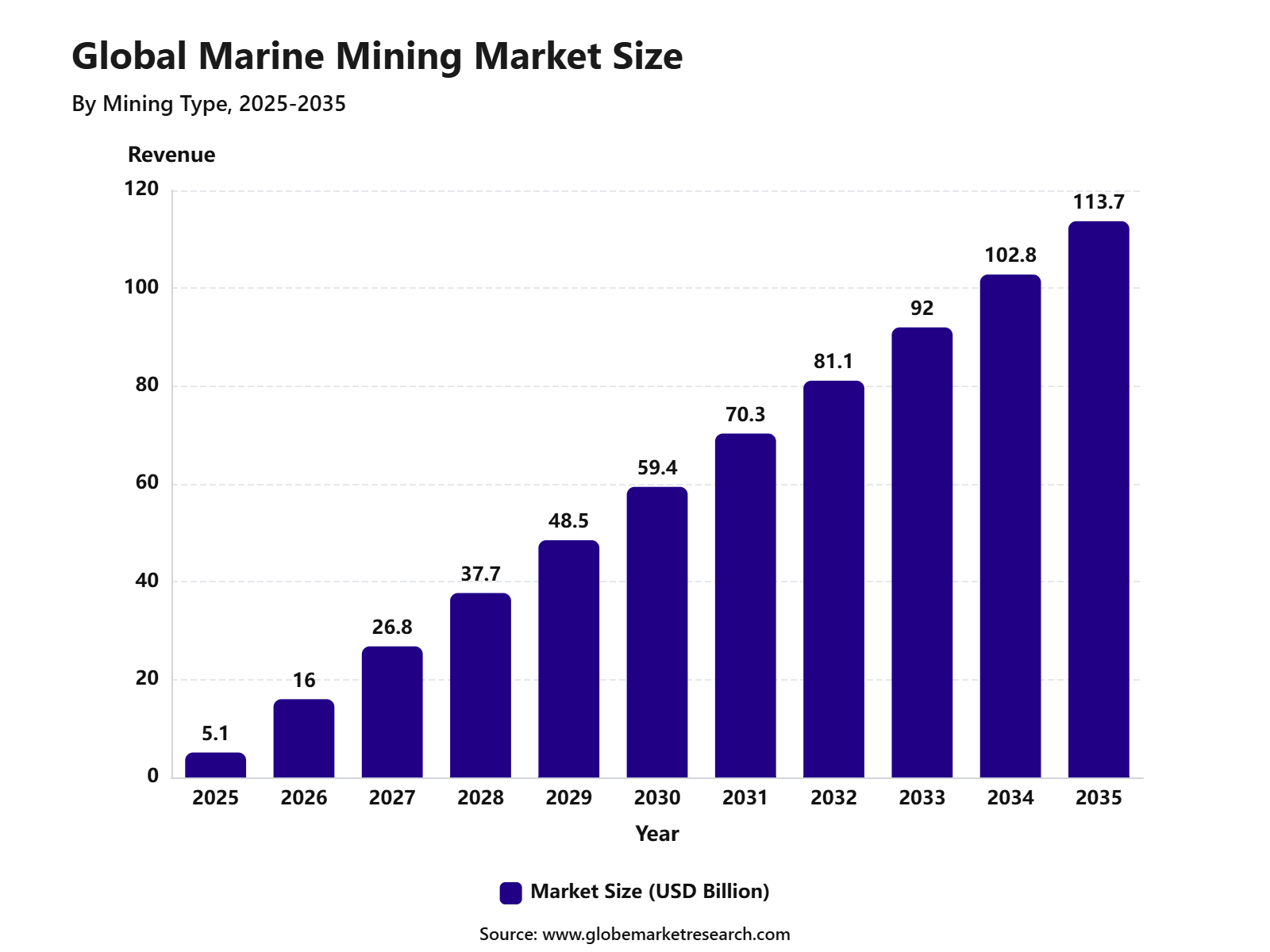

Revenue, 2025

$ 5.1 Bn

Forecast, 2035

$ 113.7 Bn

CAGR, 2025-2035

36.4%

Report Coverage

Global

Market Size and Forecast

The Global Marine Mining Market reached USD 5.1 billion in 2025 and is expected to grow to USD 113.7 billion by 2035, registering a CAGR of 36.4% from 2025 to 2035. The growth of the market can be attributed to rising demand for critical minerals, increasing exploration of seabed resources, and growing interest in deep-sea deposits containing nickel, cobalt, copper, manganese, and rare earth elements.

The Marine Mining Market refers to the extraction of minerals and metals from seabeds, continental shelves, and deep-ocean deposits. These resources are used across batteries, renewable energy systems, electric vehicles, electronics, aerospace, defense, and industrial manufacturing. The market is closely linked with offshore exploration technology, remotely operated vehicles, seabed mapping systems, marine robotics, and environmental monitoring solutions.

