Revenue, 2025

$ 2.1 Bn

Forecast, 2035

$ 11.2 Bn

CAGR, 2025-2035

18.2%

Report Coverage

Global

Market Size and Forecast

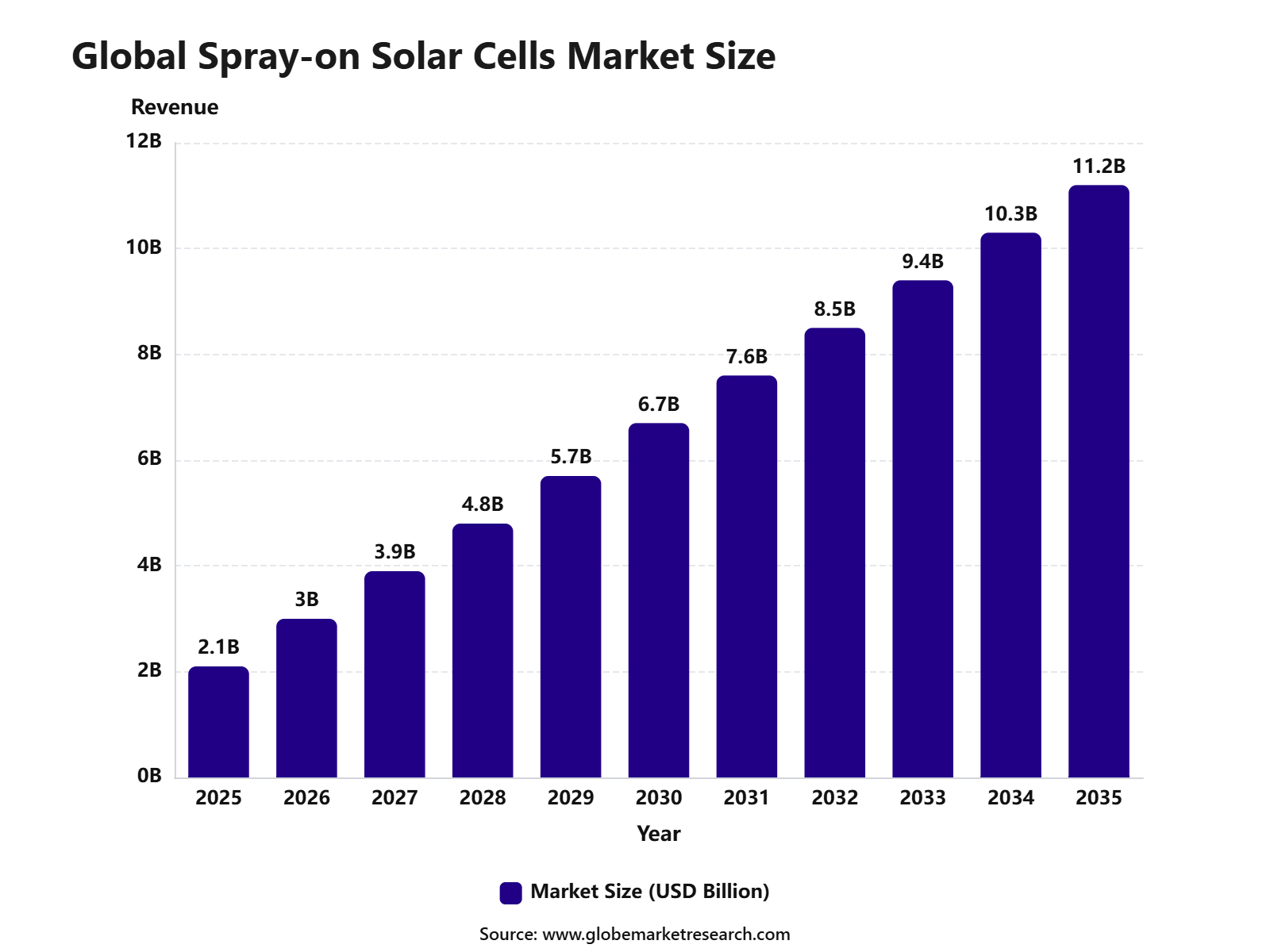

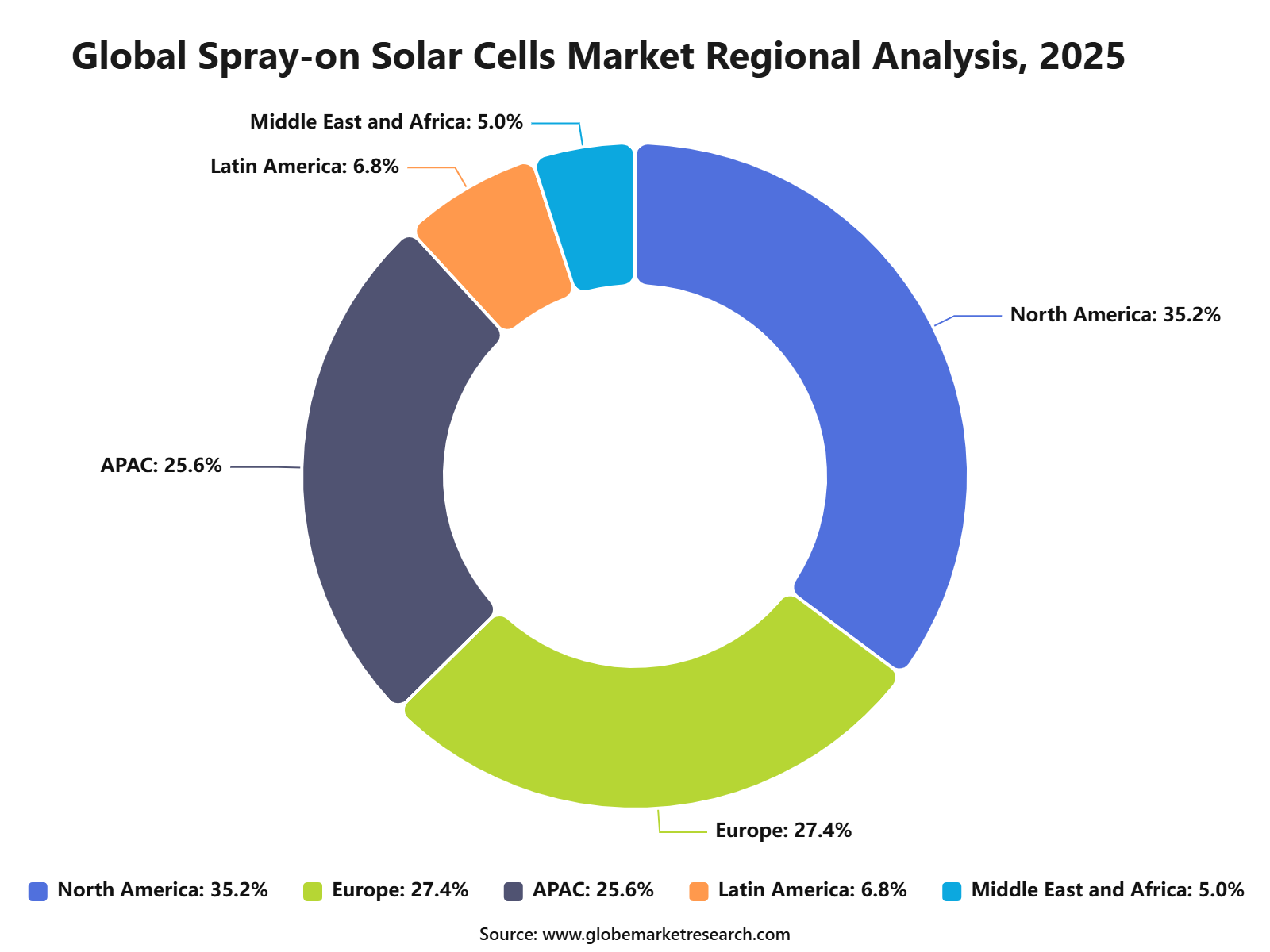

The Global Spray-on Solar Cells Market was worth USD 2.1 billion in 2025 and is expected to reach USD 11.2 billion by 2035, growing at a CAGR of 18.2% from 2025 to 2035. Based on this growth rate, the market is estimated to reach around USD 3.0 billion in 2026. North America held the largest regional share of 35.2% in 2025, supported by strong solar technology research, clean energy investments, advanced material innovation, and rising demand for lightweight and flexible photovoltaic solutions.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 2.1 Billion |

Projected Revenue, 2035 | USD 11.2 Billion |

CAGR (2025-2035) | 18.2% |

Largest Region | North America |

Fastest Growing Region | Asia Pacific |

Market Concentration/Structure | Medium/Moderately Fragmented |

Base Year | 2025 |

Forecast Period | 2025-2035 |

What is the Spray-on Solar Cells Market?

