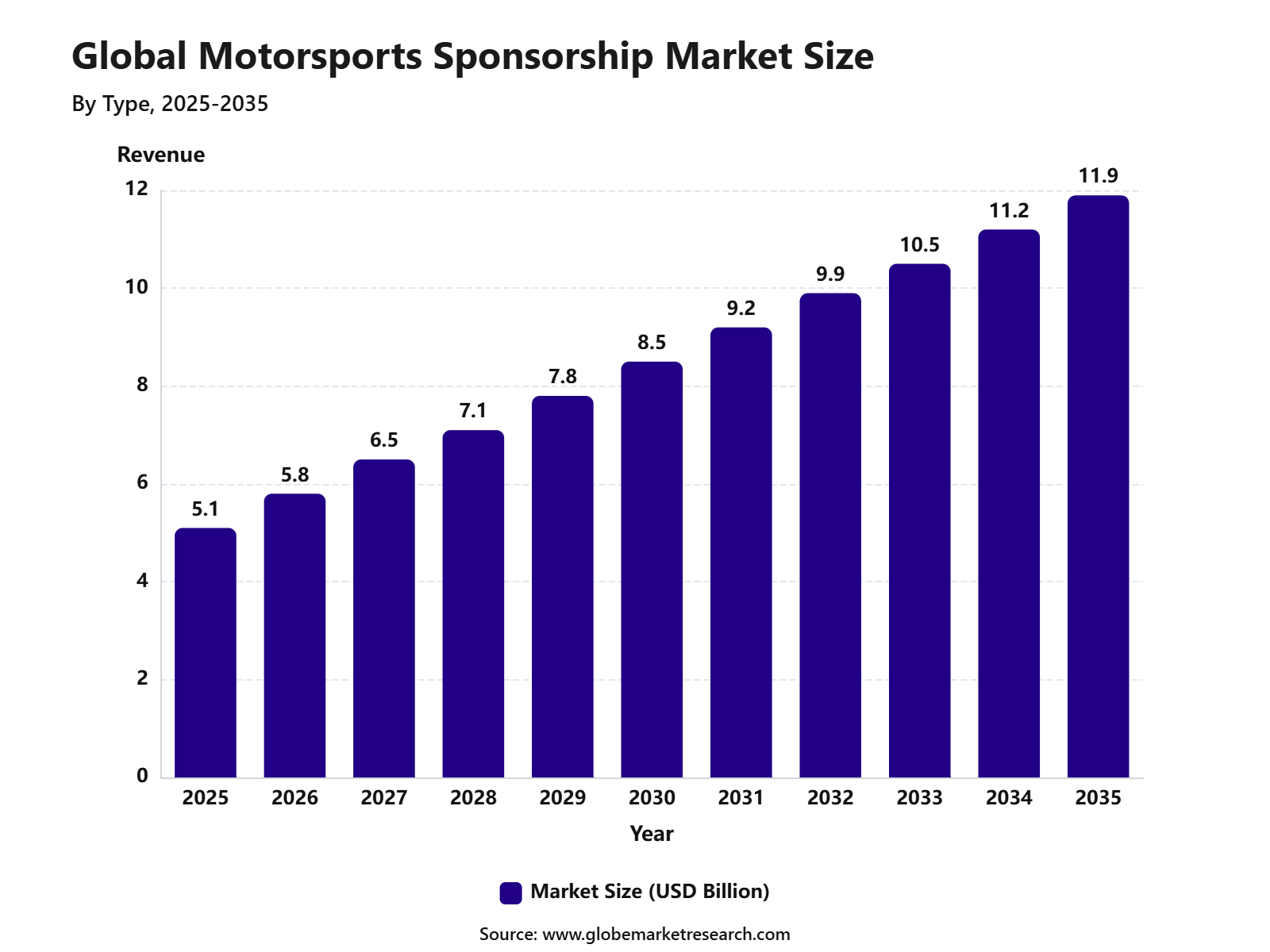

Revenue, 2025

$5.1Bn

Forecast, 2035

$11.9%

CAGR, 2026-2035

8.9%

Report Coverage

Global

Market Size and Forecast

The Global Motorsports Sponsorship Market was valued at USD 5.1 billion in 2025 and is projected to reach USD 11.9 billion by 2035, growing at a CAGR of 8.9% during the forecast period. North America held the largest regional share of 43.0% in 2025, supported by strong commercial activity across stock car racing, formula racing, off-road racing, and motorcycle racing. The region also benefits from a large motorsports fan base, established racing leagues, high brand participation, and strong media coverage across television, streaming, and digital platforms.

