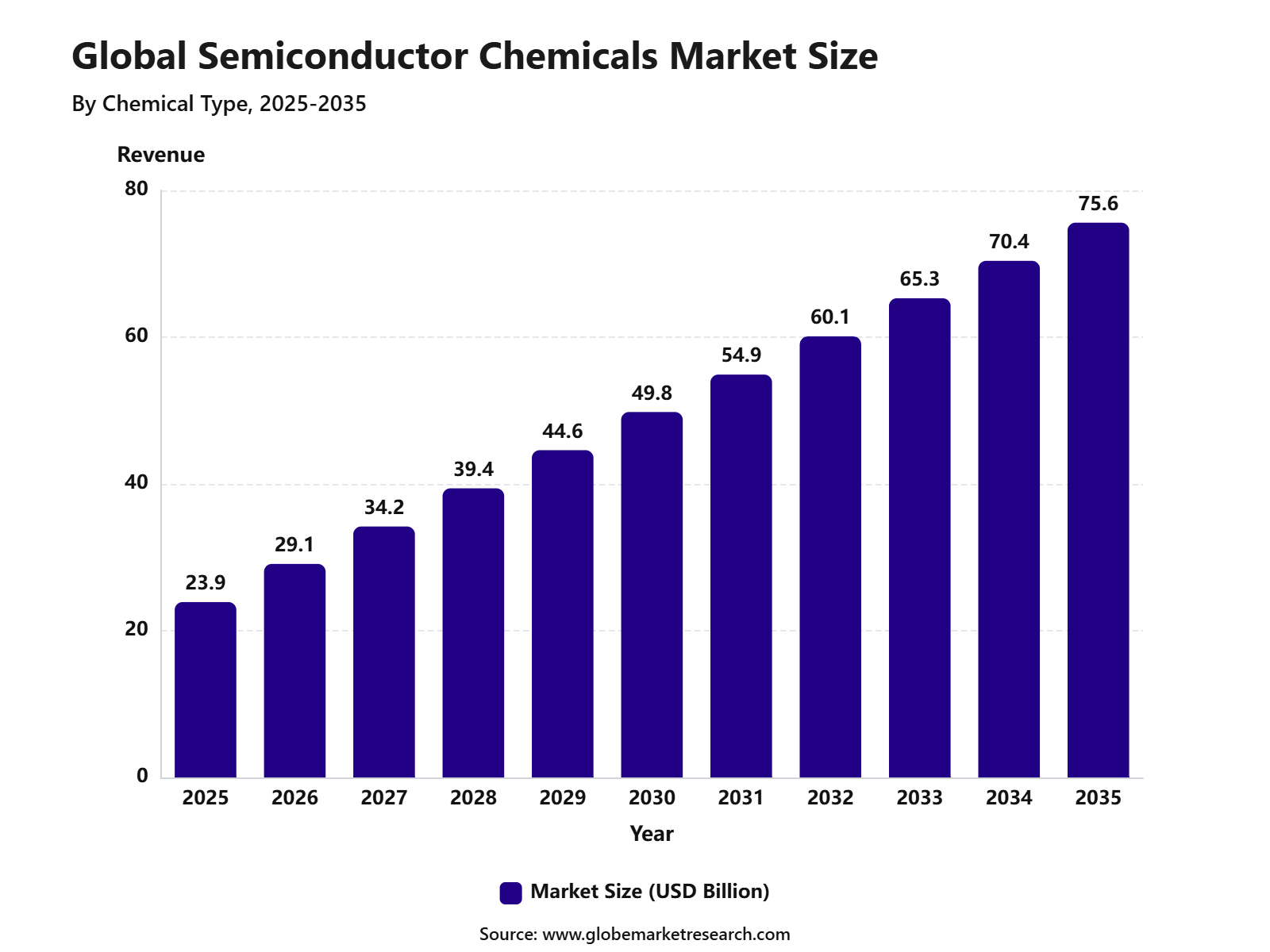

Revenue, 2025

$ 23.9 Bn

Forecast, 2035

$ 75.6 Bn

CAGR, 2025-2035

12.2%

Report Coverage

Global

Market Size and Forecast

The Global Semiconductor Chemicals Market was worth USD 23.9 billion in 2025 and is expected to reach USD 75.6 billion by 2035, growing at a CAGR of 12.2% from 2025 to 2035. Asia Pacific held the largest regional share of 36.9% in 2025, supported by large semiconductor manufacturing capacity, strong chip fabrication activity, expanding electronics production, and continuous investment in wafer processing facilities across China, Taiwan, South Korea, Japan, and Southeast Asia.

