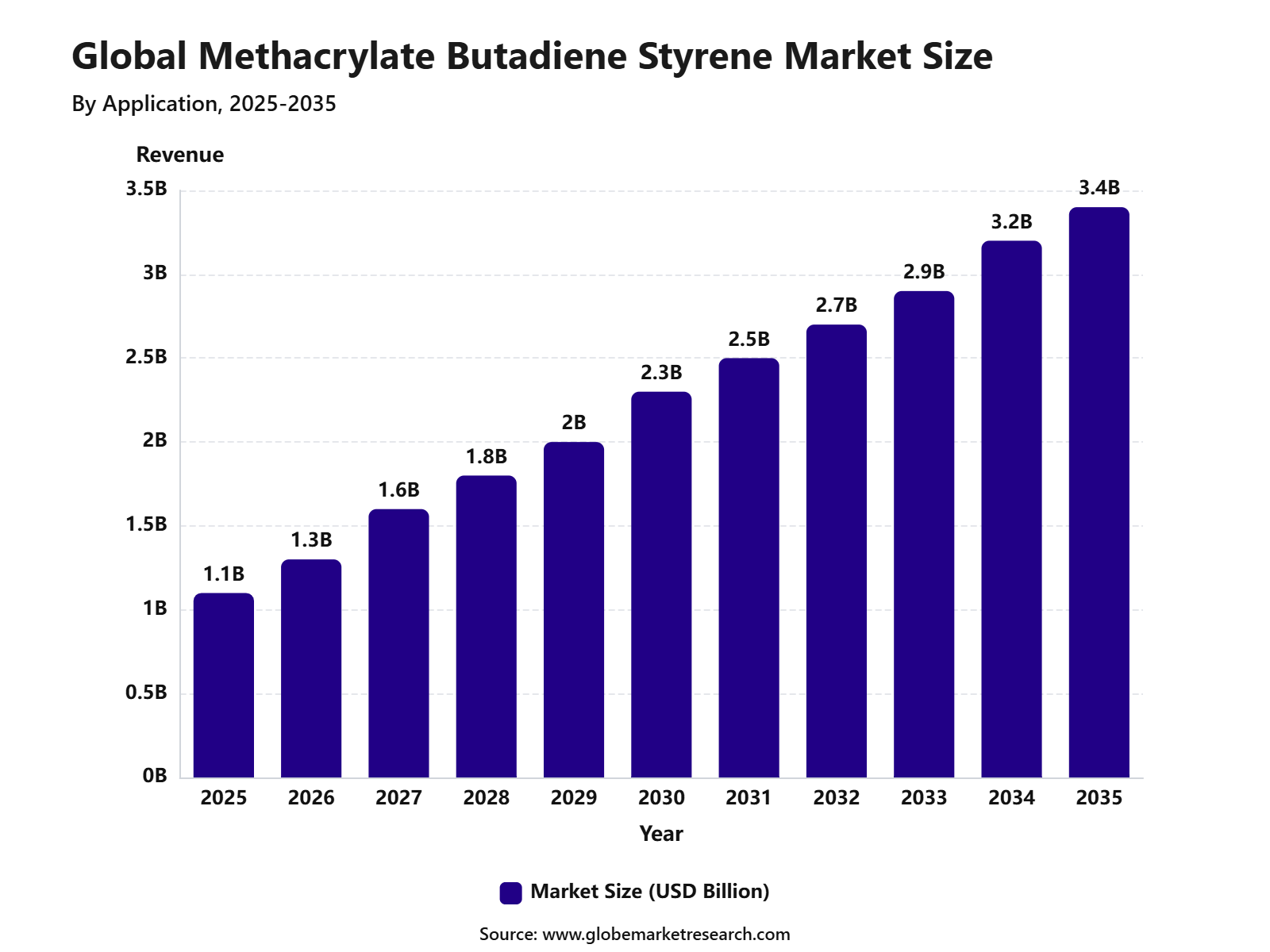

Revenue, 2025

$ 1.1 Bn

Forecast, 2035

$ 3.4 Bn

CAGR, 2025-2035

4.3%

Report Coverage

Global

Market Size and Forecast

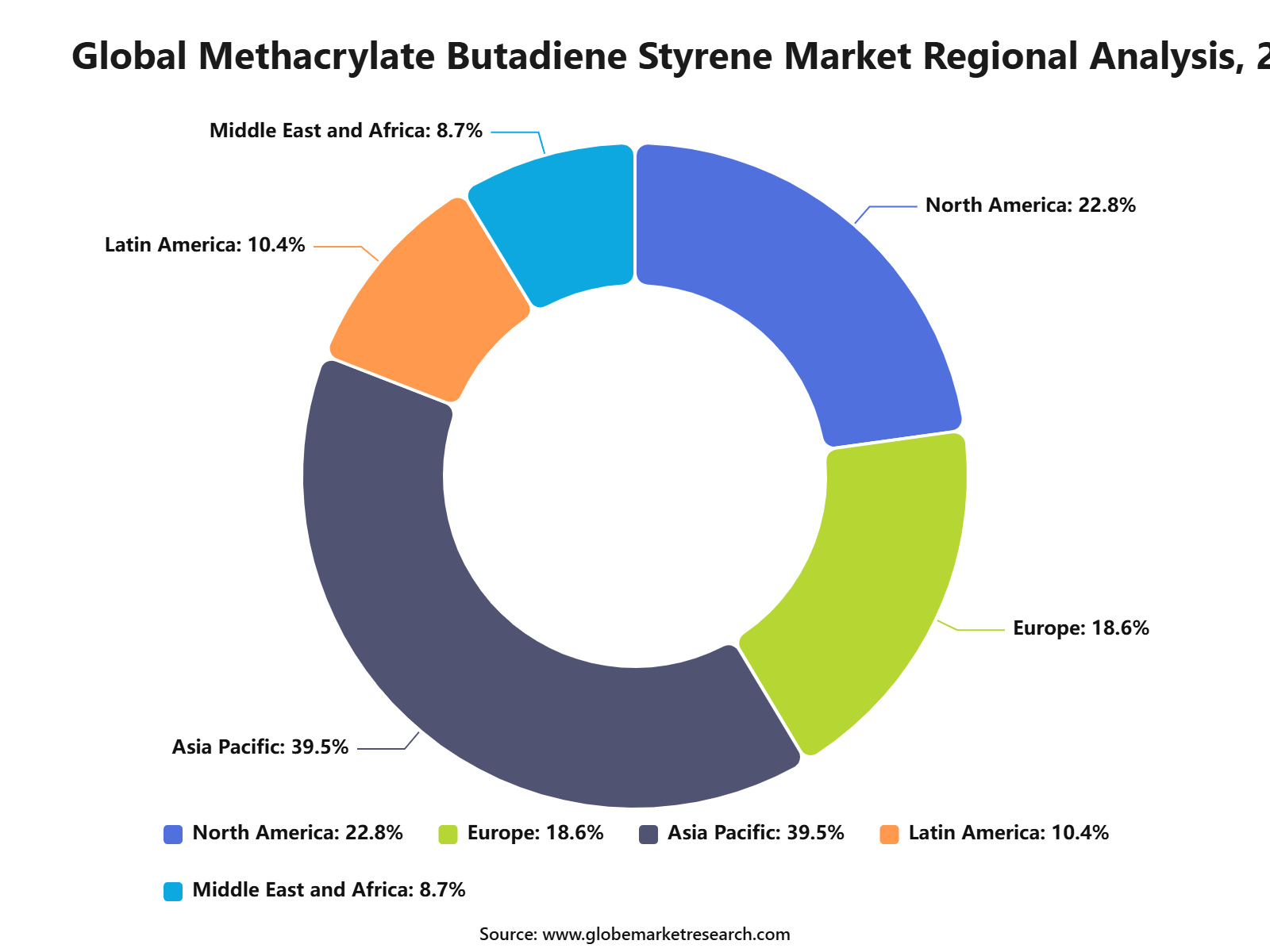

The Global Methacrylate Butadiene Styrene Market was worth USD 1.1 billion in 2025 and is expected to reach USD 3.4 billion by 2035, growing at a CAGR of 4.3% from 2025 to 2035. Asia Pacific held the largest regional share of 39.5% in 2025, supported by strong plastics manufacturing, rising demand from packaging and construction materials, and wider use of impact modifiers across China, India, Japan, South Korea, and Southeast Asia.

The Methacrylate Butadiene Styrene Market includes impact modifier materials used to improve toughness, impact strength, weather resistance, and processing performance in plastic products. MBS is widely used in PVC sheets, pipes, profiles, films, packaging materials, construction products, consumer goods, and specialty plastic applications. The market is closely linked with polymer processing, PVC modification, extrusion, injection molding, and demand for durable plastic materials.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains steady as industries continue to use MBS to improve the strength and performance of plastic products. Growth can be attributed to rising demand for impact-resistant packaging, construction plastics, consumer products, and flexible polymer applications. The expansion of PVC processing, infrastructure development, and demand for lightweight materials is expected to support long-term market growth.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 1.1 Billion |

Forecast Revenue (2035) | USD 3.4 Billion |

CAGR (2025-2035) | 4.3% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Automotive parts held the leading application share with 47.3%, supported by the use of MBS in impact-resistant, lightweight, and durable plastic components for vehicle interiors, trims, and functional parts.

Extrusion grade accounted for 59.6% share, driven by its strong processing suitability for plastic sheets, films, profiles, and components that require flexibility, clarity, and toughness.