The growth of the motorsports sponsorship market can be attributed to increasing brand investment in live sports marketing, fan engagement, digital content, and experiential campaigns. Sponsors are using race teams, drivers, events, tracks, and esports platforms to build visibility and connect with loyal motorsports audiences. Automotive companies, energy and lubricant brands, technology firms, financial services providers, telecom companies, and consumer goods brands remain active participants in this market.

The market outlook remains positive as motorsports organizations expand their digital assets, streaming partnerships, social media reach, and data-driven sponsorship models. Demand is expected to increase for team sponsorship, driver sponsorship, event sponsorship, track branding, digital sponsorship, and sim racing sponsorship. As brands look for measurable audience engagement and long-term visibility, motorsports sponsorship is expected to remain an important channel for sports marketing and brand promotion.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Race teams led the market by type with 58.8% share, supported by strong brand visibility, fan engagement, media exposure, and direct association with competitive performance.

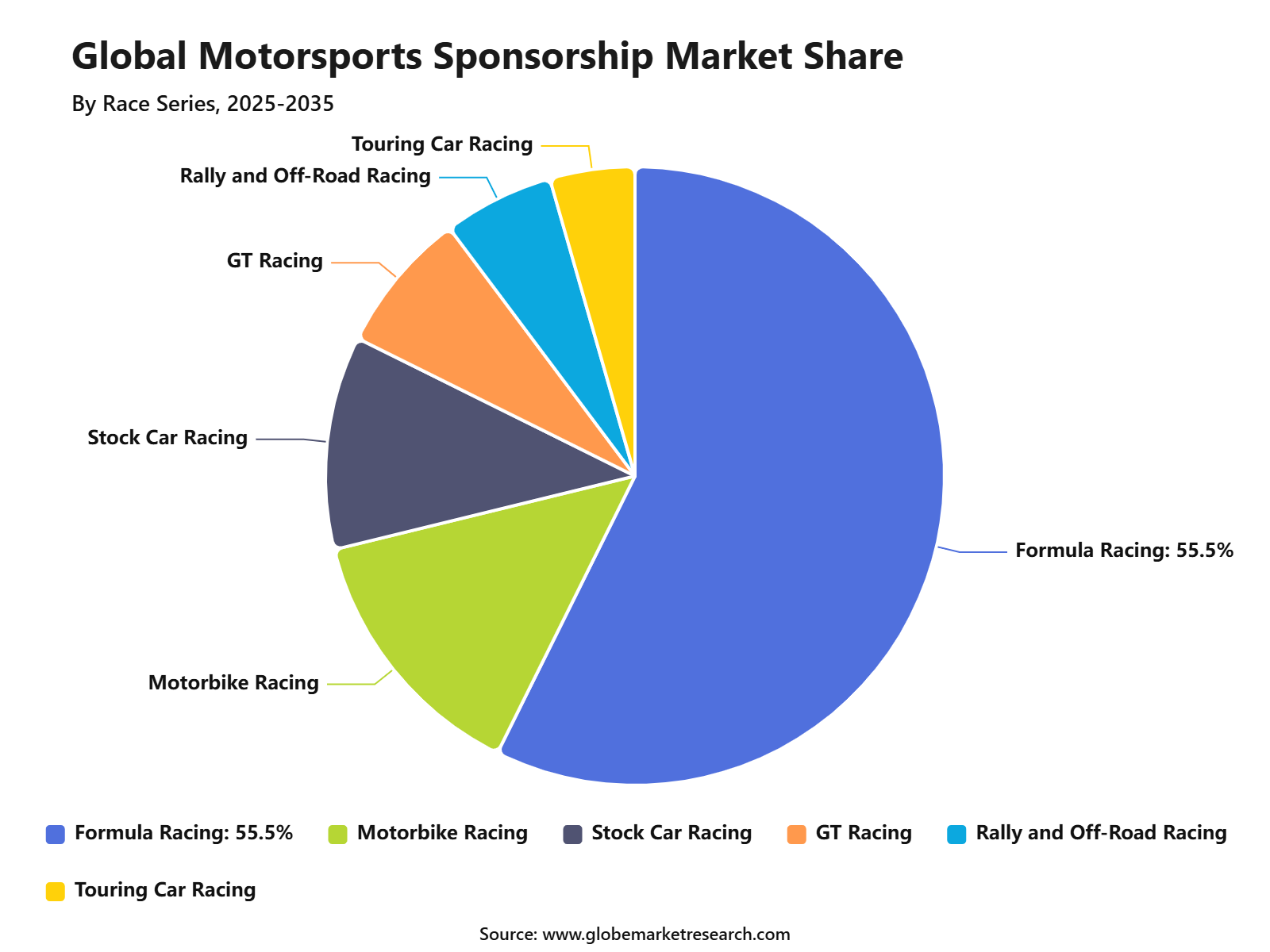

Formula racing accounted for 55.5% share by race series, driven by its global audience reach, premium sponsorship value, and strong appeal among automotive, technology, and lifestyle brands.

Automotive companies held 32.4% share by sponsor category, supported by close alignment with motorsport performance, vehicle branding, product promotion, and customer engagement.

Team sponsorship captured 43.7% share by sponsorship asset, driven by high logo visibility, driver association, race-day exposure, and long-term brand-building opportunities.