The Semiconductor Chemicals Market includes high-purity chemicals used in chip manufacturing, wafer cleaning, etching, photolithography, deposition, polishing, and surface treatment processes. These chemicals include acids, bases, solvents, photoresists, developers, wet chemicals, CMP slurries, and specialty gases used across integrated circuits, printed circuit boards, sensors, memory chips, and advanced semiconductor devices. The market is closely linked with foundries, outsourced semiconductor assembly and testing companies, chemical suppliers, and electronics manufacturers.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFFor instance, In June 2025, the Semiconductor Industry Association reported that global semiconductor sales reached USD 57.0 billion in April 2025. This showed a 2.5% increase from USD 55.6 billion recorded in March 2025 and a strong 22.7% rise compared with USD 46.4 billion in April 2024. The figures indicate steady demand across the semiconductor value chain, supported by continued use of chips in AI, data centers, consumer electronics, automotive systems, industrial equipment, and connected devices.

The market outlook remains strong as demand for advanced chips continues to rise across artificial intelligence, electric vehicles, data centers , smartphones, industrial automation, and connected devices. Growth can be attributed to higher semiconductor production, increasing use of smaller node technologies, rising purity requirements, and the need for reliable chemical supply chains. The expansion of local chip manufacturing programs, advanced packaging, and high-performance electronics is expected to support long-term demand for semiconductor chemicals.

Key Market Insights

Acid and base chemicals led the chemical type segment with 42.0% share , supported by their wide use in wafer cleaning, etching, surface preparation, and semiconductor fabrication processes.

5N purity level accounted for 47.8% share , driven by strong demand for ultra-high-purity chemicals that help reduce contamination and improve chip production quality.

