Revenue, 2025

$ 365.6 Bn

Forecast, 2035

$ 705.9 Bn

CAGR, 2025-2035

6.8%

Report Coverage

Global

Market Size and Forecast

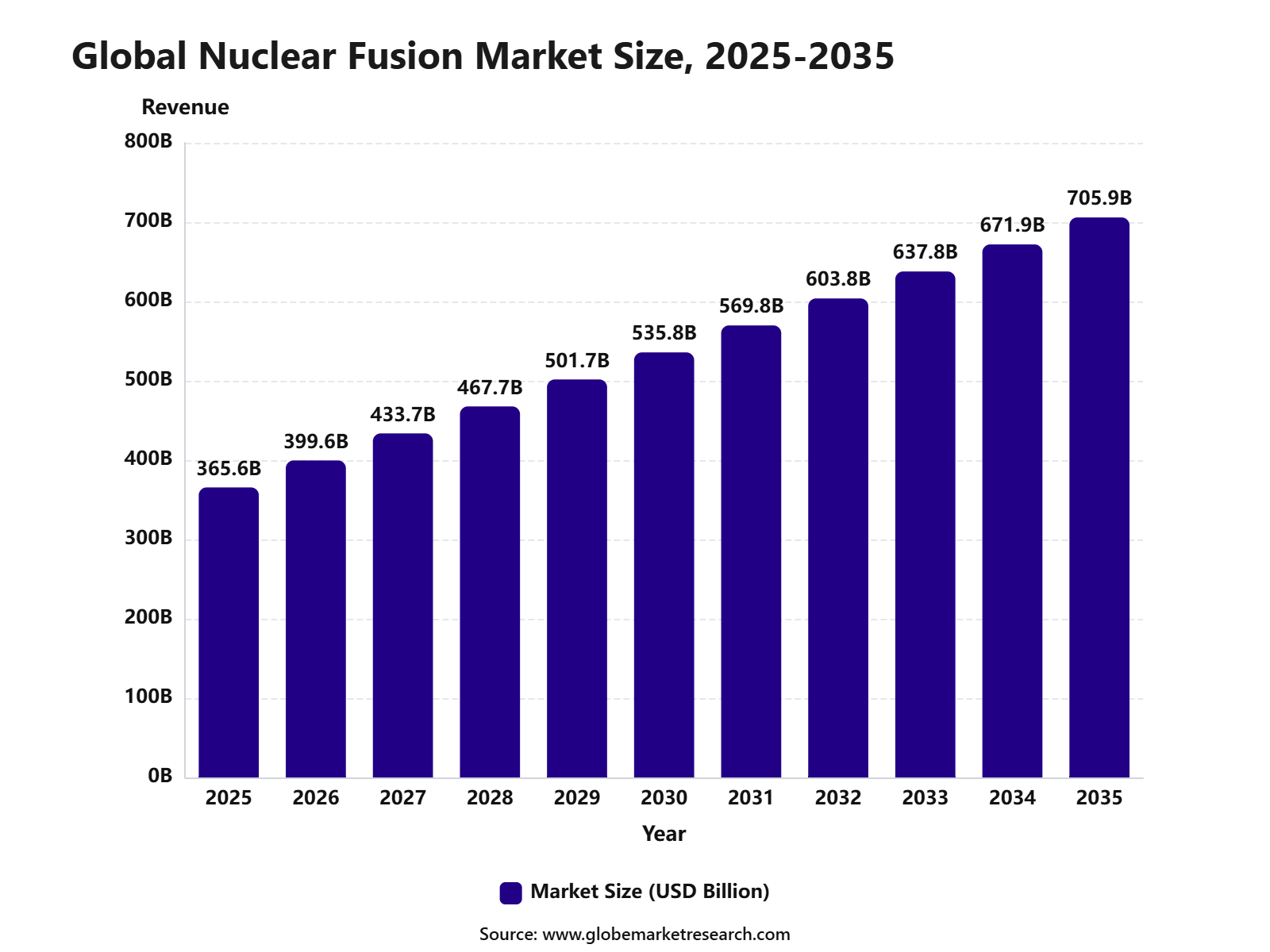

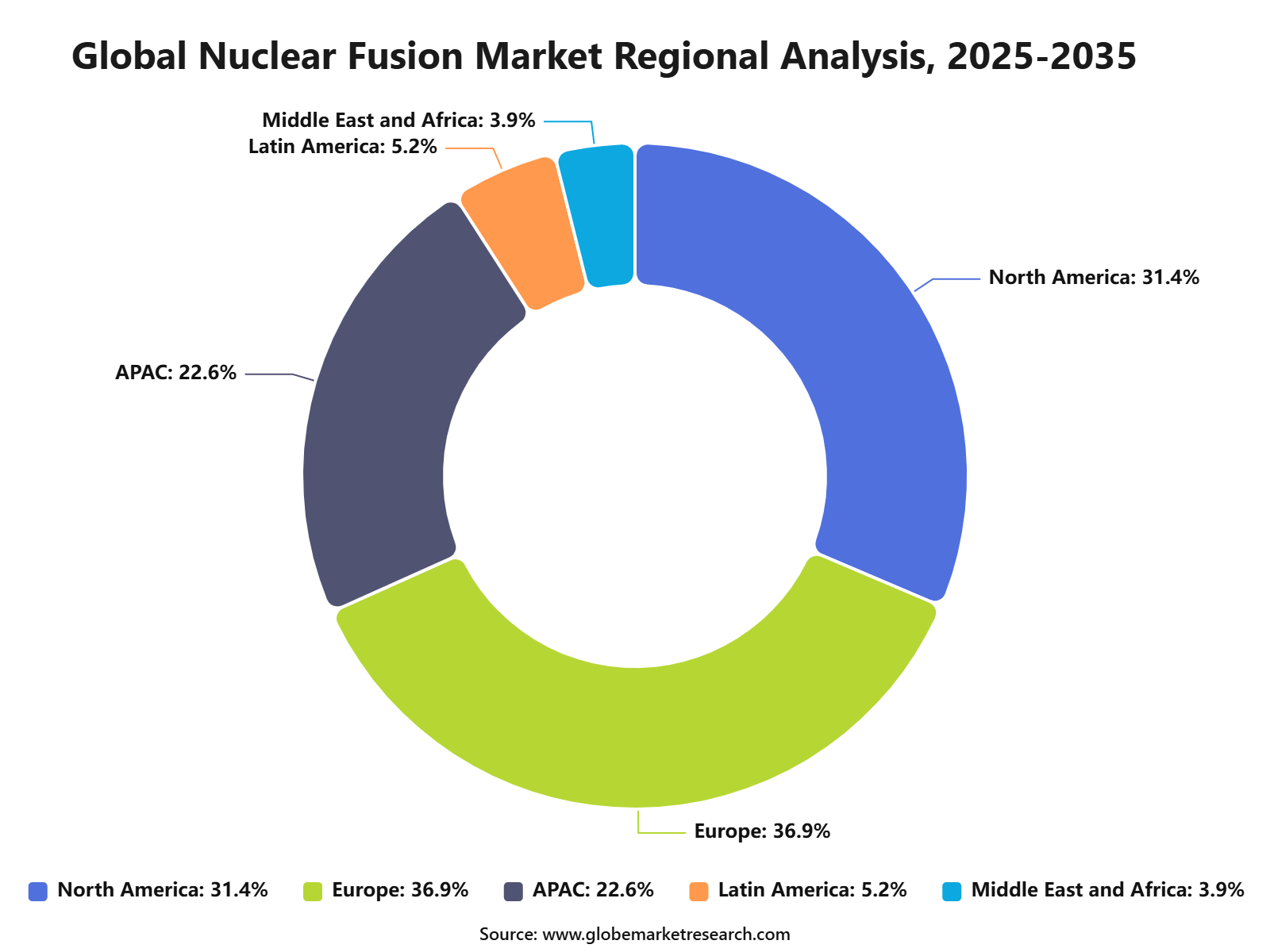

The Global Nuclear Fusion Market was worth USD 365.6 billion in 2025 and is expected to reach USD 705.9 billion by 2035, growing at a CAGR of 6.8% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 399.6 billion in 2026. Europe held the largest regional share of 36.9% in 2025, valued at around USD 134.9 billion, supported by strong fusion research programs, public funding, advanced energy infrastructure, and long-term clean energy investment.

The Nuclear Fusion Market includes technologies, systems, materials, and services focused on producing energy through fusion reactions. It covers magnetic confinement systems, inertial confinement systems, plasma heating, superconducting magnets, tritium handling, reactor components, diagnostics, and supporting engineering services. The market is closely linked with clean power generation, advanced nuclear research, energy security, and next-generation grid technologies.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 365.6 Billion |

Projected Revenue, 2035 | USD 705.9 Billion |

CAGR (2025-2035) | 6.8% |

Largest Region | Europe (36.9%, USD 134.9 Bn) |

Fastest Growing Region | Asia Pacific |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The market outlook remains positive as governments, laboratories, and private companies continue investing in fusion as a long-term clean energy solution. Growth can be attributed to rising demand for low-carbon power, stronger energy independence goals, and progress in plasma control and reactor design. The expansion of European fusion projects, public-private partnerships, and advanced materials development is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Inertial confinement led the technology segment with 73.2% share, supported by strong research activity, high-energy laser development, and its potential for controlled fusion energy generation.

