Revenue, 2025

$ 46.7 Bn

Forecast, 2035

$ 79.0 Bn

CAGR, 2025-2035

5.4%

Report Coverage

Global

Market Size and Forecast

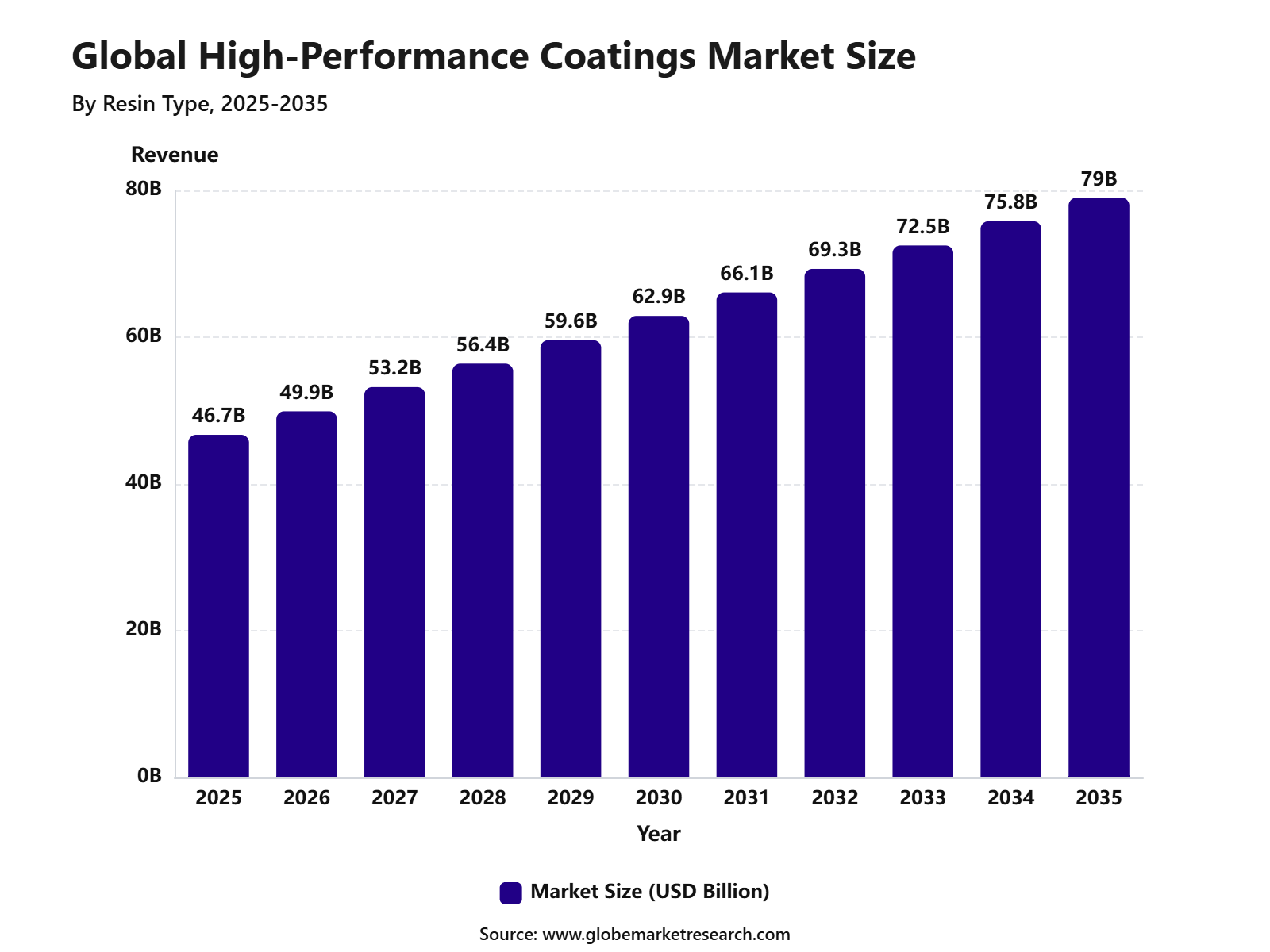

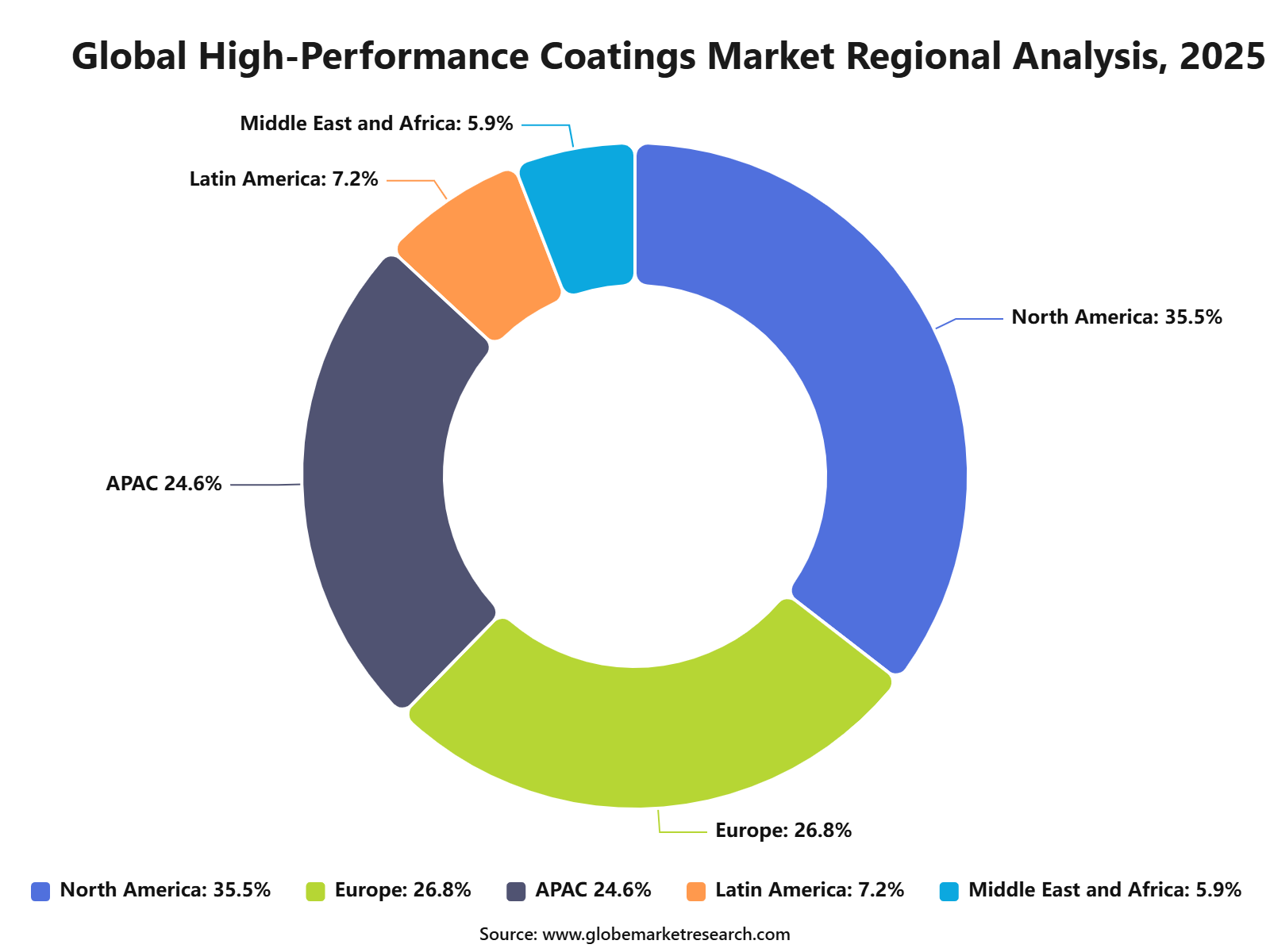

The Global High-Performance Coatings Market was worth USD 46.7 billion in 2025 and is expected to reach USD 79.0 billion by 2035, growing at a CAGR of 5.4% from 2025 to 2035. North America held the largest regional share of 35.5% in 2025, supported by strong demand from automotive, aerospace, marine, industrial equipment, oil and gas, and infrastructure protection applications.