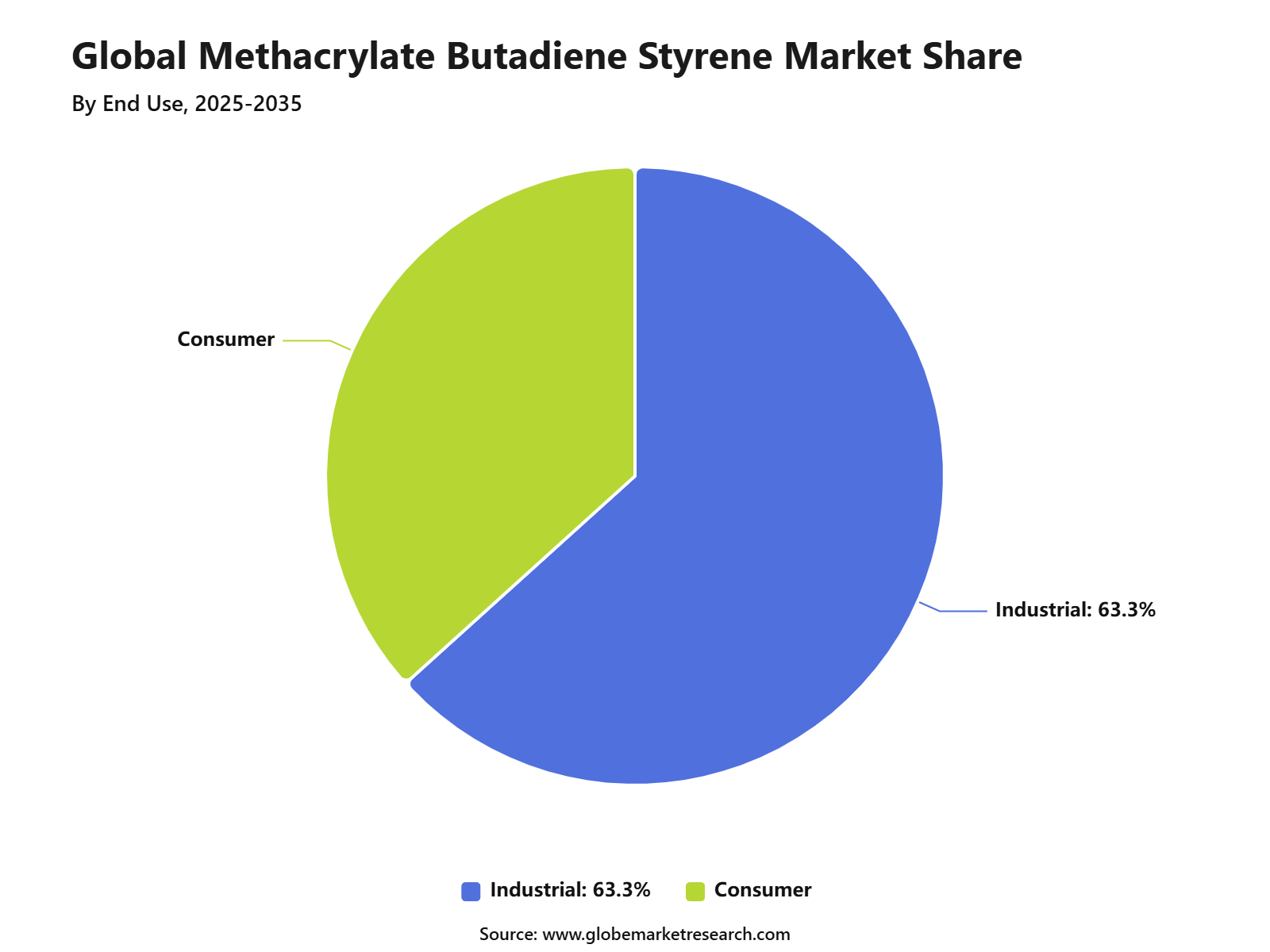

Industrial end use captured 63.3% share, supported by rising demand for high-performance polymer materials across manufacturing, fabrication, packaging, and specialty plastic applications.

Asia Pacific led the Methacrylate Butadiene Styrene market with 39.5% share, supported by strong plastics manufacturing, expanding automotive production, and growing industrial polymer consumption across major Asian economies.

Top 5 Funding and Investment Highlights

Arkema announced the proposed divestment of its impact modifiers and processing aids businesses, covering the global scope for Methyl Methacrylate Butadiene Styrene copolymers and the European and Asian scope for acrylic copolymers. The activities generated €44.0 million in sales in 2024, making this one of the clearest direct MBS-linked corporate transactions in recent disclosures.

Röhm opened its Bay City methyl methacrylate plant in Texas in 2026, with annual production capacity of 250,000 tons of MMA. The project has been reported as a USD 1.6 billion investment and is important for the MBS value chain because MMA is one of the main raw materials used in MBS copolymer production. Röhm also stated that its LiMA technology can reduce energy and water use and lower CO₂ emissions by up to 42% compared with conventional MMA production.

LG Chem announced an investment of around 60.0 billion won to build an ABS compound plant in the United States with annual capacity of 30,000 tons. Although this is an ABS compound project, it is relevant to MBS demand because MBS is used in hard and semi-hard PVC and engineering plastics to improve impact strength and processability. The project supports localized supply of high-performance plastic materials for automotive, appliance, and electronics customers.

Zhangzhou CHIMEI Chemical secured a RMB 1.8 billion syndicated loan from 15 banks to support the second phase of its ABS and PS projects. The site is planned with 600,000 tons per year of ABS, 350,000 tons per year of PS, and 180,000 tons per year of PC capacity. This investment is relevant to the wider MBS market because MBS is positioned within the same styrenic and engineering plastics ecosystem, where impact strength, transparency, and processability are key purchasing factors.

Styrenix Performance Materials acquired INEOS Styrolution Thailand, adding 85 KTPA ABS, 100 KTPA SAN, and 31 KTPA high rubber graft rubber capacity. The transaction value was reported at USD 22.3 million, with an additional USD 1.0 million for technology and licensing. This deal strengthens Southeast Asian styrenic resin supply and supports the broader value chain where MBS competes as a specialty modifier for clear PVC, engineering plastics, and impact-resistant applications.