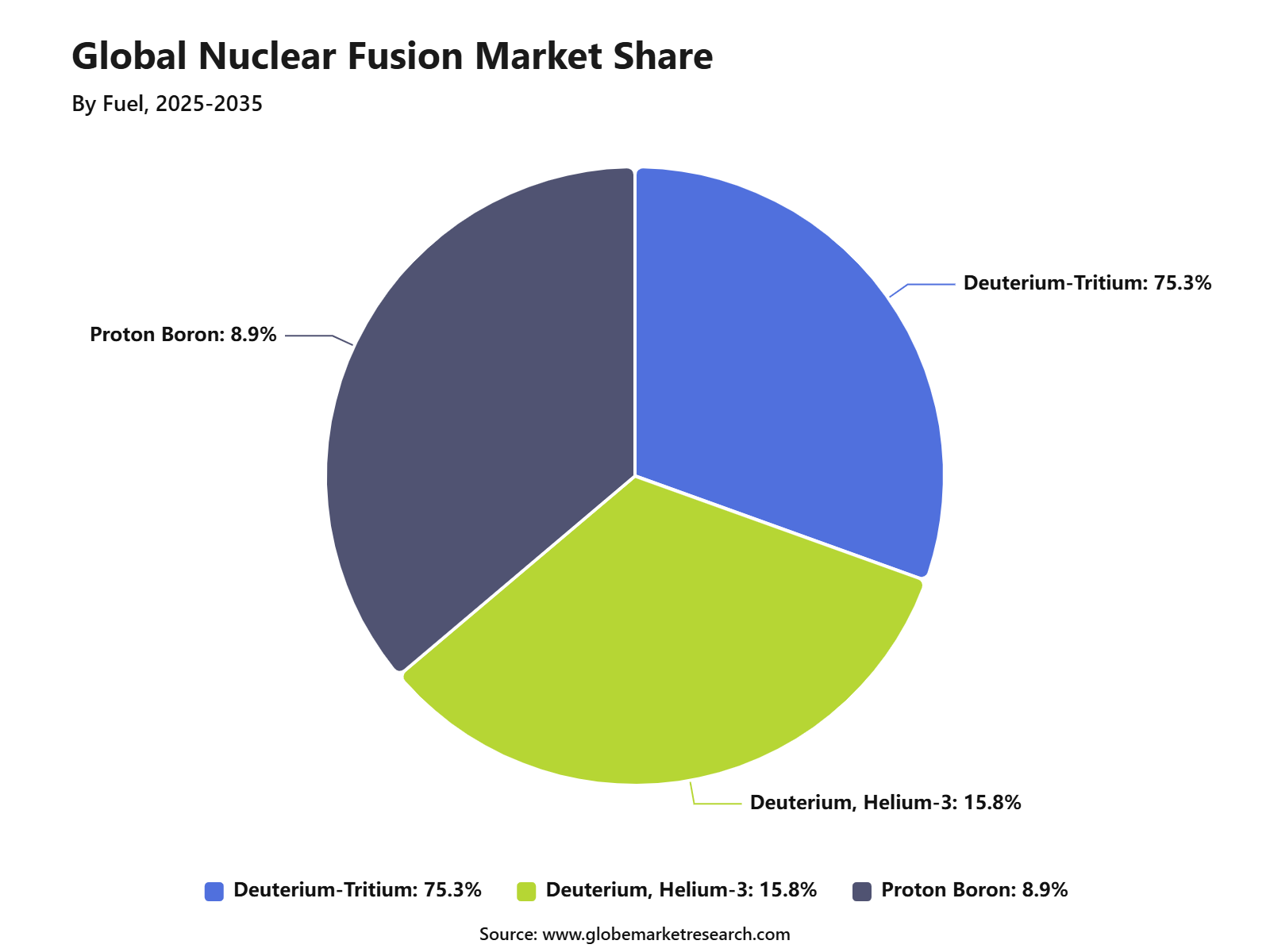

Deuterium-tritium fuel accounted for 75.3% share, driven by its high fusion reaction efficiency, established use in experimental fusion systems, and strong relevance for next-generation reactor development.

Europe led the nuclear fusion market with 36.9% share, valued at USD 134.9 billion, supported by major fusion research programs, strong public funding, advanced scientific infrastructure, and active collaboration across energy and research institutions.

Top Funding and Investment

Top Investments

The UK Government committed over £2.5 billion to fusion energy over financial years 2025 to 2026 through 2029 to 2030. The allocation includes £1.3 billion for UK Fusion Energy and STEP, £740 million for R&D infrastructure, £180 million for LIBRTI, £125 million for the Culham AI Growth Zone, and £50 million for fusion skills training for more than 2,000 people.

Germany approved a national Fusion Action Plan with more than €2 billion to be invested by 2029. The funding is targeted at fusion research, research infrastructure, pilot projects, industry participation, value-chain development, and Germany’s goal of building a commercial fusion power plant.

The UK Atomic Energy Authority advanced its £200 million Lithium Breeding Tritium Innovation, LIBRTI, programme. The programme is focused on tritium breeding, fusion fuel development, and lithium blanket technologies. UKAEA also announced £9 million for 12 smaller tritium breeding and digital simulation experiments.

The U.S. Department of Energy announced USD 134 million for fusion research and innovation programmes. This included USD 128 million for FIRE Collaboratives and USD 6.1 million for INFUSE projects, supporting materials science, laser technology, superconducting magnets, AI-based fusion modelling, and private-sector fusion development.

Proxima Fusion, RWE, Bavaria, and the Max Planck Institute for Plasma Physics signed an agreement to build the Alpha stellarator demonstrator in Garching and plan the Stellaris commercial power plant at RWE’s Gundremmingen site. Bavaria indicated a potential 20% state contribution, while Proxima planned to finance about 20% of project costs through private investment.