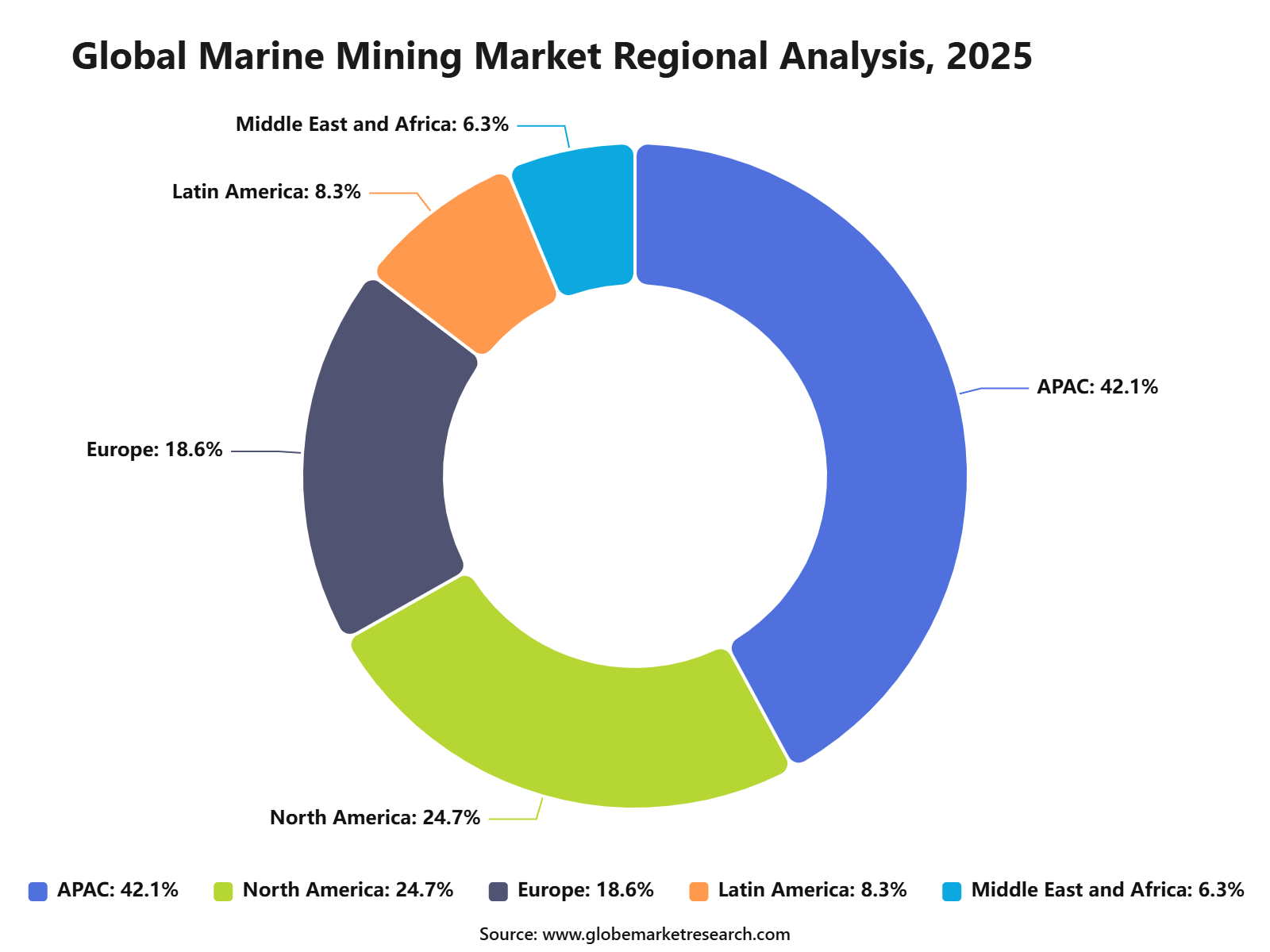

Asia Pacific held the largest regional share of 42.1% in 2025, supported by strong demand for battery minerals, expanding electric vehicle production, and rising investment in offshore resource exploration across China, Japan, South Korea, India, and Southeast Asia. The region’s growth is further driven by industrial mineral needs, maritime technology development, and government interest in securing long-term critical mineral supply chains.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