By Application

Automotive parts held 47.3% share in the Methacrylate Butadiene Styrene market, making it the leading application segment. The dominance of this segment can be linked to the strong use of MBS in impact-modified plastic components, where toughness, durability, and dimensional stability are required.

The use of MBS in automotive parts is supported by rising demand for lightweight materials in vehicle manufacturing. Automakers are increasingly replacing heavier materials with advanced plastics to improve fuel efficiency, reduce emissions, and support electric vehicle design requirements.

Demand from this segment is also driven by interior and exterior vehicle components that require resistance to cracking, weathering, and repeated mechanical stress. As vehicle production expands across Asia Pacific and other manufacturing hubs, automotive parts are expected to remain a key revenue contributor for the MBS market.

By Grade

Extrusion grade accounted for 59.6% share in the Methacrylate Butadiene Styrene market, supported by its wide suitability in continuous plastic processing applications. This grade is preferred where smooth processing, uniform thickness, and consistent product strength are needed.

The growth of extrusion grade MBS can be attributed to its strong role in producing sheets, profiles, films, and plastic components used across industrial and consumer applications. Its ability to improve impact resistance without reducing surface quality makes it valuable for manufacturers.

Extrusion grade is also gaining importance as producers focus on high-output manufacturing and cost-efficient processing. The segment benefits from demand in automotive, construction, packaging, and industrial plastic products, where material consistency and production speed remain important purchase factors.

By End Use

Industrial end use led the Methacrylate Butadiene Styrene market with 63.3% share, reflecting the material’s strong usage in durable plastic products and performance-based applications. The segment is supported by demand for impact modifiers, rigid plastics, and engineered components across manufacturing industries.

The industrial sector uses MBS due to its balance of toughness, clarity, flexibility, and processing stability. These properties make it suitable for applications where plastic products must withstand mechanical pressure, frequent handling, and long operating life.

The segment is expected to remain strong as industrial manufacturers continue to adopt advanced polymer materials for improved product quality and reliability. Growth is further supported by expansion in plastics processing, machinery components, construction materials, and industrial packaging applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Asia Pacific held 39.5% share in the Methacrylate Butadiene Styrene market, making it the leading regional market. The region’s position is supported by strong plastic manufacturing activity, high automotive production, expanding industrial output, and rising demand for performance polymers.

China, India, Japan, South Korea, and Southeast Asian countries play an important role in regional demand. These countries have large manufacturing bases for automotive parts, consumer goods, construction materials, and industrial plastic products, which supports steady MBS consumption.

The region is also benefiting from cost-efficient production, growing domestic demand, and increasing investments in polymer processing capacity. As industries continue to shift toward lightweight, durable, and process-friendly materials, Asia Pacific is expected to maintain its strong role in the Methacrylate Butadiene Styrene market.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +1.5% | Asia Pacific, 39.5% share in 2025 | Leads volume demand. |

China plastic processing strength | +1.0% | China | Drives regional consumption. |

India automotive and construction demand | +0.8% | India | Supports future growth. |

North America specialty plastics use | +0.6% | U.S. and Canada | Builds value demand. |

Europe performance additive demand | +0.5% | Germany, France, UK, Italy | Supports premium grades. |

Go-to-Market and Sales Economics

The Methacrylate Butadiene Styrene Market should be positioned through PVC compounders, packaging converters, medical packaging suppliers, appliance manufacturers, sheet extruders, film producers, and engineering plastic processors in 2026. Selling should focus on impact strength, transparency retention, low-temperature toughness, processing stability, crease-whitening resistance, and compatibility with rigid PVC and selected engineering resin systems.

Go-to-market planning should be application-led because MBS works as a performance modifier rather than a general-purpose resin. Arkema states that MBS impact modifiers are intended for PVC, engineering plastics, and thermosetting resins, offering clarity, crease-whitening resistance, impact resistance, and oil resistance in clear PVC applications.