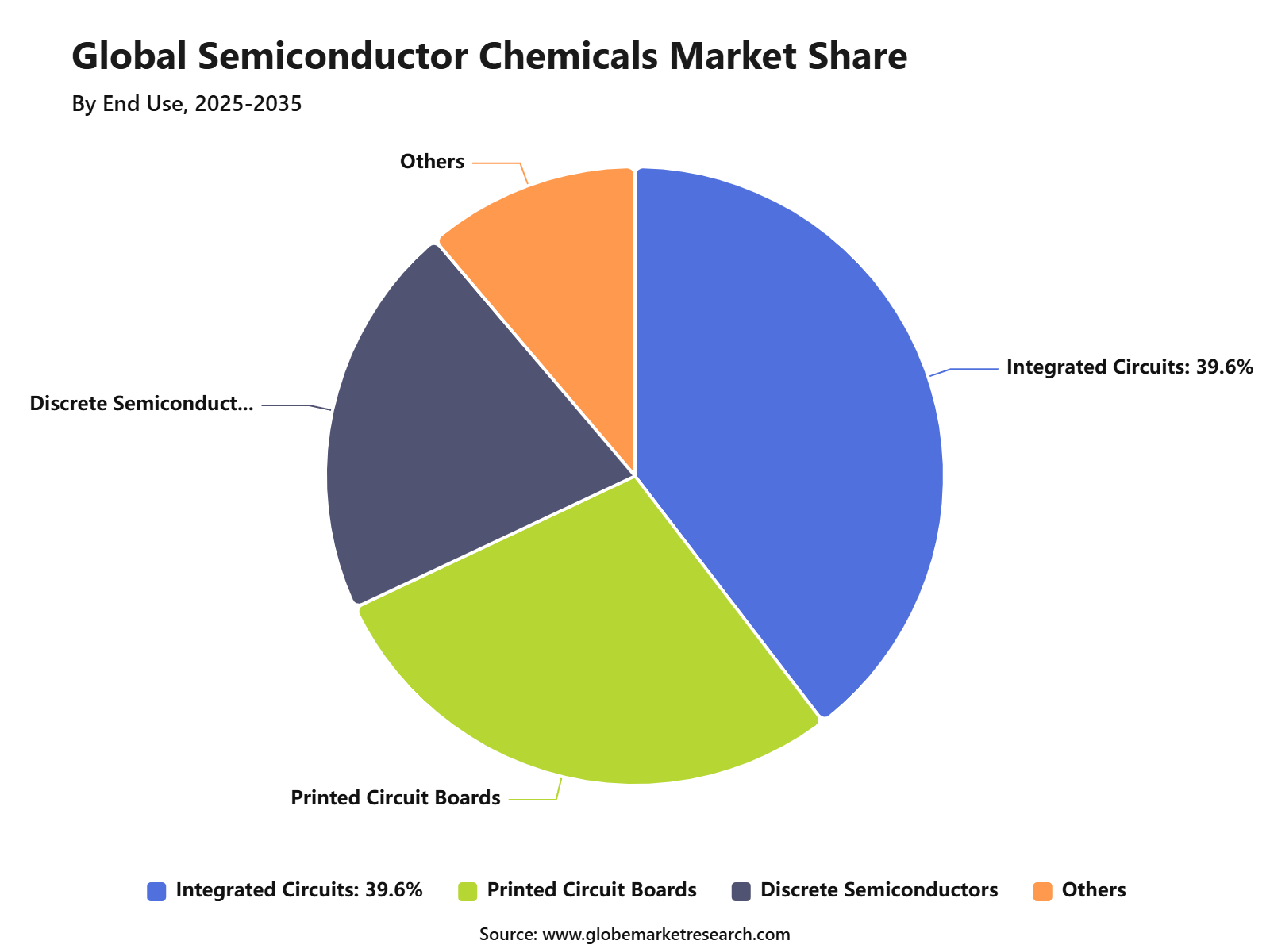

Integrated circuits held 39.6% share by end use, supported by rising demand for advanced chips used in consumer electronics, data centers, automotive systems, and industrial devices.