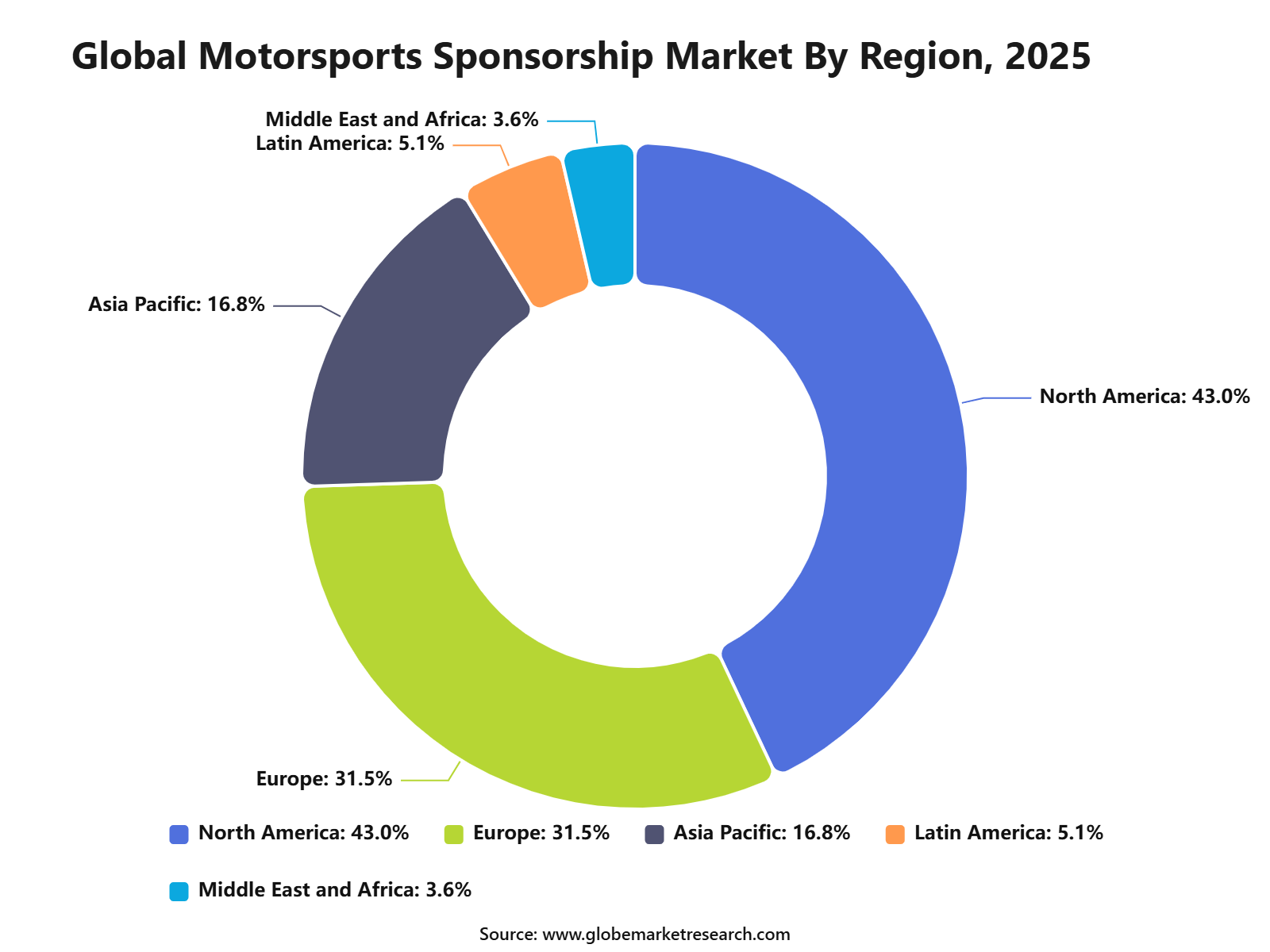

North America held 43.0% share of the motorsports sponsorship market, supported by strong racing culture, major motorsport events, large fan communities, and active brand sponsorship spending.

Go-to-Market Strategy

The Motorsports Sponsorship Market needs an audience-led and asset-led go-to-market strategy. Rights holders, race teams, drivers, leagues, and circuit owners should sell sponsorship around measurable exposure, fan engagement, hospitality, branded content, retail activation, digital campaigns, and business-to-business access. Formula 1 shows the strength of this model, with 2025 fan attendance reaching 6.75 million and live viewership rising 21% compared with 2024. Sponsorship revenue also became a larger part of Formula 1’s commercial base, accounting for 21.7% of total revenue in 2025, compared with 18.6% in 2024.

Sales economics are strongest when sponsorship is sold as a full-season performance platform rather than only as logo placement. Brands now expect broadcast exposure, social media content, driver access, fan data, VIP hospitality, product trials, retail promotions, and measurable return on marketing spend. MotoGP also supports this trend, as its 2025 season reached 3.6 million trackside attendees, TV audiences rose 9% per Grand Prix, Sprint viewership increased 26%, and its global fanbase reached 632 million.

Risk Factors & Market Barriers

The main risk in the Motorsports Sponsorship Market is uneven audience performance across racing series. Formula 1 has strong global momentum, but NASCAR’s 2025 Cup Series averaged 2.45 million viewers across the full 38-race season, down 14.7% year-on-year, partly due to a fragmented broadcast model. This creates a challenge for sponsors because media reach, audience quality, and broadcast consistency directly affect the value of sponsorship packages.