Customer targeting should prioritize transparent PVC containers, injection molded parts, films, calendered sheets, pipes, blister packaging, cosmetic packaging, and selected consumer goods. U.S. major plastic resin production reached 8.9 billion pounds in April 2026, up 11.2% year over year, supporting a large downstream conversion base for modifiers.

Risk Factors & Market Barriers

The main market barrier is feedstock and polymer cost volatility. MBS depends on methyl methacrylate, butadiene, styrene, polymerization inputs, additives, energy, and purification systems. FRED reported the U.S. plastics material and resin manufacturing index at 377.676 in May 2026, compared with 303.509 in January 2026, showing strong cost movement.

Safety and compliance risk is also important because butadiene and styrene-linked operations require strict workplace and emissions control. OSHA limits 1,3-butadiene exposure to 1 ppm over an eight-hour time-weighted average and 5 ppm over 15 minutes. These limits increase the need for monitoring, ventilation, closed handling, and worker protection.

Substitution risk can affect adoption where buyers choose acrylic impact modifiers, CPE, ABS, or other polymer blends. Dow notes that MBS modifiers are often preferred for indoor applications where weatherability is not the main concern. Outdoor applications may require stronger UV performance, making formulation support important for customer retention.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities are strongest across transparent PVC packaging, PVC films and sheets, blow-molded containers, injection molded parts, medical packaging, cosmetic containers, appliance components, engineering resins, and CPVC-related applications. Kaneka lists MBS grades for PVC blow-molded containers, injection molded parts, film, pipe and high transparent films.

PVC-linked demand remains a major revenue base because MBS improves toughness without strongly reducing clarity. A 2026 PVC eco-profile notes that PVC is used in building and construction, window frames, pipes, fittings, flooring, roofing, electrical insulation, blisters, films, toys, signs, and credit cards. These applications support modifier demand.

Engineering plastics create additional value opportunities where impact strength and low-temperature performance are required. Arkema describes MBS use in engineering resin applications, including PC/ABS monitor housings, PC/PBT automotive bumpers, and PC cell phone housings. These higher-performance uses can support premium grades and customer-specific technical qualification.

Financial Impact

The financial impact in 2026 will depend on monomer cost, rubber core quality, shell polymer consistency, energy use, plant utilization, freight, and customer qualification. FRED reported synthetic rubber manufacturing primary products at 334.404 in May 2026, compared with 265.918 in January 2026, indicating pressure on rubber-based polymer chains.

Margins can improve where producers sell specialty MBS grades for clear PVC, medical packaging, premium film, high-clarity sheet, and engineered resin modification. Commodity grades may remain more exposed to price competition. Higher-value products can protect earnings when they reduce breakage, improve processing, and help converters meet strict clarity specifications.

Financial returns can be strengthened through long-term contracts, local warehousing, technical service, stable monomer sourcing, and strong quality testing. EPA’s chemical plant standards are expected to cut more than 6,200 tons of toxic air pollution annually from covered facilities, so compliance investment may raise costs but improve buyer confidence.

Drivers Impact Analysis

The Methacrylate Butadiene Styrene Market is driven by demand for impact modifiers used in PVC, engineering plastics, automotive components, packaging, and construction products. MBS improves toughness, clarity, weather resistance, and processability, making it important in applications where plastics need stronger impact performance.

Asia Pacific supports steady demand because of plastic processing, automotive parts production, industrial manufacturing, and construction material consumption. China, India, Japan, South Korea, and Southeast Asia remain important markets due to their strong manufacturing base and demand for durable polymer materials.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for impact modifiers | +1.1% | Asia Pacific, North America, Europe | Drives core usage. |

Growth in PVC processing applications | +0.9% | China, India, Southeast Asia, U.S. | Supports additive demand. |

Expansion of automotive plastic parts | +0.8% | Asia Pacific, Europe, North America | Improves material toughness. |

Demand for clear and durable plastics | +0.7% | Packaging, consumer goods, construction | Supports product adoption. |

Growth in industrial plastic components | +0.6% | Global manufacturing markets | Builds steady demand. |

Restraints Impact Analysis

The market faces restraints from raw material price volatility, especially methacrylate, butadiene, and styrene-based inputs. Since these materials are linked to petrochemical supply chains, cost movement can pressure margins and affect customer pricing.