Top Funding

Commonwealth Fusion Systems raised USD 863 million in a Series B2 round. The company stated that the funding will be used to complete SPARC, its fusion demonstration machine, and support development work on its first ARC power plant in Virginia. CFS also reported that it had raised close to USD 3 billion to date.

Helion Energy raised USD 465 million in a Series G round led by Thrive Capital. The company said the funding will support commercial deployment, expand U.S. fusion manufacturing capacity, and advance its first fusion power plant, Orion, which is under construction in Malaga, Washington. The round valued Helion at USD 15.5 billion post-money.

Proxima Fusion raised €411 million, around USD 468 million, in financing led by XTX Ventures and East X Ventures, with RWE and Google as strategic investors. The company said the funding will support Alpha, its net-energy stellarator demonstrator, high-temperature superconducting cable and magnet production, and engineering scale-up.

Top Acquisitions

Trump Media & Technology Group and TAE Technologies signed a definitive all-stock merger agreement valued at more than USD 6 billion. What is being combined is TAE’s nuclear fusion technology platform with Trump Media’s public-market structure and capital access. The companies said shareholders of both sides would own about 50% each of the combined company on a fully diluted basis.

General Fusion entered a business-combination agreement with Spring Valley Acquisition Corp. III, implying about USD 1 billion pro-forma equity value. What is being combined is General Fusion’s Magnetized Target Fusion technology, including its LM26 demonstration machine, with Spring Valley’s public-market vehicle. The proceeds are intended to support LM26 and help General Fusion list on Nasdaq.

By Technology

Inertial confinement accounted for 73.2% share of the Nuclear Fusion Market. This leading position is supported by its strong use in high-energy fusion research, where powerful lasers or particle beams are used to compress fuel pellets and create fusion conditions.

The technology is gaining attention because it can achieve extremely high temperature and pressure within a very short time. Research centers are using inertial confinement to study plasma behavior, fuel ignition, energy gain, and advanced fusion system design.

Demand for inertial confinement is expected to remain strong as public and private funding continues to support fusion demonstration projects. Its role in scientific validation, energy research, and future clean power development makes it a key technology segment in the market.

By Fuel

Deuterium-tritium fuel accounted for 75.3% share of the Nuclear Fusion Market. This dominance can be attributed to its high fusion reaction efficiency and lower ignition temperature compared with many alternative fusion fuel combinations.

The segment is widely used in experimental fusion systems because deuterium and tritium can produce strong energy output under controlled plasma conditions. This makes the fuel combination highly relevant for tokamaks, stellarators, inertial confinement systems, and other fusion research platforms.

Demand for deuterium-tritium fuel is expected to remain strong as fusion developers work toward commercial-scale energy generation. However, tritium supply, fuel handling, and breeding technologies will remain important areas of investment for long-term fusion deployment.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Region

Europe accounted for 36.9% share of the Nuclear Fusion Market, reaching USD 134.9 billion. The region’s leadership is supported by large fusion research programs, advanced scientific infrastructure, and strong policy focus on clean energy innovation.

Countries such as France, Germany, the United Kingdom, Italy, and Spain are key contributors to regional fusion activity. Europe benefits from established research institutions, public funding support, engineering expertise, and participation in major international fusion projects.

Europe is expected to maintain a strong position as fusion technology moves from research toward demonstration and early commercial planning. Demand will remain supported by clean energy targets, advanced reactor development, plasma research, and long-term investment in low-carbon power systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Europe leads the Nuclear Fusion Market with 36.9% share in 2025, valued at around USD 134.9 billion, supported by strong fusion research funding, advanced laboratories, international collaborations, and a mature nuclear engineering supply chain. Germany, France, the UK, Italy, and Spain remain major contributors.