Another barrier is high competition for brand budgets from football, cricket, basketball, esports, influencers, streaming platforms, and digital advertising. Sponsors increasingly compare motorsports with lower-cost digital channels that provide clearer attribution. Motorsports properties must therefore prove value through verified media exposure, fan demographics, sales lift, lead generation, hospitality outcomes, and brand recall. Without strong measurement, sponsorship can be treated as an expensive awareness expense rather than a revenue-supporting investment.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape is spread across race team sponsorship, driver sponsorship, title sponsorship, trackside branding, race naming rights, hospitality, digital content, streaming integrations, esports, licensing, branded merchandise, and fan events. Formula 1 remains the most powerful global platform because it combines international races, premium hospitality, strong media rights, celebrity culture, and high-value sponsor categories. Reuters reported that Formula 1 drew a cumulative audience of 1.83 billion in 2025, with average viewership of 76.1 million per Grand Prix and sponsor visibility rising more than 90% since 2020.

NASCAR and MotoGP also offer strong revenue pools, but their positioning is different. NASCAR provides deep access to U.S. motorsport fans, retail activation, auto aftermarket brands, and regional loyalty. Its secondary series secured a new title sponsorship from O’Reilly Auto Parts for 2026, supported by 1.1 million average viewers and 17% year-on-year viewership growth on The CW. MotoGP is stronger for two-wheeler, youth, lifestyle, and international expansion campaigns, supported by rising attendance and a younger fan profile.