Another restraint is competition from alternative impact modifiers and engineering polymers. Buyers may shift to acrylic impact modifiers, CPE, ABS, or other additives when they need specific performance, lower cost, or easier processing.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Raw material price volatility | -0.7% | Global producers | Pressures margins. |

Competition from alternative modifiers | -0.6% | Global plastics markets | Limits substitution. |

Environmental pressure on plastic additives | -0.5% | Europe, North America, developed Asia | Raises compliance burden. |

Limited awareness in smaller processors | -0.4% | Emerging markets | Slows adoption. |

Dependence on PVC and polymer cycles | -0.4% | Global | Affects demand stability. |

Opportunities Impact Analysis

Opportunities are growing in automotive parts, extrusion grade materials, rigid PVC products, transparent packaging, pipes, sheets, and industrial plastic components. MBS can benefit where manufacturers require strong impact resistance without losing clarity or processing efficiency.

Higher-value opportunities are also emerging in specialty grades for automotive, construction, and consumer goods. Producers that offer consistent quality, improved dispersion, and better compatibility with PVC and other polymers can capture stronger demand.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Automotive parts applications | +1.0% | Asia Pacific, Europe, North America | Builds durable demand. |

Extrusion grade MBS demand | +0.9% | PVC sheet and profile markets | Supports processing growth. |

Rigid PVC product expansion | +0.8% | Construction and packaging markets | Improves impact strength. |

Clear packaging and consumer goods | +0.6% | Global | Adds value demand. |

Specialty modifier grade development | +0.5% | U.S., Europe, Japan, China | Improves margin potential. |

Challenges Impact Analysis

The main challenge is maintaining stable performance across different polymer formulations. MBS must deliver impact strength, clarity, and compatibility without affecting processing speed, surface quality, or final product performance. Another challenge is balancing cost with performance. In price-sensitive markets, customers may choose lower-cost additives unless MBS provides clear benefits in durability, transparency, and product life.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining formulation compatibility | -0.6% | Global plastics processors | Affects performance quality. |

Balancing cost and impact strength | -0.5% | Emerging and mass markets | Influences buyer choice. |

Meeting product safety standards | -0.4% | Packaging and consumer applications | Raises compliance needs. |

Managing supply chain reliability | -0.4% | Asia Pacific, Europe, North America | Impacts production planning. |

Competing with low-cost modifiers | -0.3% | Asia Pacific and global markets | Reduces pricing power. |

Segment Covered in the Report

By Application

Automotive Parts

Consumer Electronics

Others

By Grade

Extrusion

Injection Molding

By End Use

Industrial

Consumer

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward extrusion grade MBS, rigid PVC modification, and automotive component applications. These areas require impact strength, dimensional stability, and smooth processing, which supports continued use of MBS additives.

Industrial applications are also gaining importance because manufacturers need durable plastic components for machinery, construction, electrical products, and consumer goods. Asia Pacific’s strong polymer processing base continues to shape production and consumption patterns.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Extrusion grade remains preferred | +1.0% | Asia Pacific, Europe, North America | Leads grade demand. |

Automotive parts remain key application | +0.9% | China, India, Japan, Europe | Supports material use. |

Industrial end use stays dominant | +0.8% | Global manufacturing regions | Drives steady demand. |

Rigid PVC impact modification grows | +0.7% | Construction and packaging markets | Improves product durability. |

Specialty transparent grades gain use | +0.5% | Consumer goods and packaging | Supports clarity demand. |

Investor Type Impact Matrix

Investors should focus on companies with strong raw material access, reliable polymerization capability, and established relationships with PVC processors, automotive suppliers, and industrial plastics manufacturers. These strengths help improve supply stability and customer retention.

