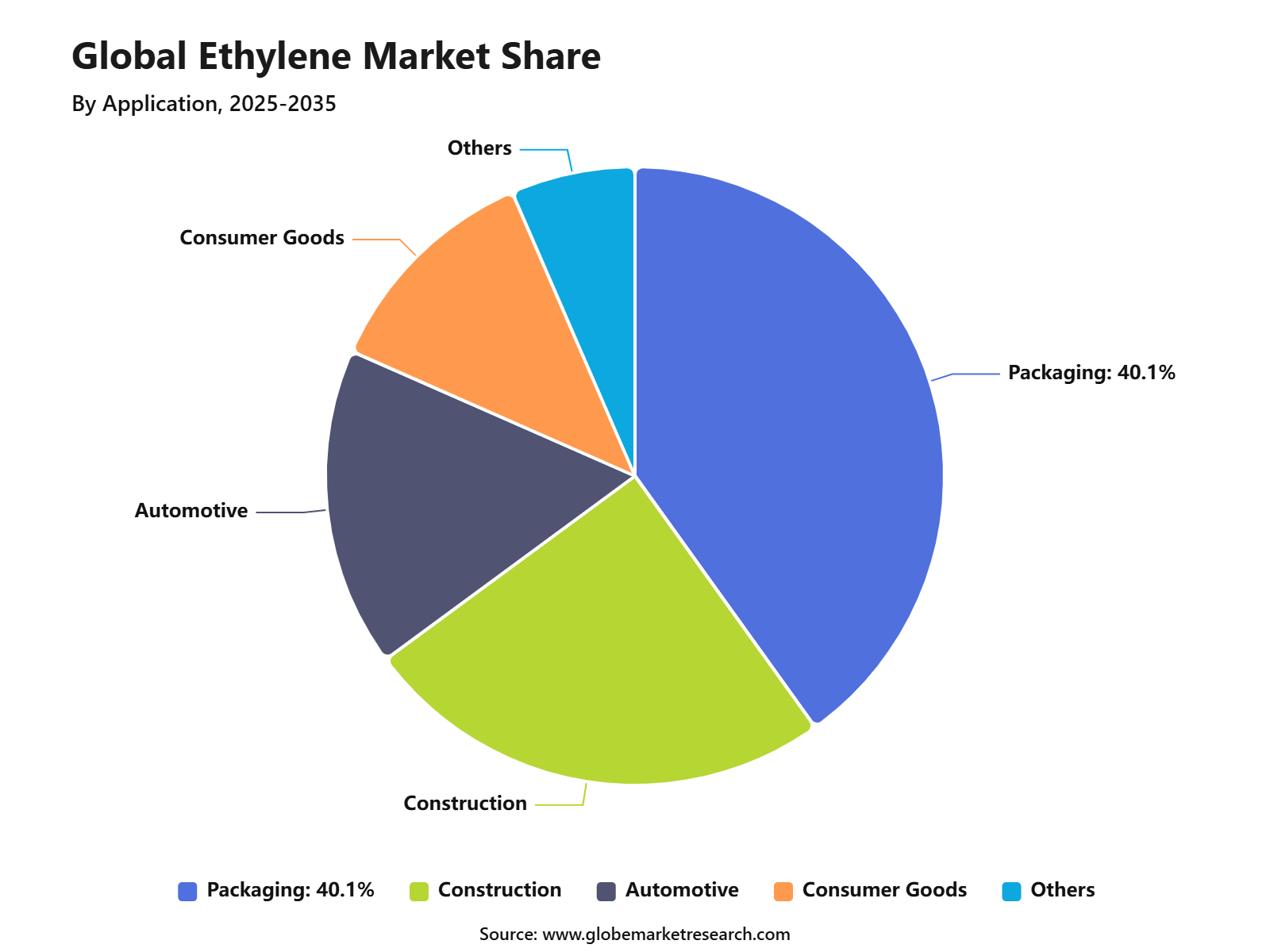

Packaging held 40.1% share by application, supported by rising use of polyethylene-based materials in flexible packaging, food packaging, consumer goods, and industrial packaging.

Asia Pacific led the ethylene market with 44.0% share, supported by strong petrochemical production, rising packaging demand, expanding manufacturing activity, and high consumption across China, India, and Southeast Asia

Go-To-Market-Strategy

Customer acquisition in the ethylene market is mainly controlled by supply reliability, feedstock advantage, contract pricing, logistics access, and downstream integration. Ethylene is difficult to transport over long distances in normal trade, so buyers usually prefer suppliers with nearby crackers, pipeline access, port terminals, or integrated derivative units. This makes customer acquisition more relationship-based than campaign-based, with long-term contracts commonly used by polyethylene, ethylene oxide, ethylene dichloride, ethylbenzene, and glycol producers.