The Spray-on Solar Cells Market includes thin-film and printable photovoltaic technologies that can be applied onto surfaces through spray coating, ink-based deposition, or solution processing methods. These cells are used in building-integrated photovoltaics, portable electronics, vehicles, smart windows, flexible panels, and off-grid power systems. The market is closely linked with nanomaterials, perovskite solar cells, organic photovoltaics, and low-cost solar manufacturing.

The market outlook remains strong as industries seek lighter, cheaper, and more adaptable solar energy solutions. Growth can be attributed to rising demand for flexible solar modules, renewable energy integration, and scalable coating-based production methods. The expansion of perovskite research, printed electronics, and energy-generating surfaces is expected to support long-term market demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

Organic photovoltaics led the technology segment with 31.2% share, supported by lightweight structure, flexible design potential, and suitability for next-generation solar coating applications.

Building integrated photovoltaics accounted for 42.5% share by application, driven by rising use of solar materials in roofs, walls, windows, facades, and energy-efficient building surfaces.

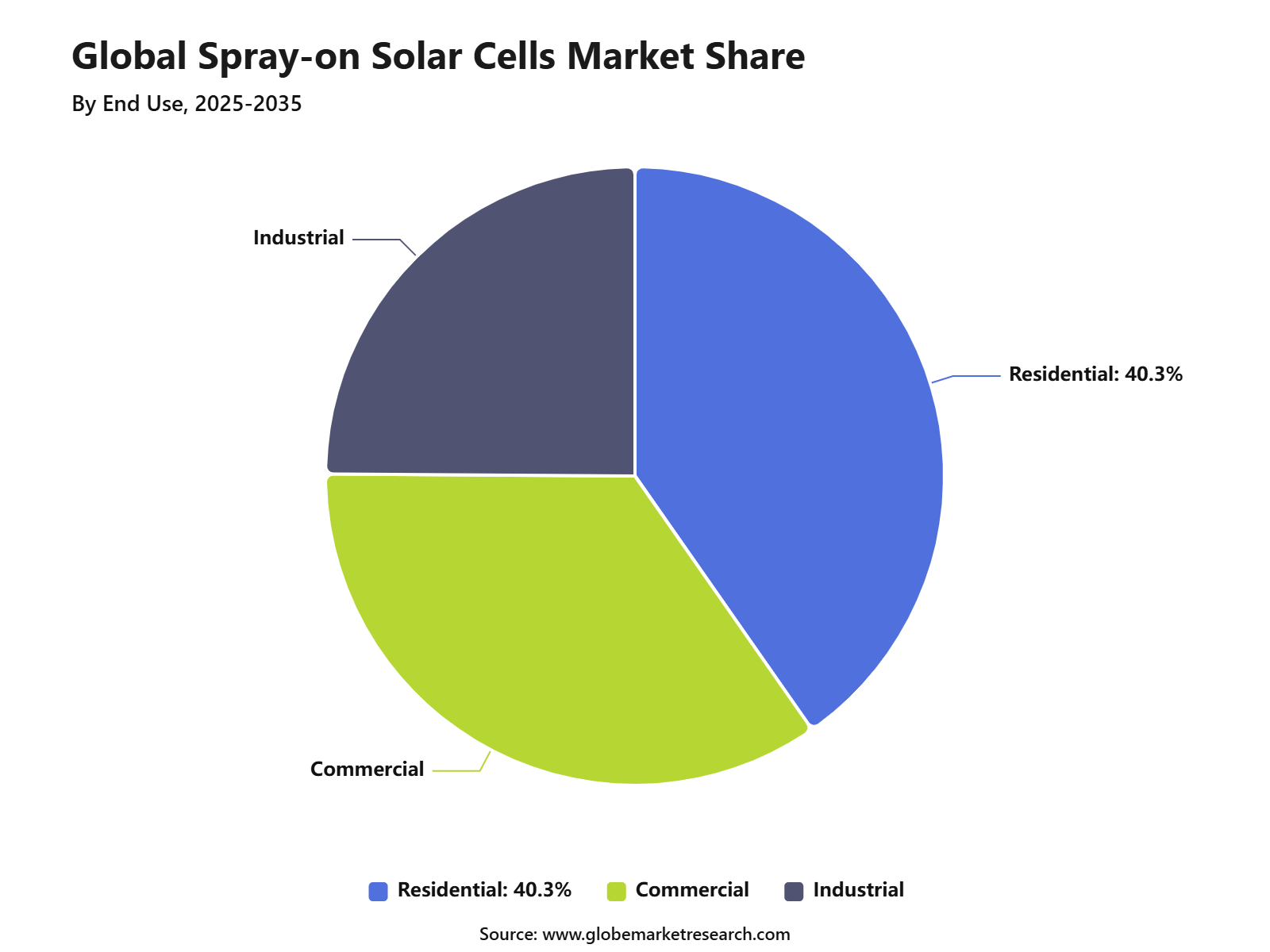

Residential installations held 40.3% share, supported by growing demand for lightweight, easy-to-apply solar solutions across homes, rooftops, and small building structures.

Flexible panels captured 41.3% share by form factor, driven by their use on curved surfaces, portable systems, building materials, and non-traditional solar installations.

North America led the spray-on solar cells market with 35.2% share, supported by strong clean energy adoption, advanced solar innovation, and rising investment in flexible and building-integrated solar technologies.

Top Funding and Investment

First Solar has spent over USD 2.0 billion on thin-film research and development, including work focused on perovskites. Its investment includes a new perovskite development line at Perrysburg, Ohio, producing small form-factor modules with a perovskite semiconductor. The company also expects total U.S. manufacturing and R&D infrastructure investment to reach about USD 4.5 billion from 2019 to 2026.

Sekisui Chemical committed ¥90 billion to build a 100 MW film-type perovskite solar cell production line at Sharp’s Sakai Plant in Osaka. The investment period runs from January 2025 to March 2027, with operation planned from April 2027. The project was also selected under Japan’s GX Supply Chain Construction Support Project, with total subsidies stated at ¥157.25 billion for a future 1 GW-level supply system.