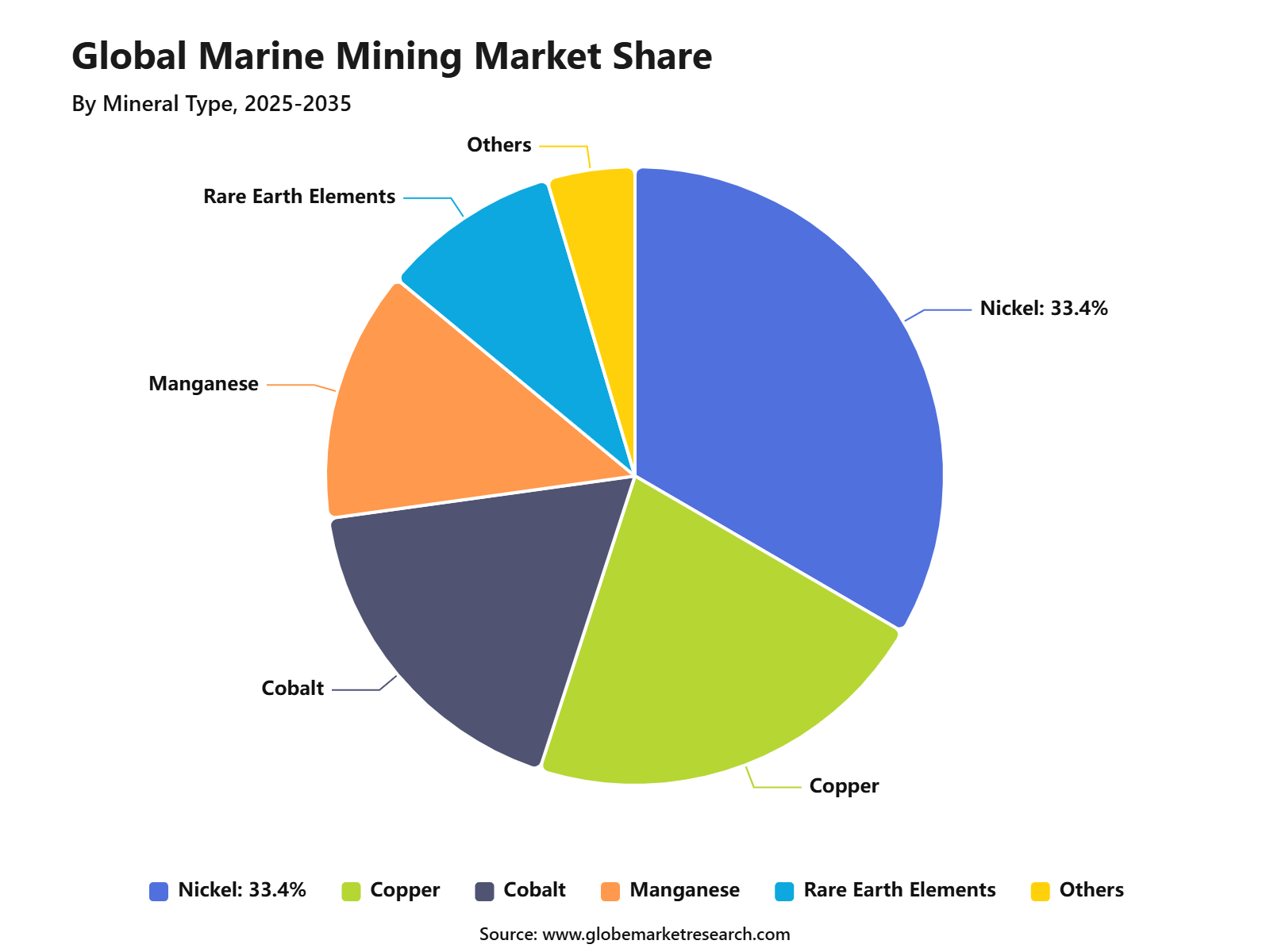

Polymetallic nodules led the mining type segment with 46.6% share, supported by their strong concentration of critical minerals used in batteries, electronics, and clean energy technologies.

Nickel accounted for 33.4% share by mineral type, driven by rising demand from electric vehicle batteries, stainless steel production, and energy storage applications.

Remotely operated vehicles held 45.5% share by technology, supported by their use in deep-sea exploration, seabed mapping, mineral collection, and safer underwater operations.

Asia Pacific led the marine mining market with 42.1% share, supported by strong demand for critical minerals, active offshore resource exploration, and rising investment in advanced marine technologies.

Government Initiatives for the Marine Mining Market

Government initiatives for the Marine Mining Market are mainly focused on seabed mineral regulation, critical mineral security, environmental protection, scientific mapping, permitting systems, and international governance. Unlike conventional mining, marine mining remains highly policy-sensitive because commercial deep-sea mining has not yet been approved under the International Seabed Authority framework. The ISA states that only exploration contracts have been issued so far, while commercial exploitation rules are still under development.

Seabed Mining Code and Commercial Regulation

The most important initiative for the marine mining market is the development of the international Mining Code. The International Seabed Authority has been working on exploitation regulations since 2014 to govern commercial mining in international seabed areas. These regulations are intended to balance mineral development with strict environmental protection, liability rules, inspection systems, and benefit-sharing obligations.

This regulatory process is directly shaping market readiness. In March 2026, the ISA Council completed part of its 31st session after nine days of negotiations on draft exploitation regulations. The continued negotiation process shows that governments are still working to create a legal structure before full commercial extraction can begin.

Exploration Contracts and Resource Assessment

Government-backed exploration licensing is supporting early-stage marine mining activity. The ISA has issued 31 exploration contracts to 21 contractors sponsored by 20 countries. These include 19 contracts for polymetallic nodules, 8 for polymetallic sulphides, and 4 for cobalt-rich ferromanganese crusts.

These contracts help companies and public agencies assess seabed mineral potential before commercial mining decisions are made. Key resources include manganese, nickel, copper, cobalt, and rare earth elements, which are used in renewable energy systems, batteries, electronics, defense equipment, and advanced manufacturing. This makes marine mining relevant to critical mineral supply security, although environmental and legal barriers remain significant.

Mining Type Analysis

Polymetallic nodules led the Marine Mining Market with 46.6% share, supported by their rich concentration of critical minerals such as nickel, cobalt, copper, and manganese. These nodules are found on deep ocean floors and are gaining attention because they can support demand from batteries, clean energy technologies, electronics, and advanced manufacturing.