The High-Performance Coatings Market includes advanced coating systems designed to provide corrosion resistance, chemical protection, weather durability, heat resistance, abrasion control, and long service life. These coatings are widely used on metal structures, pipelines, vehicles, aircraft, ships, bridges, machinery, floors, and industrial facilities. The market is closely linked with protective maintenance, asset life extension, industrial safety, and surface performance requirements.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains steady as industries continue to invest in durable coatings that reduce repair costs and protect assets in harsh environments. Growth can be attributed to rising infrastructure renovation, stricter corrosion protection standards, and increasing use of advanced coatings in transportation and energy sectors. The expansion of low-VOC formulations, smart coatings, and sustainable protective systems is expected to support long-term market demand.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 46.7 Billion |

Forecast Revenue (2035) | USD 79.0 Billion |

CAGR (2025-2035) | 5.4% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Epoxy led the resin type segment with 28.9% share, supported by its strong adhesion, corrosion resistance, chemical durability, and wide use in protective coating systems.

Waterborne formulations accounted for 36.8% share, driven by rising demand for low-VOC coatings, easier application, and better compliance with environmental standards.

Automotive applications held 25.8% share, supported by growing use of high-performance coatings for surface protection, durability, appearance, and resistance against weathering and abrasion.

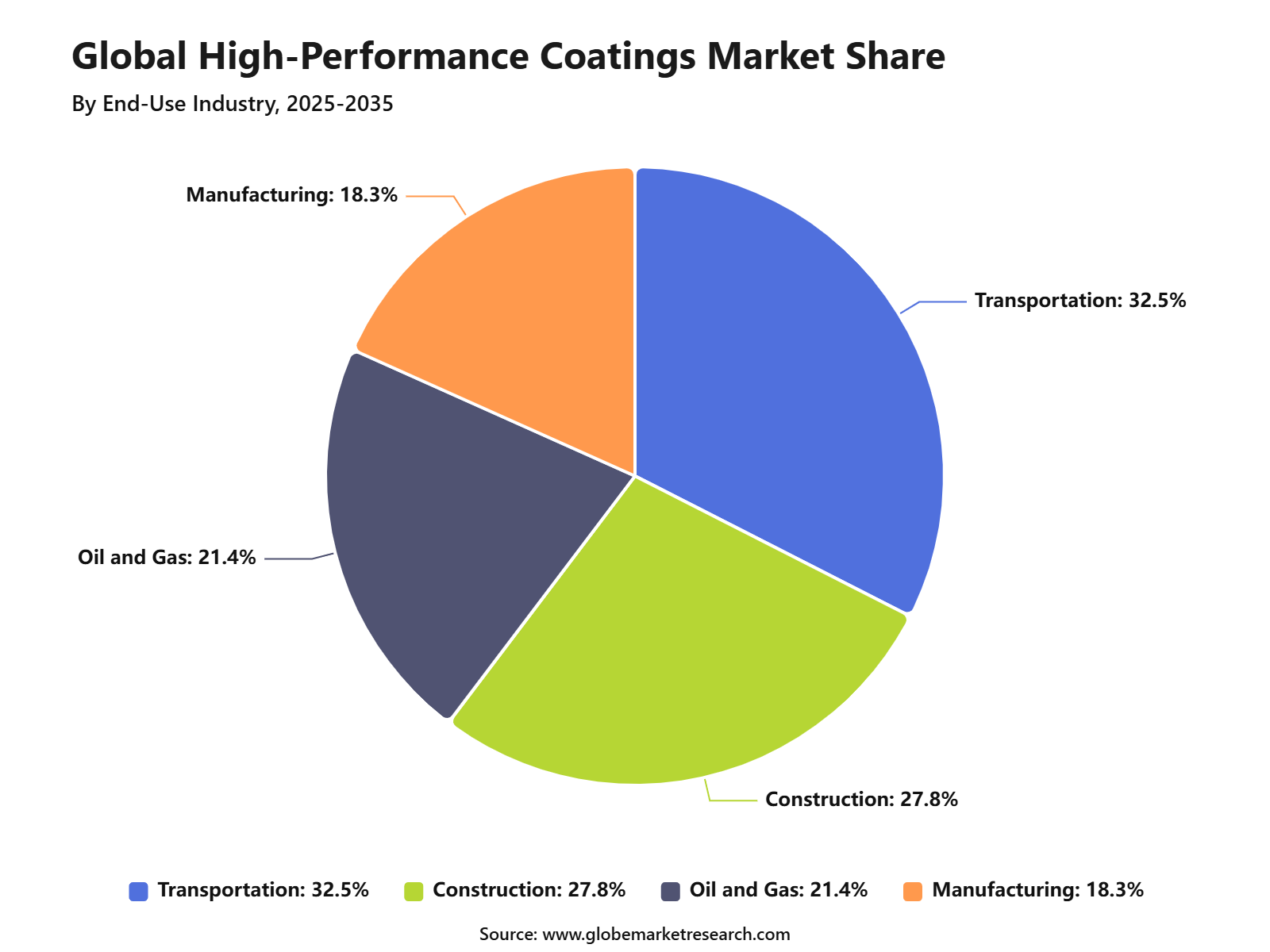

Transportation captured 32.5% share by end-use industry, driven by strong demand from automotive, aerospace, rail, marine, and commercial vehicle coating applications.

North America led the high-performance coatings market with 35.5% share, supported by advanced manufacturing, strong automotive production, strict coating performance standards, and rising demand for durable protective materials.

Top Funding and Investment Highlights

AkzoNobel and Axalta announced an all-stock merger of equals in November 2025, creating a coatings company with an enterprise value of about USD 25.0 billion. The combined company is expected to generate around USD 17.0 billion in revenue, with nearly USD 600.0 million in cost synergies. This deal strengthens high-performance coatings exposure across automotive, refinish, powder, aerospace, marine, and protective coatings.

Henkel agreed to acquire Stahl Group for EUR 2.1 billion in February 2026. Stahl is active in high-performance specialty coatings for flexible materials used in automotive, fashion, lifestyle, and packaging applications. The company generated around EUR 725.0 million in adjusted sales in 2025 and employed nearly 1,700 people, making the deal important for performance coatings used on flexible substrates.