North America remains important because of private fusion investment, national laboratory programs, venture-backed reactor developers, and advanced energy technology funding. Asia Pacific supports future growth through large energy demand, government-backed fusion programs, and strong manufacturing ecosystems in China, Japan, South Korea, and India.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Europe market leadership | +2.4% | Europe, 36.9% share in 2025 | Leads global value demand. |

Germany, France, and UK research strength | +1.5% | Western Europe | Drives regional development. |

North America private fusion investment | +1.2% | U.S. and Canada | Supports commercialization. |

Asia Pacific national fusion programs | +1.0% | China, Japan, South Korea, India | Builds future scale. |

Global supply chain collaboration | +0.8% | Europe, North America, Asia Pacific | Supports project execution. |

Go-To-Market and Sales Economics

Nuclear fusion is moving to market through public-private programs, power purchase agreements, technology licensing, pilot plants, and specialist supply-chain contracts. The U.S. Department of Energy stated in June 2026 that more than USD 10 billion in private investment is already advancing fusion technologies and demonstration projects, supporting a stronger commercialization base.

Sales economics are being shaped by high-demand clean power buyers, especially data centers, heavy industry, and utilities. IEA projects global electricity generation for data centers to rise from 460 TWh in 2024 to over 1,000 TWh by 2030, creating demand for firm, low-carbon power sources such as advanced nuclear and fusion.

Commercial models are becoming more visible through private financing and early offtake structures. Helion raised USD 465 million in June 2026 and is working toward a fusion power plant for Microsoft, while Commonwealth Fusion Systems stated in April 2026 that it has raised almost USD 3 billion since 2018.

Risk Factors & Market Barriers

The main barrier is technology readiness. Fusion plants still need proven solutions for structural materials, plasma-facing components, confinement systems, fuel cycle, blankets, and plant engineering. DOE’s fusion roadmap identifies these as core gaps that must be closed before commercial power can be delivered reliably and at scale.

Supply-chain maturity is another major risk. The Fusion Industry Association reported in 2026 that 75% of suppliers invested to expand fusion capacity, but 69% still lacked long-term demand visibility. This limits planning for magnets, lasers, vacuum systems, power electronics, fuel systems, heat management, and extreme-condition materials.

Regulation and fuel strategy also affect deployment timelines. The U.S. NRC is developing a fusion-specific framework, while DOE materials note that future fusion plants must solve tritium supply, recovery, recycling, and breeding-blanket requirements. These issues can affect permitting, safety review, plant design, and project financing.

Revenue Potential Analysis

Revenue Landscape Across

Revenue is expected across demonstration plants, magnets, superconductors, lasers, plasma systems, tritium handling, robotics, diagnostics, power electronics, heat exchangers, advanced materials, software, and engineering services. FIA reported that fusion supply-chain spending increased 24% in 2025, while 70% of fusion companies saw established suppliers pivoting toward fusion opportunities.

Europe is becoming a strong revenue landscape through government-backed pilots and large private rounds. Proxima Fusion raised EUR 411 million in July 2026 to accelerate its Alpha demonstration facility, while Focused Energy raised USD 240 million in May 2026 for laser fusion development. These investments support equipment, facilities, suppliers, and specialist workforce demand.

The UK is also building a project-led revenue base. In March 2026, the government announced a GBP 200 million Construction Partner contract for the STEP prototype fusion powerplant at West Burton, backed by GBP 1.3 billion of funding. This supports engineering, construction, manufacturing, and regional industrial renewal.

Financial Impact

Nuclear fusion can create long-term financial value by offering firm clean electricity with low fuel cost exposure once commercial plants are proven. Its near-term financial impact is already visible through private capital, public grants, supplier investment, engineering contracts, and strategic offtake agreements with power-intensive buyers such as technology companies.

Capital intensity remains high, so financial returns depend on milestone delivery, plant uptime, component lifetime, regulatory certainty, and cost reduction through repeat manufacturing. A 2026 fusion costing framework highlighted magnets, lasers, power supplies, power-core components, tritium handling, and plant integration as major cost drivers that require transparent project-level modelling.

