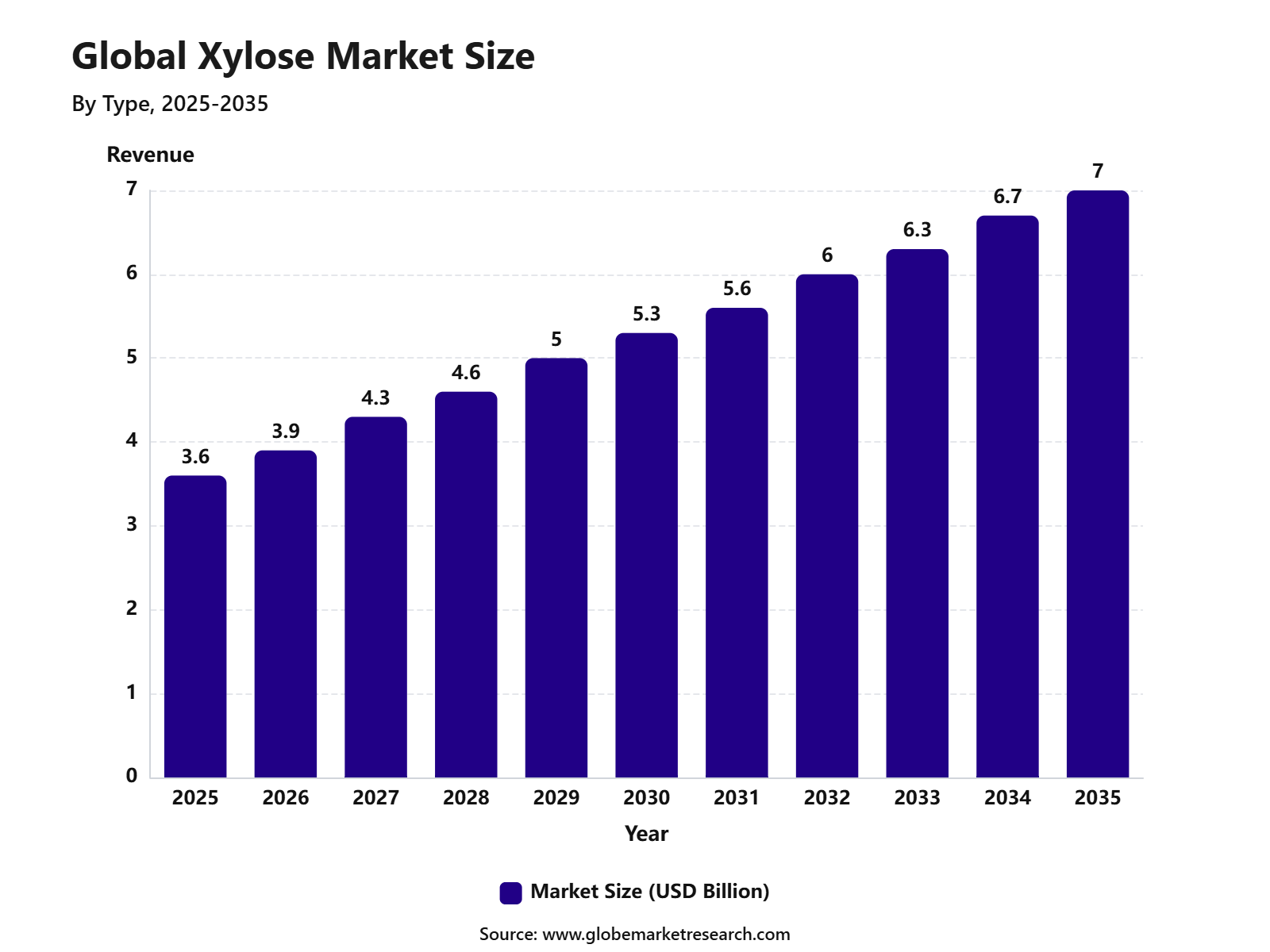

Revenue, 2025

$ 3.6 Bn

Forecast, 2035

$ 7.0 Bn

CAGR, 2025-2035

6.9%

Report Coverage

Global

Market Size and Forecast

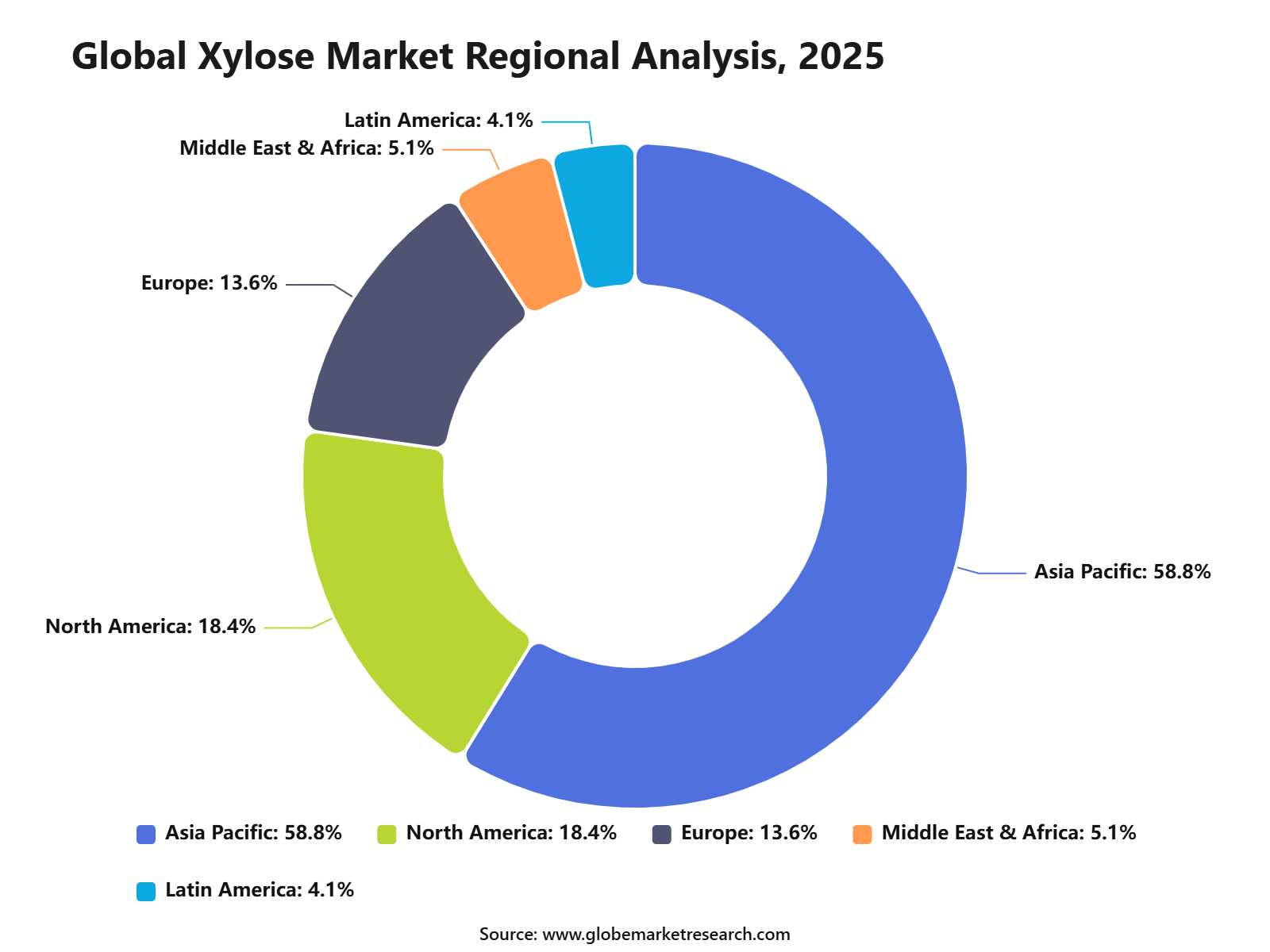

The Global Xylose Market was valued at USD 3.6 billion in 2025 and is projected to reach USD 7.0 billion by 2035, growing at a CAGR of 6.9% from 2025 to 2035. Asia Pacific held the largest regional share of 58.8% in 2025, supported by strong demand from food and beverage, pharmaceuticals, nutraceuticals, animal feed, and bio-based chemical applications.