The customer acquisition cost is high at the beginning because producers must prove stable output, product consistency, delivery security, safety compliance, and ability to handle cyclical demand. Once a buyer is secured, retention can remain strong because ethylene customers need continuous feedstock flow for large downstream plants. The economics are supported by active downstream resin demand, as U.S. production of major plastic resins reached 8.9 billion pounds in April 2026, up 11.2% from April 2025, while year-to-date production reached 35.2 billion pounds, up 6.4% year over year.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is strongest across polyethylene, packaging plastics, construction materials, automotive components, consumer goods, synthetic rubber, and industrial intermediates. Ethylene demand is closely linked with plastics and resins because ethane is mainly cracked into ethylene, which is then used to make plastics, resins, and synthetic rubber. The U.S. Energy Information Administration forecast U.S. ethane net exports to rise 14% in 2025 and 16% in 2026, supported by global petrochemical feedstock demand and new export capacity.

Asia remains a major revenue center because China and other Asian economies continue to add petrochemical capacity and consume large volumes of polymers for packaging, infrastructure, electronics, and consumer products. The IEA reported that emerging and developing economies accounted for nearly all oil demand growth in 2025, with Asia Pacific adding 360 thousand barrels per day and China adding 220 thousand barrels per day. This supports ethylene-linked feedstock demand, although naphtha, LPG, and ethane use slowed in 2025 due to trade disruption and weaker petrochemical margins.

Financial Impact

The financial impact of ethylene is highly linked to cracker utilization, feedstock spread, derivative margins, and energy costs. Ethane-based producers can gain margin advantages when ethane is cheaper than naphtha, while naphtha-based producers are more exposed to crude oil and refinery economics. This creates a clear regional profit gap, especially between North America, the Middle East, Europe, and parts of Asia.

Revenue stability improves when ethylene producers are integrated into polyethylene, ethylene oxide, glycol, or PVC value chains. Integration helps producers capture more value beyond basic ethylene sales and reduces exposure to spot-price volatility. This is important because petrochemicals are expected to remain a major source of oil demand growth, with the IEA stating that petrochemicals could account for over one-third of oil demand growth to 2030 and nearly half to 2050.

For Europe, the financial outlook is more pressured. Cefic reported that EU27 chemical capacity utilization remains around 74%, chemical production declined 3.2% year over year in the first quarter of 2026, and exports fell by EUR 4.6 billion, or 12.4%. These figures show weaker operating leverage for European ethylene and polymer producers, especially where energy and feedstock costs remain above competing regions.

Feedstock Analysis

Naphtha led the Ethylene Market with 44.1% share, supported by its strong use as a major feedstock in steam crackers, especially across refinery-integrated petrochemical complexes. It is widely used in regions where crude oil refining and petrochemical production are closely linked, allowing producers to generate ethylene along with other valuable co-products such as propylene, butadiene, and aromatics.

The growth of this segment can be attributed to the broad availability of naphtha in refinery value chains and its importance in flexible cracker operations. Naphtha cracking remains important in Asia Pacific and Europe because it supports a wider petrochemical product slate compared with lighter feedstocks. Naphtha is expected to remain a key feedstock where producers need flexibility across olefins and aromatics production. However, margins may remain sensitive to crude oil prices, refinery economics, energy costs, and competition from ethane-based production in regions with low-cost natural gas liquids.

Derivative Analysis

Polyethylene accounted for 62.5% share, making it the leading derivative segment in the Ethylene Market. Ethylene is the main building block used to produce polyethylene grades such as HDPE, LDPE, and LLDPE, which are widely used in packaging, films, containers, pipes, household goods, wire insulation, and industrial products. The dominance of polyethylene can be linked to its light weight, durability, flexibility, moisture resistance, and cost efficiency.

It remains one of the most used plastics because it can be processed into rigid, flexible, and film-based products for both consumer and industrial applications. Polyethylene demand is expected to remain closely tied to packaging, construction, agriculture, consumer goods, and infrastructure-related applications. Producers are also focusing on recyclable polyethylene, mono-material packaging, recycled-content grades, and lower-carbon production routes to respond to sustainability requirements.

Application Analysis

Packaging led the application segment with 40.1% share, supported by the wide use of ethylene-based polymers in food packaging films, bottles, pouches, bags, caps, containers, liners, and protective packaging. Polyethylene packaging is preferred because it provides moisture protection, durability, light weight, sealability, and product safety.

The growth of this segment can be attributed to rising demand for packaged food, beverages, e-commerce packaging, household products, personal care products, and industrial packaging. Ethylene-based packaging materials help extend product shelf life, reduce breakage, improve handling, and support efficient distribution.