Heliatek raised EUR 80.0 million to expand HeliaFilm organic solar film manufacturing capacity by 1.0 million square meters per year. The financing included EUR 42.0 million in equity, EUR 20.0 million in debt, and about EUR 18.0 million in subsidies. The investment supported roll-to-roll solar film capacity for building-integrated photovoltaics, construction materials, and automotive applications.

Tandem PV secured USD 50.0 million in Series A funding and debt in March 2025 to scale perovskite solar manufacturing in the U.S. The company stated that it had raised USD 83.0 million in venture capital, debt, and government funds at that stage. The funding is being used to advance high-efficiency perovskite solar panels and U.S.-based production capacity.

By Technology

Organic photovoltaics accounted for 31.2% share of the Spray-on Solar Cells Market. This leading position can be attributed to their lightweight structure, flexibility, low-temperature processing, and suitability for printable or spray-applied solar materials. The technology is gaining attention because organic photovoltaic layers can be applied on curved, flexible, and lightweight surfaces where conventional silicon panels may not be practical.

These features make them useful for building surfaces, portable devices, vehicles, and off-grid applications. Demand is expected to grow as research improves power conversion efficiency, durability, and material stability. Organic photovoltaics are likely to remain important in spray-on solar development because they support thin-film production and wider design flexibility.

By Application

Building integrated photovoltaics held 42.5% share of the Spray-on Solar Cells Market. This dominance is supported by rising interest in solar materials that can be applied directly to walls, roofs, windows, façades, and other building surfaces. Spray-on solar cells can help buildings generate electricity without depending only on traditional rooftop panels.

Their lightweight and flexible nature makes them suitable for modern architecture, renovation projects, and space-limited urban buildings. The segment is expected to remain strong as construction companies and property owners focus on energy-efficient buildings. Demand will be supported by green building standards, lower building emissions, and growing adoption of solar-integrated construction materials.