The strongest financial impact is expected where fusion supports data centers, industrial heat, grid reliability, defense energy needs, and clean baseload power. However, investors should treat revenue timing carefully because most projects are still pre-commercial. Companies with validated physics, strong supply chains, public funding, and clear customer offtake are better positioned.

Drivers Impact Analysis

The Nuclear Fusion Market is driven by rising demand for clean baseload energy, long-term energy security, low-carbon power generation, plasma research, advanced magnets, fusion fuel systems, and high-performance reactor materials. Governments and private companies are investing in fusion because it can support future electricity needs with lower greenhouse gas emissions.

Europe leads the market due to strong public research funding, advanced fusion laboratories, international reactor projects, and a mature nuclear engineering base. Germany, France, the UK, Italy, and Spain remain important contributors because of their strong energy research ecosystems and industrial supply chains.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for clean baseload power | +1.9% | Europe, North America, Asia Pacific | Drives long-term fusion investment. |

Strong government research support | +1.6% | Europe, U.S., Japan, China | Supports technology development. |

Growth in private fusion companies | +1.3% | U.S., UK, Germany, Canada | Adds commercialization momentum. |

Energy security and grid stability needs | +1.1% | Europe and energy-importing regions | Strengthens strategic demand. |

Advances in superconducting magnets | +0.9% | Fusion research and reactor developers | Improves reactor feasibility. |

Restraints Impact Analysis

The market faces restraints from high capital cost, long commercialization timelines, technical complexity, and uncertain power plant economics. Fusion systems require advanced plasma control, high-temperature materials, tritium handling, magnets, diagnostics, and precision engineering.

Another restraint is the lack of commercial-scale operating experience. Investors and utilities still need proof of reliable net energy output, plant availability, fuel cycle management, and cost competitiveness before large-scale deployment can accelerate.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High reactor development cost | -1.0% | Global fusion developers | Limits faster commercialization. |

Long technology validation timeline | -0.9% | Public and private projects | Delays market maturity. |

Plasma confinement complexity | -0.8% | Tokamak, stellarator, laser fusion systems | Raises technical risk. |

Tritium supply and handling concerns | -0.7% | Future fusion power plants | Adds fuel cycle challenge. |

Uncertain commercial power economics | -0.6% | Utilities and investors | Affects investment confidence. |

Opportunities Impact Analysis

Opportunities are strong in fusion reactor components, superconducting magnets, plasma heating systems, neutron-resistant materials, tritium breeding systems, diagnostics, power conversion systems, and specialized engineering services. These areas benefit from continued R&D and early-stage commercialization efforts.

Higher-value opportunities are also emerging in compact fusion reactors, fusion pilot plants, fusion supply chains, advanced materials testing, high-temperature superconductors, and public-private partnerships. Companies that provide reliable components, engineering expertise, and scalable manufacturing can capture long-term value.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Fusion pilot plant development | +1.8% | Europe, U.S., China, Japan | Builds commercialization pathway. |

Superconducting magnet supply | +1.5% | Europe, U.S., Japan, South Korea | Supports reactor performance. |

Advanced plasma control systems | +1.2% | Research and private fusion projects | Improves operating stability. |

Tritium breeding and fuel systems | +1.0% | Future power plant developers | Adds strategic value. |

Fusion materials and component testing | +0.8% | Europe and advanced research hubs | Supports reactor durability. |

Challenges Impact Analysis

The main challenge is proving continuous, reliable, and economically viable fusion power. Scientific progress is strong, but commercial energy systems must meet strict requirements for uptime, safety, maintenance, grid connection, and lifetime cost.