Packaging is expected to remain a major application area, although sustainability pressure is reshaping material choices. Demand will continue for flexible films, high-barrier packaging, recyclable polyethylene formats, lightweight containers, and packaging solutions that reduce material use while maintaining product protection.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

Asia Pacific led the Ethylene Market with 44.0% share, supported by strong petrochemical production, high plastics consumption, large packaging demand, and expanding manufacturing activity. China, India, Japan, South Korea, and Southeast Asia remain major demand centers for ethylene derivatives used in packaging, construction, automotive, textiles, consumer goods, and electronics.

The region’s leadership can be attributed to its large population base, rising urbanization, growing packaged goods consumption, and strong downstream conversion industry. Asia Pacific also has significant refinery and petrochemical integration, which supports naphtha-based ethylene production and large-scale derivative manufacturing.

Asia Pacific is expected to remain the leading regional market as demand grows for polyethylene, ethylene oxide, ethylene dichloride, and other ethylene-based products. Future opportunities are likely to remain strong in packaging films, consumer goods, infrastructure materials, specialty chemicals, and sustainable polymer solutions.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +2.1% | Asia Pacific, 44.0% share in 2025 | Leads consumption volume. |

China petrochemical expansion | +1.4% | China | Drives regional capacity. |

North America shale-based feedstock advantage | +1.1% | U.S. and Canada | Supports cost efficiency. |

Middle East integrated petrochemical growth | +0.9% | Saudi Arabia, UAE, Qatar | Strengthens export supply. |

Europe circular plastics transition | +0.7% | Germany, France, Netherlands, UK | Supports low-carbon shift. |

Risk Factors & Market Barriers

Regulatory & Compliance Risks

Ethylene producers face rising compliance pressure from carbon policy, plastics regulation, environmental permitting, emissions rules, and circular economy requirements. Steam cracking is energy-intensive, and regulators are increasing focus on fossil feedstock use, plant emissions, plastic waste, and product lifecycle impact. UNEP stated that the global plastic pollution treaty process is intended to address the full life cycle of plastics, including production, design, and disposal, which may affect future demand, product design, and compliance requirements for ethylene derivatives.

Plastic waste policy is another major risk because polyethylene and other ethylene derivatives are widely used in packaging and disposable applications. OECD data shows that without stronger policy action, plastics production and use could rise 70% from 435 million tonnes in 2020 to 736 million tonnes in 2040, while only 6% would come from recycled sources. This creates both demand opportunity and regulatory exposure, as governments may increase plastic taxes, recycled content rules, waste controls, and restrictions on single-use formats.

Europe shows how regulation and circularity can reshape the downstream market. Plastics Europe reported that 15.8%, or 8.7 million tonnes, of Europe’s total plastics production was circular in 2024, but circular production growth slowed from 13.6% in 2022 to 1.2% in 2024. This indicates that circular plastics are becoming strategically important, but high costs and weak demand can slow adoption and affect virgin ethylene derivative demand.

Market Adoption Barriers

Market adoption barriers are mainly linked to oversupply, price volatility, feedstock disruption, transport limits, and weak margins in some regions. Ethylene cannot be treated like a simple global commodity because safe storage and movement require special infrastructure. As a result, new suppliers must secure local pipelines, tankage, shipping access, derivative outlets, and reliable offtake agreements before capacity can be monetized.

Feedstock cost is one of the largest barriers for new entrants. In Europe, natural gas is both an energy source and an industrial feedstock, and Cefic reported that the EU chemical industry consumed 324 TWh of natural gas and 149 TWh of electricity in 2023. The same source stated that EU gas prices were around four times higher than U.S. prices over the past year, creating pressure on site economics, investment decisions, and competitiveness.

Adoption of new ethylene capacity can also be slowed by derivative market weakness. When polyethylene, glycol, PVC, or styrene margins are weak, buyers may reduce spot purchases and crackers may cut operating rates. For this reason, the most resilient ethylene producers are expected to be those with low-cost feedstock, integrated downstream assets, stable logistics, and clear exposure to packaging, infrastructure, healthcare, automotive, and consumer product demand.