Strategic investors can also target specialty MBS grades, regional compounding facilities, and application-specific technical support. Producers that offer consistent quality and customized performance grades are better positioned than suppliers competing only on price.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

MBS Manufacturers | +1.0% | Global | Expands additive capacity. |

Polymer Additive Producers | +0.9% | Asia Pacific, Europe, North America | Supports formulation demand. |

Automotive Plastic Suppliers | +0.8% | China, India, Europe, U.S. | Drives material usage. |

PVC and Industrial Plastic Processors | +0.7% | Global | Builds downstream demand. |

Private Equity and Strategic Investors | +0.5% | Specialty polymer markets | Supports capacity scaling. |

Recent Developments

In 2026, the Methacrylate Butadiene Styrene Market remained linked to demand for rigid and semi-rigid PVC, transparent sheets, window profiles, pipes, fittings, bottles, films, injection-molded parts, and engineering plastics. LG Chem continued to position MBS as a plastic modifier used in hard and semi-hard PVC and engineering plastics to improve impact strength, processability, surface properties, and foaming behavior.

Denka’s 2026 management presentation for "Mission 2030 Phase 2" covered FY2026 to FY2028, while its transparent polymer portfolio continued to include MBS resins with a balance of transparency, strength, and fluidity. This is important because transparent and high-impact polymers are being used across automobiles, home appliances, building materials, and food packaging materials.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

LG Chem Ltd.

Chi Mei Corporation

Toray Industries, Inc.

BASF SE

The Dow Chemical Company

INEOS Styrolution Group GmbH

Trinseo S.A.

Techno-UMG Co., Ltd.

Denka Company Limited

LOTTE Chemical Corporation

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Carbon Capture Chemicals Market Size to Reach USD 78.0 Billion by 2035

Carbon Capture Chemicals Market By Chemical Type (Amines, Carbonates, Ammonia-based Solvents, Ionic Liquids, Solid Sorbent Chemicals, Others), By Absorption Type (Chemical Absorption, Physical Absorption), By End-Use Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Application (Post-combustion Capture, Pre-combustion Capture, Industrial Gas Separation, Direct Air Capture, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Bio-based Chemicals Market Size to Hit USD 296.7 Bn by 2035

Bio-based Chemicals Market By Product Category (Platform Chemicals, Polymers for Plastics, Paints, Coatings, Inks and Dyes, Surfactants, Cosmetics and Personal Care Products, Adhesives, Man-made Fibers, Others), By Application (Industrial, Agricultural, Pharmaceutical, Others), By Source (Plant-based, Animal-based, Microbial-based, Waste-based), By End Use (Chemical Manufacturing, Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Processing Chemicals Market Size to Hit USD 14.6 Billion by 2035

Hydrogen Processing Chemicals Market By Chemical Type (Catalysts, Adsorbents, Solvents, Corrosion Inhibitors, Scavengers, Others), By Function (Reforming Chemicals, Purification Chemicals, Hydroprocessing Chemicals, Gas Treatment Chemicals, Corrosion Control Chemicals, Others), By Process (Steam Methane Reforming, Hydrocracking, Hydrotreating, Pressure Swing Adsorption, Water-Gas Shift Reaction, Others), By End Use (Refineries, Ammonia Production, Methanol Production, Petrochemicals, Clean Hydrogen Plants, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Electrolyte Chemicals Market to Cross USD 49.4 Billion by 2035

Electrolyte Chemicals Market By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, Others), By Electrolyte Form (Liquid Electrolytes, Gel, Solid-State Electrolytes), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, Industrial and Motive Batteries, Others), By Product Type (Lithium-Based Electrolytes, Sulfide-Based Electrolytes, Polymer-Based Electrolytes, Oxide-Based Electrolytes, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035