Another challenge is building a qualified industrial supply chain. Fusion needs specialized suppliers for magnets, vacuum systems, cryogenics, lasers, power electronics, shielding, sensors, and high-performance materials.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Achieving commercial net energy output | -0.9% | Global fusion developers | Determines market credibility. |

Building reliable reactor supply chains | -0.8% | Europe, U.S., Asia Pacific | Affects project execution. |

Managing extreme heat and neutron damage | -0.7% | Reactor material suppliers | Impacts plant lifetime. |

Ensuring fuel cycle readiness | -0.6% | Future fusion power projects | Supports operational scale. |

Attracting patient long-term capital | -0.5% | Public and private investors | Influences commercialization speed. |

Segment Covered in the Report

By Technology

Inertial Confinement

Magnetic Confinement

By Fuel

Deuterium-Tritium

Deuterium, Helium-3

Proton Boron

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Market Trend Analysis

The market trend is moving toward compact fusion designs, high-temperature superconducting magnets, private fusion startups, public-private partnerships, advanced plasma diagnostics, and pilot power plant planning. Companies are focusing on faster development cycles and modular reactor concepts.

Europe remains the leading value region because of strong research infrastructure and public funding support. North America and Asia Pacific are also gaining momentum through private investment, national energy strategies, and growing demand for clean firm power.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Compact fusion reactor concepts expand | +1.7% | U.S., UK, Europe, Canada | Supports faster commercialization. |

High-temperature superconducting magnets rise | +1.4% | Europe, U.S., Japan | Improves reactor design. |

Public-private fusion partnerships grow | +1.2% | Europe and North America | Shares development risk. |

Pilot plant planning increases | +1.0% | Europe, U.S., China, Japan | Builds market readiness. |

Fusion supply chain specialization strengthens | +0.8% | Advanced manufacturing regions | Supports component demand. |

Investor Type Impact Matrix

Investors should focus on fusion companies with strong reactor design, magnet technology, plasma control capability, material science expertise, and access to public-private funding. Long development timelines mean technical validation, milestone discipline, and supply chain readiness are key success factors.

Strategic investors can also target superconducting magnet suppliers, plasma diagnostics firms, fusion engineering contractors, tritium fuel cycle companies, advanced material developers, and remote maintenance technology providers. Companies that reduce technical risk and support pilot plant readiness are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Fusion Reactor Developers | +1.5% | Global | Expands future power generation platforms. |

Superconducting Magnet Suppliers | +1.2% | Europe, U.S., Japan, South Korea | Supports core reactor systems. |

Plasma Control and Diagnostics Companies | +1.0% | Research and pilot plant markets | Improves operating performance. |

Advanced Nuclear Material Suppliers | +0.8% | Europe, North America, Asia Pacific | Supports reactor durability. |

Strategic Clean Energy Investors | +0.7% | Global energy transition markets | Funds long-term commercialization. |

Recent Developments

June 2026: General Fusion and Renexia signed a framework agreement to plan commercial fusion deployment in Italy, covering siting, development, funding, construction and commissioning of magnetized target fusion plants.

May 2026: Tokamak Energy joined Type One Energy and AECOM to form the UK Infinity Fusion Consortium, targeting the first private-sector-led commercial fusion power plant project in the United Kingdom

June 2025: Commonwealth Fusion Systems signed a strategic partnership with Google, including a 200 MW power purchase agreement from its first ARC fusion power plant in Virginia

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Zap Energy

First Light Fusion

General Fusion

TAE Technologies

Commonwealth Fusion Systems

Tokamak Energy

Lockheed Martin

Hyperjet Fusion

Marvel Fusion

Helion Energy

HB11 Energy

Type One Energy

Agni Fusion Energy

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Small Wind Turbine Market to Hit USD 17.9 Billion by 2035

Small Wind Turbine Market Size, Share, Analysis By Axis Type (Horizontal Axis Wind Turbines and Vertical Axis Wind Turbines), By Capacity Rating (0 To 5 KW, 6 To 20 KW, and 21-100 KW), By Connectivity (Off-Grid, On-Grid, and Hybrid), By Installation Location (Rooftop/Building-Integrated and Freestanding Tower), By Application (Residential, Commercial, and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035