The growth of this segment can be attributed to rising interest in alternative mineral sources as land-based supply chains face pressure from resource concentration, permitting delays, and geopolitical risks. Polymetallic nodules are attractive because they contain multiple metals in one deposit type, which improves their strategic importance for future mineral supply.

The segment is expected to remain a major focus area during the exploration phase of marine mining. However, commercial development will depend on clear international regulations, environmental safeguards, seafloor ecosystem studies, processing economics, and responsible mineral sourcing standards.

Mineral Type Analysis

Nickel accounted for 33.4% share, making it the leading mineral type in the Marine Mining Market. Nickel is a key metal used in stainless steel, batteries, alloys, plating, energy storage systems, and advanced industrial applications, which supports its strong demand outlook.

The growth of this segment is being driven by the increasing need for battery-grade and industrial nickel. Demand from electric vehicles, renewable energy storage, and high-performance alloys is creating interest in seabed resources that may support long-term supply diversification.

Nickel is expected to remain a high-value target in marine mining because of its role in energy transition technologies and industrial manufacturing. Future demand will depend on battery chemistry trends, land-based nickel supply growth, processing capacity, environmental regulation, and market acceptance of seabed-sourced minerals.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFTechnology Analysis

Remotely operated vehicles led the technology segment with 45.5% share, supported by their use in deep-sea exploration, seabed mapping, visual inspection, sampling, monitoring, and equipment support. ROVs allow operators to work in deep ocean environments without sending people underwater, which improves safety and operational control.

The growth of this segment can be attributed to the need for accurate underwater data before any marine mining activity can move forward. ROVs can collect images, video, samples, and environmental data from difficult seabed conditions, helping companies and regulators assess mineral potential and ecological risk.

ROVs are expected to remain central to marine mining exploration because deep-sea operations require precision, remote control, and real-time observation. Demand is likely to remain strong for high-depth ROVs, sensor-equipped systems, robotic sampling tools, seabed mapping platforms, and environmental monitoring technologies.

Regional Analysis

Asia Pacific led the Marine Mining Market with 42.1% share, supported by strong demand for critical minerals, active seabed exploration interest, and large downstream industries in batteries, electronics, shipbuilding, and clean energy technologies. China, India, Japan, South Korea, and Pacific island-linked exploration zones are important to the region’s long-term position.

The growth of Asia Pacific can be linked to rising mineral security priorities and strong industrial demand for nickel, cobalt, copper, manganese, and rare earth elements. The region also benefits from advanced marine engineering capability, ocean research programs, and strong manufacturing sectors that require stable mineral inputs.

Asia Pacific is expected to remain a leading region as governments and companies evaluate seabed mineral potential. Future opportunities are likely to be seen in polymetallic nodule exploration, nickel recovery, ROV-based surveying, environmental monitoring, offshore mineral processing research, and responsible supply chain development.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +10.8% | Asia Pacific, 42.1% share in 2025 | Leads project demand. |

China battery material demand | +8.4% | China | Drives mineral interest. |

Japan and South Korea supply security focus | +6.9% | Japan, South Korea | Supports strategic sourcing. |

Europe critical mineral diversification | +5.8% | Germany, UK, France, Nordic countries | Builds investment interest. |

North America strategic mineral demand | +5.1% | U.S. and Canada | Supports future projects. |

Go-To-Market-Strategy

The Marine Mining Market should be positioned through a regulated exploration, environmental baseline, and critical-mineral security strategy in 2026. Commercial seabed mining is still not approved in international waters, so near-term entry should focus on exploration services, survey vessels, seabed mapping, ROV systems, AUV systems, sampling equipment, and environmental monitoring support.

The customer base should include government agencies, seabed mineral contractors, marine technology firms, offshore engineering companies, battery-material buyers, and strategic mineral programs. NOAA identifies deep seabed resources as containing manganese, nickel, cobalt, copper, and rare earth elements, which are used in defense systems, batteries, smartphones, and medical devices.