By End User

Residential applications accounted for 40.3% share of the Spray-on Solar Cells Market. This leading share is driven by rising household interest in clean energy, lower electricity bills, and flexible solar solutions that can be used on different home surfaces. Spray-on solar cells can support power generation on roofs, walls, windows, and small outdoor structures.

Their lightweight profile may offer advantages for homes where traditional solar panels are difficult to install due to structure, space, or design limitations. The residential segment is expected to gain further traction as homeowners seek affordable and easy-to-integrate renewable energy options. Product improvement, better durability, and wider installer acceptance will be important for long-term adoption.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Form Factor

Flexible panels held 41.3% share of the Spray-on Solar Cells Market. This segment leads because flexible solar formats can be used on curved, uneven, lightweight, and portable surfaces where rigid panels are less suitable. These panels are useful in building-integrated systems, vehicles, wearable devices, portable chargers, remote power units, and temporary energy setups.

Their design flexibility allows solar technology to move beyond fixed rooftop installations. Demand for flexible panels is expected to increase as industries focus on lightweight energy systems and new solar applications. Their ability to combine thin-film performance with easy installation supports their strong position in the market.

By Region

North America accounted for 35.2% share of the Spray-on Solar Cells Market, making it the leading regional market. Growth is supported by strong renewable energy investment, advanced solar research, building efficiency programs, and early adoption of next-generation photovoltaic technologies.

The United States is a major contributor due to strong clean energy policies, university-led materials research, solar technology startups, and demand for energy-efficient buildings. Canada also supports regional growth through building decarbonization and renewable energy initiatives.

North America is expected to maintain a strong position as spray-on and flexible solar technologies move closer to wider commercialization. Demand will be supported by residential solar adoption, building-integrated photovoltaics, and the need for lighter, more adaptable solar systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFGo-To-Market and Sales Economics

Spray-on solar cells are moving toward a specialist go-to-market route, mainly through perovskite, printable thin-film, flexible modules, and building-integrated solar surfaces. Commercial entry is expected to be strongest in rooftops, façades, vehicles, portable devices, and lightweight structures where rigid silicon panels are difficult to install. Solar demand is supportive, as global renewable capacity additions reached 800 GW in 2025, with solar PV providing over three-quarters of new renewable capacity.

Sales economics are shaped by coating speed, low material use, and the ability to print or deposit active layers on large surfaces. The U.S. Department of Energy notes that perovskite layers can be printed, coated, or vacuum-deposited on substrates, while efficiency improved from about 3% in 2009 to over 26% on small-area devices. This supports pilot-scale pricing models based on specialty applications first.

The near-term customer base is likely to include solar developers, BIPV suppliers, façade manufacturers, electronics firms, defense users, and off-grid energy providers. U.S. solar adoption also supports channel formation, as the country surpassed 6 million solar installations in 2026. Spray-on products must still prove durability before mass utility-scale acceptance, but distributed solar channels can support early commercial testing.

Risk Factors & Market Barriers

The main market barrier is not demand, but reliability. DOE identifies four commercial hurdles for perovskite solar technologies: stability and durability, power conversion efficiency at scale, manufacturability, and validation for bankability. This matters because spray-on cells must perform under heat, moisture, UV exposure, bending stress, and real outdoor conditions before project financiers accept them.

Scale-up risk is high because laboratory efficiency does not always transfer to large-area coated modules. DOE has stated that perovskite PV is not yet manufactured at scale, even though perovskite-silicon tandem cells have reached almost 34% efficiency. Uniform coating, encapsulation, quality control, and cell-to-module conversion losses remain major barriers for commercial production.

Price competition from conventional silicon is another barrier. Established solar supply chains already offer low-cost, bankable modules with warranties and large manufacturing capacity. In the U.S., domestic module manufacturing capacity reached 69.9 GW in 2026, enough to supply most national demand. Spray-on solar suppliers must therefore compete on weight, surface flexibility, aesthetics, and installation savings rather than price alone.