Financial Impact

The financial impact can be positive for teams and race organizers that package sponsorship with measurable business outcomes. Sponsorship revenue can support car development, driver programs, travel, content production, fan events, and commercial operations. For brands, the financial value comes from media exposure, customer acquisition, dealer traffic, product credibility, employee engagement, B2B relationships, and loyalty among racing fans. Formula 1’s 2025 revenue increased to USD 3.9 billion, with growth supported by sponsorship, media rights, hospitality, licensing, and digital advertising.

Financial risk remains high when sponsorship is bought without activation. A logo on a car, bike, helmet, or circuit wall may create awareness, but stronger returns usually come when sponsorship is connected to campaigns, retail offers, content, hospitality, and fan data. Sponsors should track cost per exposure, brand lift, social engagement, lead generation, dealer visits, e-commerce traffic, and hospitality conversion. Motorsports properties that provide transparent reporting and flexible activation rights will be better positioned to retain sponsors during periods of inflation, tariff pressure, or lower consumer spending.

Type Analysis

Race teams led the Motorsports Sponsorship Market with 58.8% share, supported by their direct visibility across vehicles, driver uniforms, garages, digital content, hospitality areas, and race broadcasts. Team sponsorship remains attractive because brands can connect with fans through consistent exposure across the full racing season.

The growth of this segment can be attributed to strong brand placement opportunities and deeper storytelling around drivers, team performance, engineering, and fan loyalty. Sponsors prefer race teams because they provide long-term association, measurable visibility, and strong activation opportunities across live events, social media, merchandise, and broadcast coverage.

Race Series Analysis

Formula racing accounted for 55.5% share, making it the leading race series segment in the Motorsports Sponsorship Market. The segment is supported by global viewership, premium brand positioning, international race calendars, and strong fan engagement across both traditional and digital channels.

The dominance of formula racing is being driven by its wide commercial appeal across automotive, technology, luxury, financial services, consumer goods, and telecom brands. Formula racing offers sponsors high-value exposure through team partnerships, race sponsorships, trackside branding, driver endorsements, hospitality programs, and digital campaigns.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFSponsor Category Analysis

Automotive companies captured 32.4% share, supported by the close connection between motorsports, vehicle performance, engineering, mobility technology, and brand heritage. Car manufacturers, EV companies, tire brands, lubricant companies, parts suppliers, and mobility firms use motorsports sponsorship to build trust, showcase performance, and connect with automotive enthusiasts.

The growth of this segment is also supported by the shift toward electric mobility, hybrid powertrains, advanced materials, connected vehicles, and performance technology. Motorsports provides automotive brands with a strong platform to promote innovation, test brand positioning, and reach high-intent audiences with strong interest in vehicles and performance culture.

Sponsorship Asset Analysis

Team sponsorship led the sponsorship asset segment with 43.7% share, supported by strong brand visibility across race cars, team apparel, pit crews, social media content, and media interviews. This asset type allows brands to build a deeper and more consistent identity with a racing team instead of only appearing at a single event.

The segment is preferred because it provides year-round exposure and strong fan association. Team sponsorship also supports content creation, hospitality experiences, product launches, employee engagement, and business-to-business networking, making it one of the most commercially valuable sponsorship formats in motorsports.

Regional Analysis

North America led the Motorsports Sponsorship Market with 43.0% share, supported by strong race culture, mature sports marketing budgets, large fan communities, and a well-developed sponsorship ecosystem. The region benefits from major racing formats, strong media coverage, large live audiences, and active brand participation across automotive, energy, financial services, consumer goods, and technology categories.