PPG announced a USD 380.0 million investment in May 2025 to build a new aerospace coatings and sealants manufacturing facility in Shelby, North Carolina. The 198,000-square-foot plant is expected to start construction in October 2025 and be completed in the first half of 2027. It will employ more than 110 people and produce PPG’s full aerospace coatings and sealants line.

By Resin Type

Epoxy resins accounted for 28.9% share of the High-Performance Coatings Market. This leadership can be attributed to their strong adhesion, chemical resistance, corrosion protection, and high mechanical strength across demanding industrial environments. Epoxy-based coatings are widely used on metal, concrete, machinery, pipelines, marine structures, automotive parts, and industrial floors.

These coatings provide a durable protective barrier against moisture, chemicals, abrasion, and harsh operating conditions. Demand for epoxy coatings is expected to remain strong as industries focus on longer asset life and lower maintenance costs. Their ability to protect critical surfaces in transportation, construction, oil and gas, and manufacturing applications supports their continued market dominance.

By Formulation Type

Waterborne formulations held 36.8% share of the High-Performance Coatings Market. Their strong position is supported by lower solvent content, reduced emissions, improved worker safety, and increasing preference for environmentally acceptable coating systems. These coatings are used across automotive, industrial, architectural, protective, and transportation applications.

Waterborne systems offer good durability, surface finish, corrosion resistance, and ease of application while helping manufacturers meet stricter environmental requirements. The segment is gaining wider acceptance as coating producers improve resin technology, drying performance, and film strength. Demand is further supported by industries seeking coatings that combine high protection with lower environmental impact.

By Application

Automotive applications captured 25.8% share of the High-Performance Coatings Market. The segment is supported by strong demand for coatings that improve vehicle appearance, corrosion resistance, scratch protection, weather durability, and long-term surface performance. High-performance coatings are used on vehicle bodies, wheels, chassis parts, underbody components, interiors, and electric vehicle parts.

These coatings help protect vehicles from road salt, UV exposure, moisture, chemicals, heat, and mechanical wear. The automotive segment is expected to remain a key demand area as manufacturers focus on lightweight materials, premium finishes, electric mobility, and longer vehicle life. Coating performance has become important for both product quality and lifecycle cost reduction.