Revenue Potential Analysis

Revenue Landscape Across

Revenue opportunities are expected across building-integrated photovoltaics, flexible rooftops, portable solar, vehicle-integrated solar, agrivoltaics, sensors, and defense power systems. Buildings are especially important because spray-on or printed layers can turn walls, glass, and curved surfaces into energy-generating assets. Global solar generation increased by 636 TWh in 2025 to reach 2,778 TWh, confirming strong end-market demand for new PV formats.

The U.S. market shows a mixed but useful revenue signal. Solar installations reached 7.8 GWdc in Q1 2026, while residential installations were 1,179 MWdc and increased 6% year over year. This creates a route for lightweight, easy-install products where structural limits, design needs, or labor costs reduce the appeal of heavy conventional panels.

Commercial revenue can also emerge through licensing, coating equipment, specialty inks, encapsulation materials, and pilot manufacturing partnerships. DOE’s thin-film solar program awarded USD 44.0 million for research, development, and demonstration projects, while earlier perovskite funding focused on manufacturing R&D and validation. This shows that revenue may develop through both product sales and technology transfer.

Financial Impact

The financial impact of spray-on solar cells will depend on whether installation savings can offset lower bankability in early years. If coatings reduce weight, framing, mounting hardware, and labor, total installed cost can improve in complex locations. Solar PV generation is forecast by the IEA to rise by 320 to 360 TWh every year through 2030, supporting long-term revenue demand.

Higher efficiency could improve project economics when spray-on perovskites are used as tandem layers with silicon. Oxford PV stated in 2026 that its perovskite-based tandem technology delivers at least 20% more power than conventional modules, with theoretical efficiency potential up to 43%. Such gains can increase energy output per square meter, especially on space-limited rooftops and façades.

The strongest financial returns are expected from premium use cases rather than commodity solar farms. Early buyers are more likely to pay for lightweight design, flexible installation, low-load structures, and energy generation from unused surfaces. However, financing costs may stay higher until independent testing, long-term field data, and warranty standards prove product life close to established PV modules.

Drivers Impact Analysis

The Spray-on Solar Cells Market is driven by rising demand for lightweight, flexible, low-cost, and easy-to-install solar technologies. These cells can support building-integrated photovoltaics, curved surfaces, portable electronics, vehicles, rooftops, facades, and off-grid applications where rigid panels are difficult to use.

North America leads the market due to strong clean energy investment, advanced materials research, solar innovation, and demand for distributed renewable energy. The U.S. remains the key regional contributor because of its focus on next-generation photovoltaics, energy security, and building-level solar deployment.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for flexible solar solutions | +4.8% | North America, Europe, Asia Pacific | Drives core market growth. |

Growth in building-integrated photovoltaics | +4.0% | U.S., Canada, Europe, Japan | Supports urban solar use. |

Demand for lightweight renewable energy systems | +3.5% | Portable, transport, and off-grid markets | Expands application scope. |

Advancement in organic photovoltaic materials | +2.9% | North America, Europe, Asia Pacific | Improves technology readiness. |

Clean energy policy and investment support | +2.5% | U.S., Canada, Europe | Supports commercialization. |

Restraints Impact Analysis

The market faces restraints from lower commercial maturity, limited long-term durability, and efficiency gaps compared with conventional silicon solar panels. Many spray-on solar technologies are still moving from pilot-scale development toward reliable mass production.

Another restraint is customer confidence. Buyers in construction, utilities, and industrial markets need proven lifetime performance, warranty support, weather resistance, and bankable project economics before adopting newer solar formats at scale.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Lower efficiency than silicon panels | -2.4% | Global solar markets | Slows wider adoption. |

Limited long-term durability data | -2.0% | Building and outdoor applications | Affects buyer trust. |

High commercialization uncertainty | -1.7% | Emerging solar technology firms | Raises investment risk. |

Scaling production with consistent quality | -1.4% | North America, Europe, Asia Pacific | Limits supply readiness. |

Competition from mature PV panels | -1.2% | Global rooftop and utility markets | Restricts near-term share. |

Opportunities Impact Analysis

Opportunities are strong in building-integrated photovoltaics, flexible panels, residential rooftops, portable solar, automotive surfaces, consumer electronics, and off-grid energy systems. Spray-on solar cells can create value where thin, lightweight, and adaptable solar coatings are needed.