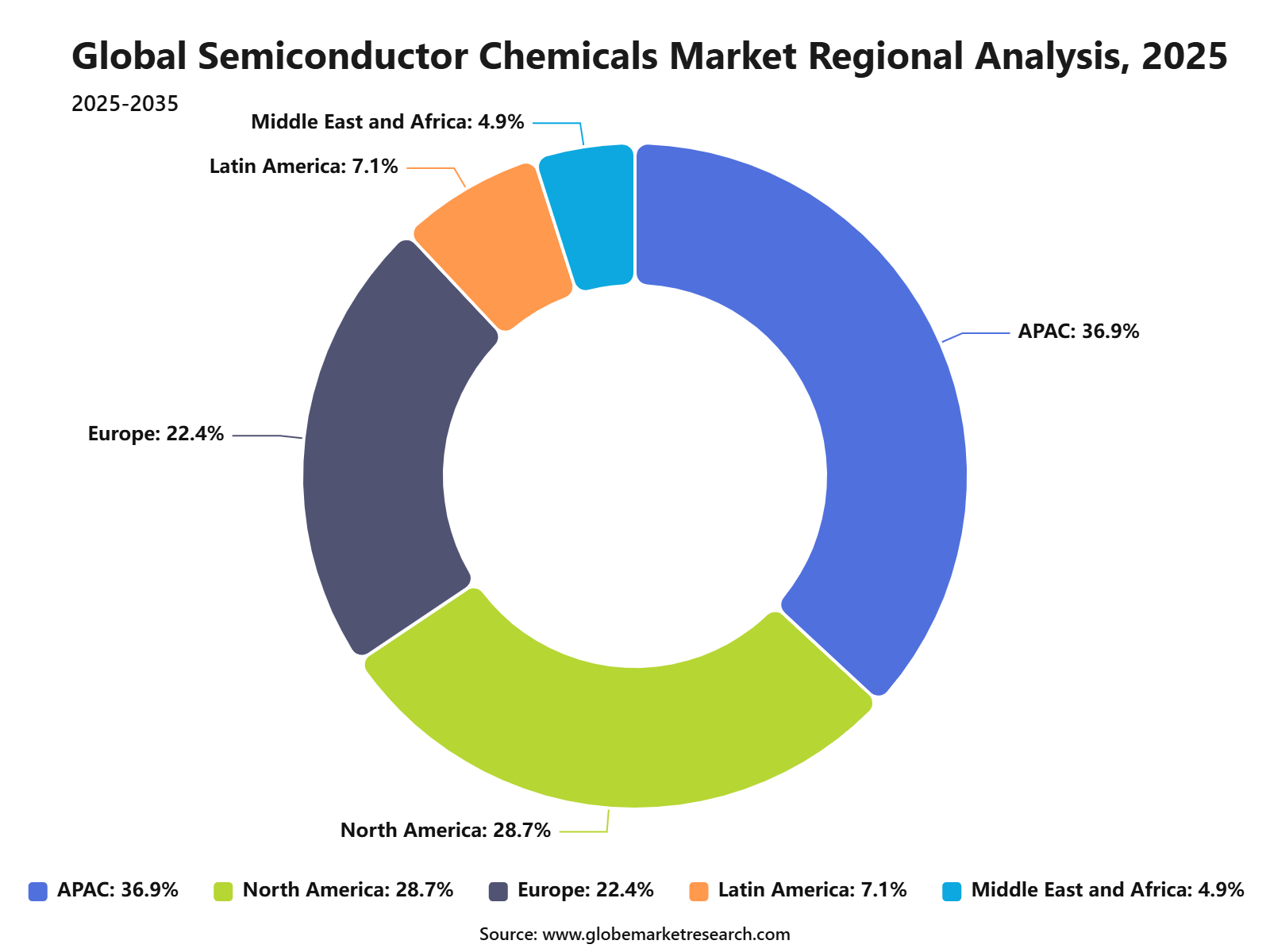

Asia Pacific led the semiconductor chemicals market with 36.9% share , supported by large-scale chip manufacturing, strong electronics production, and expanding semiconductor fabrication capacity.

AI-Driven Semiconductor Chemical Manufacturing

Artificial intelligence is becoming an important production tool in semiconductor chemical manufacturing, especially as chip fabrication becomes more complex and chemical purity requirements become tighter. Semiconductor chemicals such as wet chemicals, photoresists, solvents, etchants, CMP slurries, specialty gases, and cleaning agents must meet strict quality, consistency, and contamination-control standards. This pressure is rising because global semiconductor materials revenue reached a record USD 73.2 billion in 2025, while wafer fabrication materials revenue increased to USD 45.8 billion , supported by stronger demand for lithography-related materials and wet chemicals.

AI is mainly used to improve process stability, batch quality, and yield control. In chemical production lines, AI models can analyze sensor data from reactors, filtration systems, distillation units, blending tanks, and purification equipment. This helps manufacturers detect early signs of impurity drift, particle contamination, moisture variation, and abnormal temperature or pressure behavior before the chemical batch moves to customer qualification. For semiconductor-grade chemicals, this is critical because even small contamination levels can affect wafer yield and device performance.

AI is expected to gain stronger adoption as fabs require more advanced materials and tighter supplier control. SEMI reported that worldwide 300mm fab equipment spending is expected to increase 18% to USD 133 billion in 2026 and 14% to USD 151 billion in 2027, driven by AI chip demand and regional semiconductor self-sufficiency programs. Higher fab investment increases the need for reliable chemical supply, advanced purity control, and faster process qualification, making AI a practical tool for semiconductor chemical manufacturers.

Go-To-Market-Strategy

The go-to-market strategy for the semiconductor chemicals market should focus on direct supply agreements with wafer fabs, foundries, integrated device manufacturers, outsourced semiconductor assembly and testing companies, and semiconductor equipment suppliers. Demand is mainly linked to wet chemicals, solvents, photoresists, CMP slurries, specialty gases, deposition precursors, cleaning chemicals, and surface preparation materials. SEMI’s materials coverage for 2026 includes wafer fab materials, bulk wet chemicals, electronic specialty gases, CMP technologies, advanced cleaning, and advanced thin-film materials, showing that chemical demand is spread across several critical fab process steps.