The go-to-market approach should be partnership-led because projects require permits, technical proof, ocean science data, and long approval timelines. ISA has entered 15-year exploration contracts with 21 contractors, while polymetallic nodule contractors receive exploration areas of 75,000 square kilometres each. This creates demand for compliance-ready marine services.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities are currently stronger in exploration, marine robotics, bathymetric mapping, environmental assessment, sampling, vessel leasing, data analytics, and project consulting than in mineral production. ISA lists 19 exploration contracts for polymetallic nodules, seven for polymetallic sulphides, and five for cobalt-rich crusts, creating a service-based revenue base before commercial mining begins.

Across mineral types, polymetallic nodules attract strong attention because they contain nickel, cobalt, copper, and manganese. Polymetallic sulphides and cobalt-rich ferromanganese crusts also support interest in copper, cobalt, rare earth elements, and other strategic minerals. Revenue can therefore be built around exploration packages, test mining support, metallurgical studies, and compliance documentation.

Regional activity is expected to concentrate around the Clarion-Clipperton Zone, Indian Ocean, Mid-Atlantic Ridge, and Pacific Ocean exploration areas. NOAA also listed multiple 2026 U.S. exploration license applications, including public comment periods and hearings. These activities indicate that North America-linked permitting, Pacific seabed access, and contractor-led exploration can support near-term revenue.

Financial Impact

The financial impact of the Marine Mining Market in 2026 is shaped by high upfront spending and delayed production revenue. Companies must fund vessels, robotics, sensors, data systems, sampling campaigns, feasibility studies, environmental work, and regulatory filings before commercial extraction is approved. This makes cash flow dependent on contracts, government support, and strategic partners.

Revenue quality can improve where suppliers provide recurring services rather than waiting for mineral sales. Environmental monitoring, traceability systems, equipment maintenance, digital seabed data, laboratory testing, and compliance reporting can create repeat income. The 2026 IEA-OECD traceability report surveyed more than 80 companies across copper, lithium, nickel, cobalt, graphite, and rare earth supply chains.

Long-term financial upside is linked with critical-mineral demand, but recycling and substitution may reduce the need for new extraction. IEA states that scaling recycling could reduce new mining supply growth by 25% to 40% by mid-century. Marine mining players therefore need strong cost discipline, environmental credibility, and flexible business models.

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Polymetallic nodules lead mining focus | +8.7% | Pacific and Indian Ocean regions | Drives resource interest. |

Nickel remains key mineral target | +7.4% | Asia Pacific, Europe, North America | Supports battery demand. |

ROV-based operations gain importance | +6.6% | Deep-sea mining projects | Improves extraction safety. |

Strategic minerals linked to energy transition | +6.0% | Global | Expands investment case. |

Stronger ESG review of seabed projects | +4.8% | Europe, North America, Pacific Islands | Shapes project approvals |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Marine Mining Companies | +8.5% | Global offshore zones | Expands exploration activity. |

Battery Material Producers | +7.3% | Asia Pacific, Europe, North America | Drives mineral offtake. |

Offshore Technology Providers | +6.4% | Deep-sea project markets | Supports equipment demand. |

Strategic Government Investors | +5.6% | U.S., Japan, South Korea, Europe | Secures mineral supply. |

Infrastructure and Private Equity Investors | +4.8% | Processing and logistics hubs | Funds commercial scaling. |

Segment Covered in the Report

By Mining Type

Polymetallic Nodules

Seafloor Massive Sulfides

Cobalt-Rich Crusts

Others

By Mineral Type

Nickel

Copper

Cobalt

Manganese

Rare Earth Elements

Others

By Technology

Remotely Operated Vehicles

Autonomous Underwater Vehicles

Seabed Mining Systems

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for critical minerals | +9.4% | Asia Pacific, North America, Europe | Drives resource exploration. |

Growth in nickel and cobalt demand | +8.1% | China, Japan, South Korea, Europe | Supports battery supply. |