Xylose is a naturally occurring sugar commonly derived from plant-based biomass such as wood, corn cobs, sugarcane bagasse, and other agricultural residues. The growth of the market can be attributed to rising demand for low-calorie sweeteners, increasing use of xylose in xylitol production, and growing preference for naturally sourced ingredients in food, oral care, and dietary supplement products.

The market outlook remains positive as manufacturers increase the use of xylose in sugar-free confectionery, functional foods, pharmaceutical formulations, and bio-based industrial products. Asia Pacific is expected to maintain its leading position due to abundant agricultural raw materials, expanding food processing capacity, strong xylitol production, and rising consumer demand for healthier sugar alternatives.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Market Insights

D-Xylose led the type segment with 56.6% share, supported by its wide use in food ingredients, pharmaceutical formulations, sweeteners, and specialty chemical applications.

Powder form accounted for 64.2% share, driven by easier handling, longer shelf life, better storage stability, and suitability for large-scale industrial use.

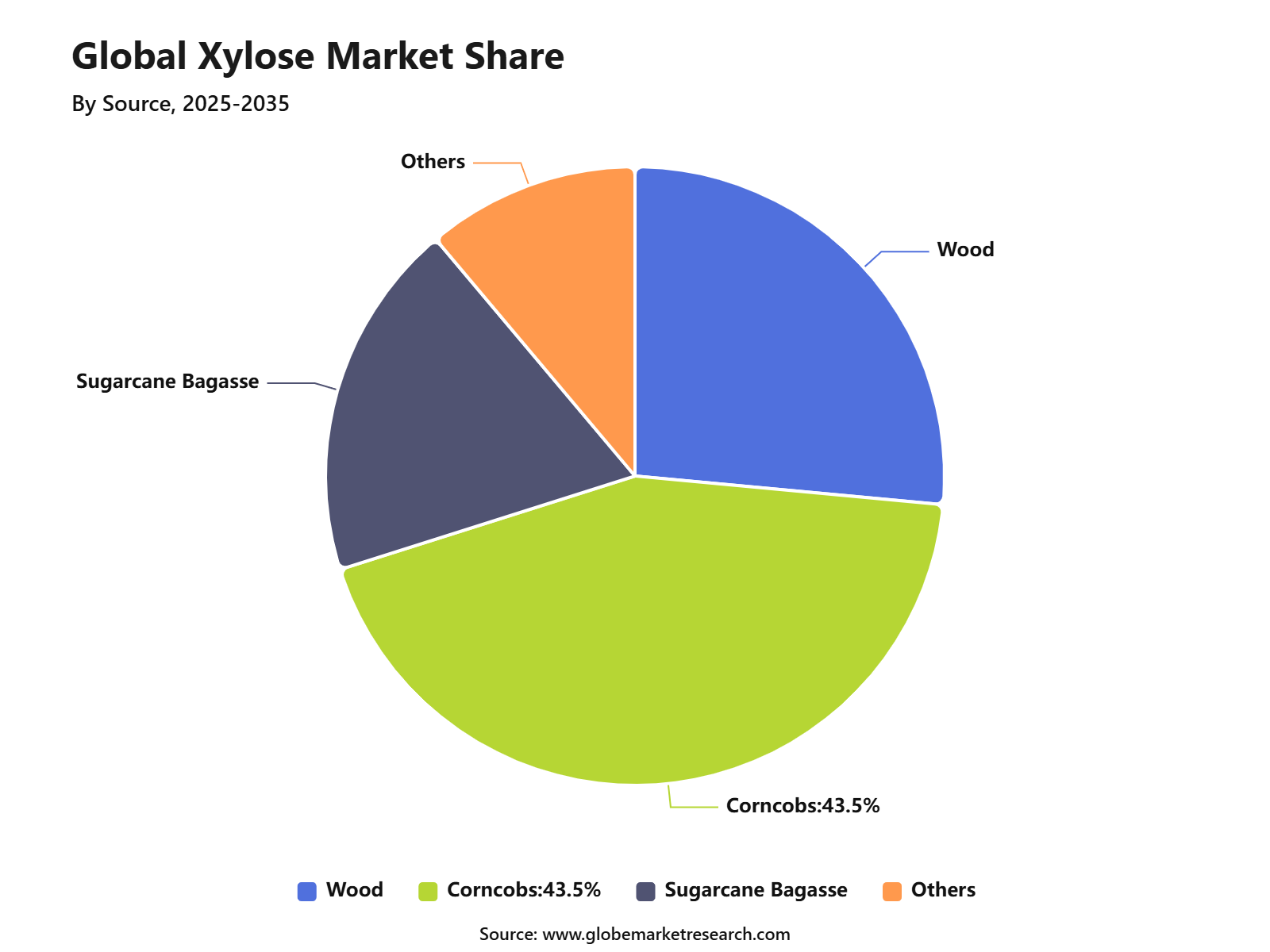

Corncobs held 43.5% share by source, supported by strong availability, cost-effective processing, and high xylose extraction potential from agricultural biomass.

Food and beverage captured 49.9% share by application, driven by demand for low-calorie sweeteners, flavoring ingredients, and functional food formulations.

Asia Pacific led the xylose market with 58.8% share, supported by strong agricultural raw material supply, expanding food processing activity, and rising demand for natural sweetener ingredients.

Go-to-Market Strategy

The Xylose Market needs an application-led go-to-market strategy because xylose is mainly sold as a functional ingredient and chemical intermediate rather than as a mass-market sweetener. Suppliers should target xylitol producers, food and beverage formulators, diabetic food manufacturers, oral care brands, pharmaceutical excipient users, nutraceutical companies, and bio-based chemical producers. U.S. Customs describes D-xylose as a chemically pure sugar extracted from wood or straw, used to produce xylitol and also used in foods for diabetics as a sweetening agent. This supports a sales model based on purity, particle size, moisture control, regulatory documentation, and consistent batch quality.