Sales economics are shaped by purity level, contamination control, qualification time, safety documentation, fab proximity, packaging quality, and long-term supply reliability. Semiconductor buyers do not switch chemical suppliers quickly because even small contamination can affect wafer yield, reliability, and customer qualification. Supplier success depends on tight specifications, lot-to-lot consistency, local technical support, and the ability to deliver high-purity chemicals in drums, bulk containers, cylinders, and fab-ready distribution systems.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities are strongest across wafer fabrication materials because advanced nodes, AI chips, high-bandwidth memory, and advanced packaging require more process steps and tighter chemical control. SEMI reported in May 2026 that global semiconductor materials revenue reached a record USD 73.2 billion in 2025, with wafer fabrication materials rising 5.4% to USD 45.8 billion and packaging materials growing 9.3% to USD 27.4 billion . Taiwan remained the largest semiconductor materials consumer at USD 21.7 billion , followed by China at USD 15.6 billion and South Korea at USD 11.2 billion , showing that Asia remains the largest revenue concentration for semiconductor chemical suppliers.

Financial Impact

The financial impact is expected to remain positive for suppliers that can secure long-term fab contracts, pass strict qualification tests, and support local supply chains near major chip clusters. SEMI reported that worldwide 300mm fab equipment spending is expected to rise 18% to USD 133 billion in 2026 and 14% to USD 151 billion in 2027, while Q1 2026 silicon wafer shipments increased 13.1% year over year to 3,275 million square inches. Higher wafer starts, advanced-node expansion, and stronger memory investment can improve chemical volume demand, but margins will depend on raw material availability, energy costs, purification capacity, waste treatment, and customer-specific quality certification.

Chemical Type Analysis

Acid and base chemicals led the Semiconductor Chemicals Market with 42.0% share , supported by their critical use in wafer cleaning, wet etching, surface preparation, residue removal, and process conditioning. These chemicals are used throughout semiconductor fabrication because even small contamination levels can affect wafer yield and device performance.

The growth of this segment can be attributed to rising wafer complexity and increasing process steps in advanced semiconductor manufacturing. Chemicals such as sulfuric acid, nitric acid, hydrofluoric acid, hydrochloric acid, ammonium hydroxide, and other high-purity acids and bases are widely used in front-end and back-end processes.

Demand is expected to remain strong as chipmakers expand production for AI chips, memory, logic devices, power semiconductors, sensors, and automotive electronics. Suppliers that provide stable purity, tight contamination control, safe handling, and reliable delivery are likely to remain important to semiconductor fabs.

Purity Level Analysis

5N purity level held 47.8% share , driven by the need for extremely low impurity levels in semiconductor chemical processing. 5N purity refers to 99.999% purity, which is important because trace metals, particles, and ionic contaminants can create defects during wafer fabrication. The dominance of this segment is supported by the strict quality requirements of advanced integrated circuit production.

High-purity chemicals are required in cleaning, deposition support, lithography-related steps, etching, chemical mechanical polishing, and surface treatment processes. The 5N purity segment is expected to remain important as device geometries become smaller and process tolerances become tighter. Demand will be supported by advanced nodes, high-performance chips, memory devices, and semiconductor fabs that require stable chemical quality to protect yield and reliability.

End Use Analysis

Integrated circuits accounted for 39.6% share of the Semiconductor Chemicals Market, making them the leading end-use segment. IC manufacturing requires large volumes of specialty chemicals for wafer preparation, cleaning, etching, polishing, deposition support, photoresist processing, and packaging-related steps. The growth of this segment can be linked to rising demand for chips used in smartphones, data centers, electric vehicles, industrial automation, consumer electronics, telecommunications, and AI systems.

Integrated circuits are becoming more complex, which increases the need for higher-purity and application-specific chemicals. Integrated circuits are expected to remain the largest end-use area because they represent the core output of semiconductor fabs. Strong demand is likely to continue for wet chemicals, photoresist chemicals, CMP chemicals, cleaning chemicals, and high-purity solvents used in IC production.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

Asia Pacific led the Semiconductor Chemicals Market with 36.9% share , supported by the region’s strong semiconductor manufacturing base, large fab concentration, and high demand for wafer processing chemicals. Taiwan, South Korea, China, and Japan remain central to global chip production, which supports strong consumption of high-purity process chemicals. The region’s dominance can be attributed to advanced foundry capacity, memory chip production, outsourced semiconductor assembly and testing, and continued fab investment.