Expansion of offshore mineral exploration | +7.2% | Asia Pacific, Pacific Islands, Indian Ocean | Builds project pipeline. |

Increasing demand from clean energy technologies | +6.4% | Global energy transition markets | Strengthens mineral need. |

Technological progress in deep-sea equipment | +5.6% | Asia Pacific, Europe, North America | Improves extraction feasibility. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Environmental concerns over seabed disturbance | -5.8% | Global marine ecosystems | Slows project approvals. |

Unclear international regulations | -5.1% | International seabed areas | Creates investment uncertainty. |

High exploration and extraction cost | -4.6% | Deep-sea mining zones | Limits commercial rollout. |

Public opposition and ESG pressure | -4.0% | Europe, North America, Pacific regions | Affects project acceptance. |

Technical risk in deep-water operations | -3.5% | Offshore and remote regions | Raises execution risk. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Polymetallic nodule development | +8.9% | Pacific Ocean, Indian Ocean | Leads resource potential. |

Nickel-rich seabed deposits | +7.6% | Asia Pacific and deep-sea zones | Supports battery materials. |

Remotely operated vehicle deployment | +6.8% | Global marine mining projects | Improves operational control. |

Strategic mineral supply diversification | +6.1% | U.S., Europe, Japan, South Korea | Reduces land-based reliance. |

Partnerships with marine technology firms | +5.3% | Asia Pacific, Europe, North America | Accelerates project readiness. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Protecting deep-sea biodiversity | -5.5% | Global seabed ecosystems | Raises approval barriers. |

Commercializing extraction at scale | -4.9% | Deep-water project sites | Creates cost risk. |

Building processing and logistics chains | -4.2% | Asia Pacific, North America, Europe | Limits supply efficiency. |

Monitoring environmental impact | -3.8% | International waters | Requires strict oversight. |

Securing long-term regulatory clarity | -3.4% | Global marine mining zones | Delays investment decisions. |

Recent Developments

June 2026: Glomar Minerals and Cobalt Blue advanced site selection for Project Infinity, a proposed U.S. polymetallic nodule processing facility. The project is designed to refine about 200,000 tons of nodules and produce around 7,500 tons of cobalt hydroxide per year.

June 2026: NORI and TOML, subsidiaries of The Metals Company, filed claims before the International Tribunal for the Law of the Sea against the International Seabed Authority. The dispute followed compliance-related concerns under ISA exploration contracts, showing that legal risk remains a major barrier for deep-sea mining projects.

May 2026: The Metals Company and Allseas signed a commercial production agreement for the first polymetallic nodule collection system. The system is planned for 3.0 million wet tonnes per year, with commissioning targeted for Q4 2027, subject to permits, financing, and regulatory approvals. Deal value was not disclosed.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 5.1 Billion |

Forecast Revenue (2035) | USD 113.7 Billion |

CAGR (2025-2035) | 36.4% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Mining Type (Polymetallic Nodules, Seafloor Massive Sulfides, Cobalt-Rich Crusts, Others), By Mineral Type (Nickel, Copper, Cobalt, Manganese, Rare Earth Elements, Others), By Technology (Remotely Operated Vehicles, Autonomous Underwater Vehicles, Seabed Mining Systems, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | The Metals Company, BHP, Rio Tinto, Vale, Nautilus Minerals, Ocean Infinity, Seabed Resources, Global Sea Mineral Resources, DeepGreen Metals, UK Seabed Resources |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

The Metals Company

BHP

Rio Tinto

Vale

Nautilus Minerals

Ocean Infinity

Seabed Resources

Global Sea Mineral Resources

DeepGreen Metals

UK Seabed Resources

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Fuel Cells Market to Hit USD 70.2 Billion by 2035

Hydrogen Fuel Cells Market Size, Share, Analysis By Type (Air-Cooled Type, Water-Cooled Type), By Application (Stationary, Transport, Portable), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035