The growth of North America is being supported by the strength of NASCAR, IndyCar, Formula 1 events in the U.S., off-road racing, drag racing, and digital fan engagement. Brands are investing in motorsports sponsorship to improve audience reach, build customer loyalty, strengthen premium positioning, and create measurable marketing campaigns across live and digital channels.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +2.6% | U.S. and Canada | Leads sponsorship value. |

Europe motorsports heritage and fan base | +2.0% | UK, Germany, Italy, France | Supports premium deals. |

Asia Pacific racing expansion | +1.8% | Japan, China, India, Southeast Asia | Drives new sponsor demand. |

Middle East event investment | +1.3% | UAE, Saudi Arabia, Qatar, Bahrain | Builds premium sponsorship. |

Latin America motorsports audience growth | +0.8% | Brazil, Mexico, Argentina, Chile | Supports gradual adoption. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Digital-first sponsorship activation | +2.2% | Global | Boosts fan engagement. |

Growth of driver-led branding | +1.9% | North America, Europe, Asia Pacific | Improves personal connection. |

Streaming and social media partnerships | +1.7% | U.S., Europe, India, Japan | Expands sponsor reach. |

Sustainability-linked sponsorships | +1.3% | Europe, North America, GCC | Supports responsible branding. |

Premium hospitality and event experiences | +1.1% | Global racing hubs | Builds sponsor value. |

Investor Type Impact Matrix

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Automotive Sponsors | +2.2% | Global | Drives core spending. |

Technology and Telecom Companies | +1.8% | North America, Europe, Asia Pacific | Expands digital activation. |

Energy and Lubricant Brands | +1.6% | Global | Supports race partnerships. |

Media and Streaming Investors | +1.4% | U.S., Europe, Asia Pacific | Strengthens content reach. |

Private Equity and Sports Investors | +1.1% | North America, Europe, GCC | Supports asset scaling. |

Segment Covered in the Report

By Type

Race Teams

League Organizers and Promoters

Track Owners and Runners

By Race Series

Formula Racing

One-Make Series

Touring Car Racing

Stock Car Racing

GT Racing

Rally and Off-Road Racing

Motorbike Racing

By Sponsor Category

Automotive Companies

Energy and Lubricants

Technology Companies

Financial Services

Consumer Goods

Telecom and Media

Others

By Sponsorship Asset

Team Sponsorship

Driver Sponsorship

Event Sponsorship

Track and Venue Sponsorship

Digital and Streaming Sponsorship

Esports and Sim Racing Sponsorship

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising brand investment in sports marketing | +2.4% | North America, Europe, Asia Pacific | Drives sponsorship spending. |

Growing motorsports viewership | +2.1% | U.S., Europe, Middle East, Asia Pacific | Expands audience reach. |

Strong demand for digital fan engagement | +1.8% | Global | Improves sponsor visibility. |

Expansion of racing events and leagues | +1.6% | North America, Europe, GCC, Asia Pacific | Supports sponsorship inventory. |

Rising value of team and driver partnerships | +1.4% | Global motorsports hubs | Builds brand association. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High sponsorship cost | -1.2% | Premium racing series | Limits smaller sponsors. |

Economic uncertainty in advertising budgets | -1.0% | Global | Slows spending decisions. |

Dependence on event schedules | -0.8% | Global racing markets | Affects campaign continuity. |

Limited sponsor access in top-tier teams | -0.7% | Formula racing, stock car racing | Restricts entry options. |

Measurement challenges in sponsorship ROI | -0.6% | Global | Raises budget scrutiny. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in digital and streaming sponsorship | +2.2% | North America, Europe, Asia Pacific | Expands online exposure. |

Esports and sim racing sponsorship | +1.8% | U.S., Europe, Japan, South Korea | Opens younger audiences. |

Expansion in emerging racing markets | +1.6% | India, GCC, Southeast Asia, Latin America | Builds new sponsor demand. |

Electric and sustainable racing formats | +1.4% | Europe, North America, China | Supports green branding. |

Data-led sponsorship activation | +1.2% | Developed markets | Improves campaign returns. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Proving measurable sponsor ROI | -1.0% | Global | Affects renewal decisions. |

Brand safety and reputation risks | -0.8% | Global | Increases sponsor caution. |

Competition from other sports properties | -0.7% | North America, Europe, Asia Pacific | Pressures sponsorship pricing. |

Audience fragmentation across platforms | -0.6% | Global | Complicates media planning. |

Rising event operating costs | -0.5% | Racing teams and organizers | Pressures sponsorship packages. |

Recent Developments

January 2026, Standard Chartered joined Formula 1 as official partner

Formula 1 announced a multi-year partnership with Standard Chartered from 2026. The bank became the Official Wealth Management and Corporate and Investment Banking Partner of Formula 1. This development shows rising demand from financial services brands to use motorsport for global client engagement, premium hospitality, and brand positioning.