Asia Pacific also benefits from established electronics supply chains, skilled manufacturing ecosystems, and strong demand from consumer electronics, automotive, industrial, and data center applications. Asia Pacific is expected to remain the leading regional market as semiconductor production expands and process complexity increases. Opportunities are likely to remain strong in acid and base chemicals, 5N purity chemicals, integrated circuit manufacturing chemicals, CMP materials, and advanced wafer cleaning solutions.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +3.6% | Asia Pacific, 36.9% share in 2025 | Leads fab concentration. |

North America chip manufacturing expansion | +2.4% | U.S. | Supports local chemical demand. |

Europe semiconductor capacity growth | +1.9% | Germany, France, Netherlands, Ireland | Builds regional supply. |

Japan and South Korea material strength | +2.2% | Japan, South Korea | Supports specialty chemicals. |

India emerging semiconductor ecosystem | +1.3% | India | Creates future demand. |

Top Two Opportunities for Semiconductor Chemicals Market

Expand high-purity chemicals for advanced fabs and AI-driven chip production

The strongest opportunity is the supply of ultra-high-purity acids, bases, solvents, photoresist materials, deposition precursors, and CMP chemicals for advanced semiconductor fabs. Global chip demand is rising sharply, with SIA reporting April 2026 semiconductor sales of USD 110.5 billion , up 93.9% year over year, while WSTS projected annual semiconductor sales to reach USD 1.5 trillion in 2026. This growth is being supported by AI infrastructure, accelerated computing, memory, and advanced logic demand, all of which require tighter chemical purity, better contamination control, and more stable process performance.

Chemical suppliers should prioritize materials used in 300mm wafer processing, EUV lithography, advanced cleaning, etching, deposition, and planarization. SEMI reported that global 300mm fab equipment spending is expected to increase 18% to USD 133 billion in 2026 and reach USD 151 billion in 2027, supported by AI chips, advanced nodes, and regional fab expansion. This creates a clear opportunity for chemical producers that can meet strict purity requirements, provide local technical support, and qualify materials with leading foundries and integrated device manufacturers.

Develop PFAS-free, low-emission, and circular semiconductor chemical solutions

The second major opportunity is the development of safer and more sustainable semiconductor chemicals. PFAS materials are still used in several semiconductor processes because of their heat resistance, chemical stability, and process performance, but regulatory and environmental pressure is increasing. Imec has reported early progress in PFAS-free chemically amplified resists for EUV lithography, with initial tests showing comparable patterning performance, while further work is being extended to rinses, underlayers, and metal-oxide resists.

This opportunity is gaining stronger policy support. In June 2026, the U.S. Department of Commerce announced a USD 500 million CHIPS R&D award to accelerate AI-driven semiconductor materials discovery, including PFAS-free process chemicals, advanced catalysts, rare earth-free materials, and other critical inputs for semiconductor manufacturing. This shows that chemical innovation is now being treated as a strategic supply chain priority, not only as a compliance issue.

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Acid and base chemicals dominance | +2.8% | Asia Pacific, North America, Europe | Leads process demand. |

Rising adoption of 5N purity level | +2.5% | Advanced fabs | Supports precision production. |

Integrated circuits remain key end use | +2.3% | Global semiconductor industry | Drives stable usage. |

Shift toward advanced packaging | +1.9% | Taiwan, South Korea, Japan, U.S. | Expands specialty demand. |

Localized semiconductor supply chains | +1.7% | U.S., Europe, India, China | Supports regional production. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Specialty Chemical Manufacturers | +2.8% | Global | Expands high-purity capacity. |

Semiconductor Material Suppliers | +2.4% | Asia Pacific, U.S., Europe | Supports fab demand. |

Foundries and Chipmakers | +2.1% | Taiwan, South Korea, U.S., China | Drives direct consumption. |

Private Equity Firms | +1.6% | Advanced manufacturing regions | Supports capacity scaling. |

Government-Backed Industrial Investors | +1.5% | U.S., Europe, India, Japan | Enables supply localization. |