Sales economics are stronger when xylose is linked to higher-value downstream uses such as xylitol, specialty foods, oral care, fermentation, and bio-based chemicals. Corncobs, wood, straw, and sugarcane bagasse are important feedstock routes because they provide hemicellulose-rich material for xylose extraction. USDA data for 2025/2026 shows large corn production bases in the United States and China, with the United States at 432.34 million metric tons and China at 301.24 million metric tons, supporting the availability of agricultural residues such as corncobs and stalks.

Risk Factors & Market Barriers

The main risk factor is feedstock quality and processing efficiency. Xylose extraction depends on biomass quality, moisture, storage, pretreatment technology, acid or enzymatic hydrolysis, purification, and crystallization efficiency. If agricultural residues are contaminated, degraded, or inconsistent, the final xylose yield and quality can be affected. This creates quality-control pressure for suppliers that serve food-grade, pharmaceutical-grade, and high-purity xylitol production customers.

Another barrier is competition from cheaper sweeteners and other polyol intermediates. Xylose has strong value in xylitol production and specialty applications, but it competes indirectly with glucose, sorbitol, erythritol, maltitol, stevia, sucralose, and other sugar reduction systems in food and beverage formulations. OECD-FAO notes that sugarcane continues to drive more than 85% of total sugar crop production, showing that conventional sugar remains deeply established in global food systems. This means xylose suppliers need to compete on function, low glycemic positioning, dental health linkage through xylitol, and clean-label value rather than only sweetness cost.

Revenue Potential Analysis

Revenue Landscape Across

The revenue landscape for xylose is spread across xylitol production, diabetic foods, low-sugar formulations, oral care, nutraceuticals, pharmaceuticals, fermentation media, bio-based chemicals, and research-grade carbohydrates. Xylitol production remains one of the most important downstream routes because xylose is hydrogenated into xylitol, which is widely used in sugar-free chewing gum, oral care, confectionery, and special dietary products. The European Commission’s food and feed portal lists an authorized health claim that chewing gum sweetened with 100% xylitol has been shown to reduce dental plaque, supporting oral care and functional confectionery demand.