By End-Use Industry

The transportation industry held 32.5% share of the High-Performance Coatings Market. This dominance is driven by wide use across automotive, rail, aerospace, marine, commercial vehicles, and logistics equipment. Transportation assets are exposed to corrosion, abrasion, fuel, chemicals, changing temperatures, and outdoor weather conditions.

High-performance coatings help extend operating life, reduce repair frequency, and maintain safety, appearance, and structural protection. Growth in this segment is also supported by rising demand for electric vehicles, aircraft maintenance, commercial fleets, and marine protection. As transportation systems become more advanced, the need for durable and specialized coatings is expected to increase.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

North America accounted for 35.5% share of the High-Performance Coatings Market. The region’s leadership is supported by strong demand from automotive, aerospace, construction, industrial manufacturing, marine, and oil and gas sectors.

The market benefits from high adoption of advanced coating technologies, strict performance standards, and growing focus on asset protection. Industries in the region use high-performance coatings to reduce corrosion damage, improve operational reliability, and lower maintenance costs.

North America is expected to maintain a strong position due to continued investment in infrastructure renewal, vehicle production, aerospace maintenance, and industrial modernization. Demand for waterborne, low-emission, and long-lasting coating systems will further support regional growth.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-to-Market and Sales Economics

The go-to-market approach for the High-Performance Coatings Market should focus on technical performance, asset protection and lifecycle cost reduction. Demand is strongest in automotive, aerospace, marine, industrial equipment, construction, energy, infrastructure and electronics, where coatings must provide corrosion resistance, chemical resistance, heat stability, weather protection and longer service life. In Q1 2026, PPG reported net sales of USD 3.9 billion, up 7% year over year, with organic growth supported by higher selling prices and strength in aerospace, protective and marine coatings.

Sales economics are being shaped by specification-led buying, where customers choose coatings based on durability, compliance and application support rather than only price. Axalta’s Performance Coatings segment reported USD 802 million in Q1 2026 net sales, with growth outside North America offsetting softer regional demand. This shows that global suppliers need strong refinish networks, local distribution and technical service teams to protect revenue across uneven markets.

The strongest commercial model is direct selling to OEMs, asset owners, contractors and industrial applicators, supported by approved product lists and long-term maintenance programs. Sherwin-Williams reported Q1 2026 consolidated net sales of USD 5.67 billion, up 6.8%, while its Performance Coatings Group supplies engineered solutions for construction, industrial, packaging and transportation markets in more than 120 countries.

Risk Factors & Market Barriers

The main barriers are raw material volatility, long qualification timelines, regulatory pressure, and higher upfront pricing. High-performance coatings depend on resins, pigments, additives, solvents, curing agents, corrosion inhibitors, and specialty fillers. FRED reported the U.S. paint and coating manufacturing PPI at 442.155 in May 2026, up from 431.311 in January.

VOC and hazardous air pollutant regulations can also affect formulation choices. AMPP notes that VOC limits for industrial maintenance coatings can be 450 grams per liter, depending on category and rule. Producers must therefore manage solvent content, worker safety, emissions control, application conditions, and customer-specific regulatory documentation.

Technical barriers remain high because each end use requires a different balance of adhesion, flexibility, gloss, hardness, weathering, chemical resistance, and curing speed. Marine, aerospace, electronics, automotive, and infrastructure buyers often require multi-stage qualification. Any coating failure can lead to warranty costs, repainting, downtime, and customer loss.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities are strongest across protective coatings, marine coatings, aerospace coatings, automotive coatings, industrial coatings, powder coatings, floor coatings, coil coatings, and electronics coatings. Special-purpose coatings, including marine, industrial, construction, and maintenance coatings, reached a FRED index level of 543.969 in May 2026, reflecting a high-value coating category.

Infrastructure and construction remain strong revenue bases. U.S. construction spending reached a seasonally adjusted annual rate of USD 2,172.4 billion in April 2026. FHWA also states that the Infrastructure Investment and Jobs Act provides about USD 350.0 billion for federal highway programs over fiscal years 2022 to 2026.