Higher-value opportunities are also emerging in organic photovoltaics, perovskite-based coatings, tandem structures, and printable solar technologies. Companies that improve efficiency, stability, and scalable coating methods can gain strong long-term advantage.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Building-integrated solar applications | +4.5% | North America, Europe, Japan | Builds premium demand. |

Flexible and curved surface deployment | +3.8% | Transport, consumer devices, rooftops | Expands use cases. |

Perovskite and organic PV development | +3.4% | U.S., Canada, Europe, Asia Pacific | Improves performance potential. |

Off-grid and portable power systems | +2.8% | Remote and emergency energy markets | Adds practical demand. |

Solar coatings for smart buildings | +2.3% | Urban construction markets | Creates new revenue streams. |

Challenges Impact Analysis

The main challenge is improving conversion efficiency while maintaining flexibility, coating uniformity, and low-cost production. Spray-on solar cells must deliver reliable performance across temperature, humidity, UV exposure, dust, and mechanical stress.

Another challenge is integrating the technology into real products and buildings. Developers must work with construction companies, glass makers, coating suppliers, electronics firms, and solar installers to create practical commercial systems.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Improving power conversion efficiency | -2.3% | Global R&D and manufacturing hubs | Affects competitiveness. |

Ensuring outdoor weather resistance | -1.9% | Rooftop and facade applications | Impacts service life. |

Achieving uniform coating quality | -1.6% | Spray and printing production lines | Raises manufacturing risk. |

Integrating with building materials | -1.3% | Construction and BIPV markets | Adds design complexity. |

Building installer and buyer confidence | -1.1% | Commercial and residential markets | Slows adoption. |

Segment Covered in the Report

By Technology

Organic Photovoltaics

Inorganic Photovoltaics

Perovskite Solar Cells

By Application

Portable Electronics

Transportation

By End Use

Residential

Commercial

Industrial

By Form Factor

Flexible Panels

Rigid Panels

Transparent Panels

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Regional Impact Analysis

North America leads the Spray-on Solar Cells Market with 35.2% share in 2025, supported by advanced solar R&D, clean energy investments, building-integrated photovoltaic interest, and demand for distributed power solutions. The U.S. remains the main regional driver due to strong research and early-stage commercialization activity.

Europe remains important because of green building standards, urban solar adoption, and strong decarbonization goals. Asia Pacific is expected to build future demand through electronics manufacturing, solar supply chains, smart city projects, and flexible PV development.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +5.0% | North America, 35.2% share in 2025 | Leads value demand. |

U.S. advanced solar innovation | +3.7% | U.S. | Drives regional development. |

Canada clean energy and building integration | +2.4% | Canada | Supports niche adoption. |

Europe green building demand | +2.2% | Germany, UK, France, Netherlands | Builds premium applications. |

Asia Pacific flexible PV manufacturing | +2.0% | China, Japan, South Korea, India | Supports future scale. |

Market Trend Analysis

The market trend is moving toward organic photovoltaics, perovskite solar coatings, building-integrated photovoltaics, residential flexible formats, and lightweight solar films. These technologies are gaining attention because they can expand solar adoption beyond traditional rigid panel surfaces.

Flexible panels and sprayable coatings are also becoming more relevant for urban buildings, portable devices, vehicles, and low-load rooftops. North America remains the value leader, while Europe and Asia Pacific support future growth through green building and solar manufacturing initiatives.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Organic photovoltaic adoption rises | +4.2% | North America, Europe, Asia Pacific | Supports flexible solar growth. |

Building-integrated photovoltaics expand | +3.7% | U.S., Canada, Europe, Japan | Drives premium applications. |

Flexible panel demand increases | +3.2% | Residential, transport, portable uses | Broadens market reach. |

Perovskite coating research advances | +2.8% | U.S., Europe, Japan, China | Improves future efficiency. |

Lightweight solar films gain traction | +2.2% | Off-grid and rooftop markets | Adds installation flexibility. |

Investor Type Impact Matrix

Investors should focus on companies with strong materials science capability, scalable coating processes, flexible PV expertise, and partnerships in construction, solar installation, electronics, and smart building systems. Technology validation and durability testing remain key investment factors.