Segment Covered in the Report

By Chemical Type

Acid and Base Chemicals

High-Performance Polymers

Adhesives

Solvents

Others

By Purity Level

4N

5N

6N and Above

By End Use

Integrated Circuits

Printed Circuit Boards

Discrete Semiconductors

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising semiconductor wafer production | +3.2% | Asia Pacific, North America, Europe | Drives chemical demand. |

Growth in advanced chip manufacturing | +2.8% | Taiwan, South Korea, Japan, U.S. | Supports high-purity chemicals. |

Expansion of memory and logic devices | +2.4% | Asia Pacific, U.S., Europe | Increases process chemical use. |

Rising demand from integrated circuits | +2.0% | Global semiconductor hubs | Strengthens core consumption. |

Government support for chip production | +1.7% | U.S., Europe, China, India, Japan | Expands local capacity. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High purity and quality requirements | -1.6% | Global manufacturers | Raises production complexity. |

Raw material price volatility | -1.3% | Global chemical suppliers | Pressures margins. |

Strict environmental regulations | -1.1% | Europe, U.S., Japan, South Korea | Increases compliance cost. |

Supply chain dependence on limited suppliers | -1.0% | Asia Pacific, North America | Creates availability risk. |

High capital investment in production | -0.9% | Specialty chemical producers | Limits new entry. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of high-purity wet chemicals | +2.9% | Asia Pacific, U.S., Europe | Supports chip fabrication. |

Rising demand for photoresists and developers | +2.5% | Taiwan, South Korea, Japan, U.S. | Enables advanced lithography. |

Growth in 5N purity chemicals | +2.2% | Advanced semiconductor fabs | Builds premium demand. |

New fab investments across regions | +2.0% | U.S., Europe, India, Japan | Creates long-term demand. |

Chemical recycling and waste reduction solutions | +1.5% | Europe, North America, Asia Pacific | Improves sustainability value. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining ultra-high purity consistency | -1.5% | Global fabs | Affects yield performance. |

Managing hazardous chemical handling | -1.2% | Semiconductor production sites | Raises safety burden. |

Long qualification cycles with chipmakers | -1.1% | Global suppliers | Slows customer onboarding. |

Geopolitical pressure on chip supply chains | -1.0% | U.S., China, Taiwan, Europe | Creates sourcing risk. |

Waste treatment and disposal complexity | -0.9% | Global | Increases operating cost. |

Recent Developments

In May 2026, BASF launched a yellow-light material solution for photolithography-related semiconductor processes. It blocks wavelengths below 530 nm and can reduce energy use by 25% in cleanroom lighting systems.

In 2026, Shin-Etsu progressed its Isesaki lithography materials base, with first-phase completion planned by 2026. The site covers about 150,000 square meters , and first-phase investment is expected at about JPY 83.0 billion

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 23.9 Billion |

Forecast Revenue (2035) | USD 75.6 Billion |

CAGR (2025-2035) | 12.2% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Chemical Type (Acid and Base Chemicals, High-Performance Polymers, Adhesives, Solvents, Others), By Purity Level (4N, 5N, 6N and Above), By End Use (Integrated Circuits, Printed Circuit Boards, Discrete Semiconductors, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | BASF SE, Merck KGaA, Fujifilm Holdings Corporation, Shin-Etsu Chemical Co., Ltd., Tokyo Ohka Kogyo Co., Ltd., JSR Corporation, Entegris, Inc., DuPont de Nemours, Inc., Sumitomo Chemical Co., Ltd., and Dow Inc. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

BASF SE

Merck KGaA

Fujifilm Holdings Corporation

Shin-Etsu Chemical Co., Ltd.

Tokyo Ohka Kogyo Co., Ltd.

JSR Corporation

Entegris, Inc.

DuPont de Nemours, Inc.

DuPont de Nemours, Inc.

Dow Inc.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Ethylene Market Size to Hit USD 306.4 Billion by 2035

Global Ethylene Market Size, Share Analysis By Feedstock (Naphtha, Ethane, Propane, Butane, Others), By Derivative (Polyethylene, Ethylene Oxide, Ethylene Dichloride, Ethylbenzene, Others), By Application (Packaging, Construction, Automotive, Consumer Goods, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035