January 2026, McLaren Mastercard naming partnership became active

McLaren Racing’s expanded partnership with Mastercard became active from the 2026 season, with the team operating as McLaren Mastercard Formula 1 Team. The partnership is focused on fan access, experiences, and deeper consumer engagement. Independent motorsport sources have reported Mastercard’s 2026 title sponsorship value at around USD 90 million per year, although the official deal value was not disclosed by the parties.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 5.1 Billion |

Forecast Revenue (2035) | USD 11.9 Billion |

CAGR (2025-2035) | 8.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type (Race Teams, League Organizers and Promoters, Track Owners and Runners), By Race Series (Formula Racing, One-Make Series, Touring Car Racing, Stock Car Racing, GT Racing, Rally and Off-Road Racing, Motorbike Racing), By Sponsor Category (Automotive Companies, Energy and Lubricants, Technology Companies, Financial Services, Consumer Goods, Telecom and Media, Others), By Sponsorship Asset (Team Sponsorship, Driver Sponsorship, Event Sponsorship, Track and Venue Sponsorship, Digital and Streaming Sponsorship, Esports and Sim Racing Sponsorship) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Mercedes-AMG Petronas Formula One Team, Scuderia Ferrari, McLaren Racing, Ducati, Oracle Red Bull Racing, Alpine F1 Team, Haas F1 Team, Aston Martin Aramco Formula One Team, Team Penske, Cadillac F1 Team, Hendrick Motorsports, Ferrari, Joe Gibbs Racing, Other Key Players |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Mercedes-AMG Petronas Formula One Team

Scuderia Ferrari

McLaren Racing

Ducati

Oracle Red Bull Racing

Alpine F1 Team

Haas F1 Team

Aston Martin Aramco Formula One Team

Team Penske

Cadillac F1 Team

Hendrick Motorsports

Ferrari

Joe Gibbs Racing

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Automotive and Transportation

Used Car Market Size to Reach USD 2,529.2 billion by 2035

Global Used Car Market Size, Go-to-Market Strategy Analysis By Vehicle Type (Sports Utility Vehicle, Hatchbacks, Sedan and Others), By Fuel Type (Petrol, Hybrid, Diesel, Electric and Others), By Distribution Channel (Franchised Dealers, Independent Dealers, Online Platforms, Others), By End Use (Personal and Commercial), By Sales Channel (Online and Offline), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Inboard Electric Motors Market to hit 13.1 Bn by 2035

Global Inboard Electric Motors Market Size By Type(Low Power Below 10 HP, Medium Power 10 to 35 HP, Large Power Above 35 HP), By Application (Civil Entertainment, Municipal, Commercial, Other Applications), By Boat / Vessel Type (Recreational Boats, Yachts, Fishing Boats, Workboats, Passenger Boats, Commercial Vessels), By Battery Type (Lithium-ion Batteries, Lead-acid Batteries, Nickel-based Batteries, Other Battery Types), By Sales Channel (OEM, Aftermarket), By End User (Individual Boat Owners, Commercial Operators, Tourism and Leisure Operators, Municipal Authorities, Marine Transport Operators), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Automotive AI Agents Market to hit 16.5 Bn by 2035

Global Automotive AI Agents Market By Agent Type (Conversational AI Agents, Autonomous Driving AI Agents, Predictive Maintenance AI Agents, Fleet Management AI Agents and Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles (EVs), Autonomous Vehicles), By Application (Driver Assistance & Safety, In-Vehicle Virtual Assistants, Predictive Maintenance, Fleet & Logistics Management, Infotainment Personalization), By Deployment Type (Cloud-Based AI Agents, Edge/On-Board AI Agents, Hybrid Deployment), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Chauffeur Car Market to Exceed USD 403.8 Billion by 2035

By Service Type (Business Travel Services, Leisure Travel Services, Airport Transfers, Event-specific Services), By Vehicle Type (Luxury Cars, Executive Cars, SUVs, Vans, Limousines), By Customer Type (Corporate Clients, Individual Customers, Tourist and Leisure Travelers), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035