Automotive, aerospace, and electronics provide higher-value demand. IEA expects global electric car sales to reach 23.0 million in 2026, representing 28% of total car sales. Airbus reported 81 aircraft deliveries in May 2026 and 262 deliveries year-to-date, supporting coatings demand for transport surfaces, interiors, components, and protective finishes.

Financial Impact

The financial impact in 2026 will depend on resin pricing, pigment cost, energy use, curing technology, batch quality, application efficiency, and customer approval timelines. Architectural coatings reached a FRED index level of 530.861 in May 2026, while special-purpose coatings remained higher, showing stronger price intensity in performance-led coating categories.

Margins can improve when suppliers target premium applications instead of commodity coatings. Bridges, offshore platforms, ships, aircraft, wind towers, EV battery systems, chemical plants, and semiconductor facilities can justify higher prices when coatings reduce corrosion, downtime, cleaning, repainting, and asset replacement. Lifecycle savings should be clearly quantified for procurement teams.

Financial returns are expected to be stronger for suppliers offering technical service, certified systems, and long-term maintenance partnerships. SEMI projects worldwide 300mm fab equipment spending to rise 18% to USD 133 billion in 2026, creating demand for clean manufacturing surfaces, process-area coatings, corrosion protection, and specialty protective materials.

Drivers Impact Analysis

The High-Performance Coatings Market is driven by rising demand for durable, corrosion-resistant, weather-resistant, and chemical-resistant surface protection across automotive, aerospace, marine, construction, energy, and industrial equipment applications. These coatings help extend asset life, reduce maintenance cost, and protect materials in harsh operating environments.

North America leads the market due to strong industrial activity, infrastructure maintenance, aerospace manufacturing, oil and gas operations, and demand for advanced protective coatings. The U.S. remains a major contributor because of large-scale use in transportation, industrial facilities, commercial buildings, and energy infrastructure.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for corrosion protection | +1.4% | North America, Europe, Asia Pacific | Drives core usage. |

Growth in industrial maintenance coatings | +1.2% | U.S., Canada, Germany, China | Supports recurring demand. |

Expansion of aerospace and automotive uses | +1.0% | North America, Europe, Japan | Builds premium demand. |

Infrastructure repair and refurbishment | +0.9% | U.S., Europe, Asia Pacific | Supports coating consumption. |

Demand for longer asset life | +0.7% | Marine, energy, manufacturing sectors | Reduces maintenance cost. |

Restraints Impact Analysis

The market faces restraints from volatile raw material prices, strict VOC regulations, and the higher cost of advanced coating systems. High-performance coatings often require specialty resins, additives, pigments, curing agents, and surface preparation, which increases total application cost.

Environmental rules are also shaping product development. Manufacturers must reduce solvent emissions, improve worker safety, and meet performance requirements at the same time, which can increase formulation complexity and slow adoption among cost-sensitive users.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Raw material price volatility | -0.8% | Global producers | Pressures margins. |

Strict VOC and emission standards | -0.7% | North America, Europe, Japan | Raises compliance burden. |

High application and surface preparation cost | -0.6% | Industrial and infrastructure users | Limits wider use. |

Competition from standard coatings | -0.5% | Price-sensitive markets | Slows premium adoption. |

Skilled applicator requirement | -0.4% | Construction, marine, industrial sites | Affects project quality. |

Opportunities Impact Analysis

Opportunities are growing in infrastructure protection, energy assets, marine coatings, aerospace coatings, electric vehicles, and advanced industrial equipment. These applications need coatings that can withstand corrosion, abrasion, chemicals, UV exposure, heat, and moisture.

Higher-value opportunities are also emerging in waterborne, powder, and low-VOC high-performance coating systems. Companies that can combine strong durability with regulatory compliance and easier application can capture stronger demand from industrial and commercial customers.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Low-VOC coating innovation | +1.3% | North America, Europe, developed Asia | Supports cleaner adoption. |

Infrastructure protection projects | +1.1% | U.S., Canada, Europe, Asia Pacific | Builds long-term demand. |

Marine and offshore coating demand | +0.9% | North America, Europe, Asia Pacific | Expands corrosion control. |

Energy and utility asset protection | +0.8% | U.S., Middle East, Asia Pacific | Supports industrial use. |