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Naphtha remains key feedstock | +1.5% | Asia Pacific, Europe | Supports cracker operations. |

Polyethylene leads derivative demand | +1.7% | Global | Drives ethylene consumption. |

Packaging remains largest application | +1.4% | Asia Pacific, North America, Europe | Supports stable usage. |

Shift toward circular plastics | +1.0% | Europe, North America, developed Asia | Encourages recycling integration. |

Capacity expansion in Asia Pacific | +1.2% | China, India, Southeast Asia | Strengthens regional supply. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Petrochemical Producers | +1.6% | Global | Expands ethylene capacity. |

Polymer Manufacturers | +1.4% | Asia Pacific, North America, Europe | Drives derivative demand. |

Refining and Integrated Energy Companies | +1.1% | Middle East, Asia Pacific, U.S. | Improves feedstock access. |

Infrastructure and Industrial Investors | +0.9% | Petrochemical hubs | Supports plant expansion. |

Sustainability and Recycling Investors | +0.8% | Europe, North America, Asia Pacific | Builds circular value chains |

Segment Covered in the Report

By Feedstock

Naphtha

Ethane

Propane

Butane

Others

By Derivative

Polyethylene

Ethylene Oxide

Ethylene Dichloride

Ethylbenzene

Others

By Application

Packaging

Construction

Automotive

Consumer Goods

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for polyethylene | +1.8% | Asia Pacific, North America, Europe | Drives core consumption. |

Growth in packaging applications | +1.5% | Asia Pacific, Europe, North America | Supports resin demand. |

Expansion of petrochemical production | +1.3% | China, India, Middle East, U.S. | Increases ethylene use. |

Rising demand from construction materials | +1.1% | Asia Pacific, Middle East, Latin America | Supports downstream growth. |

Growth in consumer goods manufacturing | +0.9% | Asia Pacific, North America, Europe | Expands plastic usage. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Volatility in naphtha and feedstock prices | -0.9% | Asia Pacific, Europe, Middle East | Pressures margins. |

Environmental pressure on plastic use | -0.8% | Europe, North America, developed Asia | Limits demand growth. |

High capital cost of crackers | -0.7% | Global producers | Restricts new capacity. |

Carbon emission regulations | -0.6% | Europe, U.S., Japan, South Korea | Raises compliance cost. |

Supply-demand imbalance risk | -0.5% | Global petrochemical hubs | Affects pricing stability. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of polyethylene capacity | +1.7% | Asia Pacific, Middle East, North America | Builds downstream demand. |

Growth in flexible packaging | +1.4% | Asia Pacific, Europe, Latin America | Supports resin consumption. |

Bio-based and low-carbon ethylene development | +1.1% | Europe, North America, Japan | Supports sustainability shift. |

Demand from automotive and construction plastics | +1.0% | Asia Pacific, North America, Europe | Expands application scope. |

Integration of refining and petrochemical assets | +0.9% | Middle East, China, India | Improves cost efficiency. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Managing emissions from steam cracking | -0.8% | Global production sites | Raises operating burden. |

Feedstock supply uncertainty | -0.7% | Asia Pacific, Europe | Impacts production planning. |

Plastic waste and recycling pressure | -0.6% | Europe, North America, Asia Pacific | Affects product demand. |

Intense competition among producers | -0.5% | Global petrochemical market | Reduces margin strength. |

Complex logistics for downstream derivatives | -0.4% | Global | Impacts supply efficiency. |

Recent Developments

In January 2026, SABIC signed agreements to divest its European Petrochemicals business to AEQUITA for USD 500.0 million. The assets produce ethylene, propylene, LDPE, LLDPE, HDPE, PP, and compounds across UK and German sites.

In May 2026, LyondellBasell reported Q1 EBITDA of USD 568.0 million, or USD 615.0 million excluding items. Olefins and Polyolefins Americas EBITDA doubled sequentially, supported by stronger integrated polyethylene margins and higher contract prices.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 157.2 Billion |

Forecast Revenue (2035) | USD 306.4 Billion |

CAGR (2025-2035) | 6.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Feedstock (Naphtha, Ethane, Propane, Butane, Others), By Derivative (Polyethylene, Ethylene Oxide, Ethylene Dichloride, Ethylbenzene, Others), By Application (Packaging, Construction, Automotive, Consumer Goods, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | ExxonMobil Corporation, SABIC, Dow Inc., Shell plc, LyondellBasell Industries N.V., INEOS Group, Sinopec, TotalEnergies SE, Reliance Industries Limited, Formosa Plastics Corporation |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

ExxonMobil Corporation

SABIC

Dow Inc.

Shell plc

LyondellBasell Industries N.V.

INEOS Group

Sinopec

TotalEnergies SE

Reliance Industries Limited

Formosa Plastics Corporation

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Semiconductor Chemicals Market Size to Exceed USD 75.6 Bn by 2035

Global Semiconductor Chemicals Market Size, Share Analysis By Chemical Type (Acid and Base Chemicals, High-Performance Polymers, Adhesives, Solvents, Others), By Purity Level (4N, 5N, 6N and Above), By End Use (Integrated Circuits, Printed Circuit Boards, Discrete Semiconductors, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035