Strategic investors can also target organic PV developers, perovskite coating companies, printable solar ink firms, encapsulation suppliers, and building-integrated solar solution providers. Companies that improve efficiency, lifetime, and production scale are better positioned for long-term growth.

Investor Type | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Spray-on Solar Technology Developers | +3.9% | Global | Expands next-generation PV supply. |

Organic and Perovskite PV Companies | +3.4% | North America, Europe, Asia Pacific | Drives technology progress. |

Building-Integrated Solar Firms | +2.9% | North America, Europe, Japan | Builds application demand. |

Advanced Coating and Materials Companies | +2.4% | Global manufacturing hubs | Improves product performance. |

Strategic and Clean Energy Investors | +2.0% | North America, Europe, Asia Pacific | Funds commercialization growth. |

Recent Developments

In March 2026, Swift Solar acquired core manufacturing assets and intellectual property from Meyer Burger. The deal included gigawatt-scale heterojunction manufacturing equipment and a global patent portfolio, supporting Swift Solar’s plan to scale perovskite-silicon tandem solar production in the U.S.

In June 2026, Oxford PV and Fraunhofer ISE combined Oxford PV’s perovskite-silicon cells with Fraunhofer’s Matrix Shingle technology. The large-area bifacial module reached 546 W and was prepared for display at Intersolar Europe 2026.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Market Concentration: Medium

Consolidated

The Spray-on Solar Cells Market shows medium concentration because only a limited number of companies and research-backed manufacturers have reached advanced pilot, demonstration, or pre-commercial production stages. Technical know-how is concentrated around perovskite chemistry, organic PV materials, roll-to-roll coating, encapsulation, and large-area process control. This gives early technology leaders an advantage in patents, manufacturing learning, and project partnerships.

At the same time, the market is not highly consolidated because commercial deployment is still developing. Many universities, start-ups, chemical suppliers, coating equipment providers, construction material firms, and solar manufacturers are still testing different materials and production routes. As a result, market leadership has not yet been fully locked in.

Market Structure

The market structure is innovation-led and project-based. Established solar companies are focused on improving efficiency and bankability, while specialist firms are working on flexible films, façade solar, transparent PV, organic PV, and perovskite modules. Construction and building-material partnerships are becoming important because spray-on solar cells need to be integrated into roofs, walls, windows, and lightweight structures rather than sold only as standalone panels.

Commercial growth will likely depend on three practical factors: proven outdoor durability, scalable roll-to-roll production, and clear installation economics. IEA expects renewable power capacity to increase by almost 4,600 GW between 2025 and 2030, with utility-scale and distributed solar PV representing nearly 80% of renewable electricity capacity expansion. This gives spray-on solar cells a large opportunity base, but adoption will depend on whether the technology can prove reliable performance at commercial scale.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

SolarPrint

Nanosolar

Heliatek

Oxford PV

Sunflare

Ubiquitous Energy

SolarWindow Technologies

PowerFilm Solar

Saule Technologies

Swift Solar

GreatCell Energy

First Solar

Tesla

Nanoco Technologies

Dyesol

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Energy and Power

Hydropower Generation Market to Hit USD 560.9 Billion by 2035

Hydropower Generation Market Size, Share, Analysis By Plant Type (Large Hydropower Plant, Small Hydropower Plant, Pumped Storage Hydropower), By Application (Utility, Industrial, Rural Electrification), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Power Generation Market to Hit USD 2,539.5 Billion by 2035

Power Generation Market Size, Share, Analysis By Type (Conventional/Non-Renewable (Nuclear and Fossil Fuels), Non-Conventional/Renewable (Solar, Wind, Hydro, and Others)), By End-User (Residential, Commercial, Industrial, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Single Phase String Inverters Market to Hit USD 5.1 Billion by 2035

Single Phase String Inverters Market Size, Share, Analysis By Connectivity (On-Grid, Off-Grid), By Power Rating (Below 1 kW, 1 kW to 3 kW, 3 kW to 5 kW, Above 5 kW), By Application (Residential, Commercial), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Hydrogen Fuel Cells Market to Hit USD 70.2 Billion by 2035

Hydrogen Fuel Cells Market Size, Share, Analysis By Type (Air-Cooled Type, Water-Cooled Type), By Application (Stationary, Transport, Portable), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035