Powder coating and waterborne systems | +0.7% | Global manufacturing markets | Improves sustainability value. |

Challenges Impact Analysis

The main challenge is balancing durability, cost, application ease, and environmental compliance. End users want coatings that perform in demanding conditions, but they also expect faster curing, lower emissions, and reduced lifecycle cost. Another challenge is maintaining coating performance across different substrates and environments. Steel, aluminum, concrete, composites, and plastics require different surface preparation and coating systems, which increases technical complexity for suppliers and applicators.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing performance and compliance | -0.7% | North America, Europe, Asia Pacific | Raises formulation difficulty. |

Surface preparation complexity | -0.6% | Industrial and infrastructure sites | Affects coating life. |

Maintaining adhesion across substrates | -0.5% | Automotive, aerospace, construction | Impacts reliability. |

Reducing curing time without quality loss | -0.5% | Manufacturing and repair facilities | Affects productivity. |

Proving long-term field performance | -0.4% | Marine, energy, infrastructure | Slows qualification. |

Segment Covered in the Report

By Resin Type

Epoxy

Polyurethane

Acrylic

Polyester

Silicone

By Formulation Type

Waterborne

Solvent-borne

Powder Coatings

UV-cured

By Application

Aerospace

Automotive

Industrial

Marine

Electronics

By End-Use Industry

Construction

Oil and Gas

Transportation

Manufacturing

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward epoxy, polyurethane, fluoropolymer, ceramic, and powder-based high-performance coatings. These coating types are preferred where durability, corrosion resistance, chemical resistance, and appearance retention are important.

Industrial and infrastructure applications remain major demand areas, while aerospace, automotive, and energy sectors support premium-grade coatings. North America continues to lead value demand because of advanced industrial standards, infrastructure maintenance, and strong protective coating usage.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Epoxy coatings remain widely used | +1.3% | Industrial, marine, infrastructure sectors | Leads protection demand. |

Polyurethane coatings gain preference | +1.1% | Automotive, aerospace, construction | Supports durability. |

Powder coatings expand adoption | +0.9% | Manufacturing and metal finishing | Reduces emissions. |

Waterborne technologies gain traction | +0.8% | North America, Europe, Asia Pacific | Supports VOC compliance. |

Anti-corrosion coatings remain key trend | +0.7% | Energy, marine, infrastructure | Adds lifecycle value. |

Investor Type Impact Matrix

Investors should focus on coating companies with strong formulation capability, regulatory expertise, industrial distribution, and exposure to infrastructure, aerospace, marine, and energy sectors. These customer groups require high reliability, which supports long-term supply relationships. Strategic investors can also target waterborne technologies, powder coatings, anti-corrosion systems, and smart protective coatings. Companies that combine strong performance with easier application and lower emissions are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High-Performance Coating Manufacturers | +1.2% | Global | Expands product capacity. |

Industrial Coating Suppliers | +1.0% | North America, Europe, Asia Pacific | Drives maintenance demand. |

Aerospace and Automotive Coating Companies | +0.9% | U.S., Canada, Europe, Japan | Supports premium use. |

Marine and Energy Coating Providers | +0.8% | Offshore and industrial regions | Builds corrosion protection. |

Private Equity and Strategic Investors | +0.6% | Specialty coating markets | Supports portfolio growth. |

Recent Developments

In April 2026, Axalta received three Edison Awards for coating innovations in vehicle customization, EV battery safety, and AI-powered tint manufacturing. Its Alesta e-PRO FG Black coating is designed for EV battery systems and can resist extreme thermal conditions up to 1200°C, while TintMaster AI improved right-first-time performance by up to 29% in selected manufacturing cases.

Sherwin-Williams also reported strong 2026 activity in performance coatings. Its Performance Coatings Group generated USD 1.71 billion in Q1 2026 sales, compared with USD 1.60 billion in Q1 2025. The group supplies engineered coatings for construction, industrial, packaging, and transportation markets in more than 120 countries.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

AkzoNobel

BASF SE

PPG Industries

Sherwin-Williams

Hempel

Nippon Paint

RPM International

Kansai Paint

Jotun

Axalta Coating Systems

Eastman Chemical Company

Covestro AG

DuPont

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035