Bio-based chemicals provide another revenue route because xylose can be used in fermentation and biomass conversion pathways. Agricultural residues such as straw, wood residues, corncobs, and sugarcane bagasse can support circular production models when collection, pretreatment, and purification are economically viable. OECD-FAO expects global sugar production to expand, with sugarcane remaining a major crop base, which supports long-term availability of bagasse and other biomass streams for biorefinery use.

Financial Impact

The financial impact can be positive for producers that control feedstock sourcing, improve extraction yield, and supply consistent high-purity grades. Better margins can be achieved through food-grade xylose, pharmaceutical-grade xylose, xylitol feedstock contracts, and customer-specific specifications. Producers located near biomass sources may benefit from lower raw material logistics costs, especially when corncobs, straw, and bagasse are available from nearby agricultural processing.

Financial risk remains linked to purification cost, energy use, waste treatment, freight, tariffs, and competition from lower-cost sweetener systems. The 5.8% U.S. duty classification for D-xylose can affect import economics, while quality failures can raise rejection costs for food and pharmaceutical customers. Stronger financial resilience is expected from suppliers with stable biomass procurement, validated manufacturing processes, documented regulatory compliance, and long-term contracts with xylitol and specialty ingredient buyers.

Type Analysis

D-Xylose led the Xylose Market with 56.6% share, supported by its strong use as a raw material for xylitol, food ingredients, pharmaceuticals, animal nutrition, and bio-based chemicals. It is widely preferred because it can be derived from plant biomass and used in multiple industrial and food-related applications.

The growth of this segment can be attributed to rising demand for low-calorie sweeteners, sugar alternatives, and bio-based ingredients. D-Xylose is especially important in xylitol production, where it acts as the main intermediate for producing a sweetener used in food, oral care, and wellness-related products.

Form Analysis

Powder held 64.2% share of the Xylose Market, making it the leading form segment. Powdered xylose is preferred because it is easier to store, transport, measure, blend, and use in food processing, pharmaceutical formulations, laboratory applications, and industrial production.

The segment is supported by its longer shelf life, handling convenience, and compatibility with dry ingredient systems. Manufacturers prefer powdered xylose because it can be used efficiently in sweetener production, nutraceuticals, bakery formulations, oral care products, and specialty chemical processes.

Source Analysis

Corncobs accounted for 43.5% share, supported by their strong availability as an agricultural residue and their high hemicellulose content. Corncobs are widely used as a biomass source for xylose extraction because they can be converted through hydrolysis into xylose-rich streams for further processing.

The growth of this segment is linked to rising interest in agricultural waste valorization and bio-based production. Corncob-based xylose supports circular use of crop residues and provides a practical feedstock for producing xylitol, ethanol, and other value-added bio-products.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFApplication Analysis

Food and beverage led the application segment with 49.9% share, driven by the use of xylose in sweetener production, functional food ingredients, flavor development, and health-focused formulations. Xylose is closely linked with xylitol, which is widely used as a sugar substitute in chewing gum, confectionery, beverages, oral care products, and diabetic-friendly food products.

The segment is supported by rising consumer demand for reduced-sugar, low-calorie, and natural-origin ingredients. Food and beverage manufacturers are increasingly using xylose-derived ingredients to support clean-label positioning, better sweetness profiles, and product reformulation for health-conscious consumers.

Regional Analysis

Asia Pacific led the Xylose Market with 58.8% share, supported by strong agricultural biomass availability, growing food processing activity, and large-scale demand for xylitol and sugar-reduction ingredients. China, India, Japan, South Korea, and Southeast Asian countries remain important contributors due to their strong food manufacturing base and expanding bio-based chemical production.

The region’s dominance can be attributed to the availability of corncobs and other lignocellulosic feedstocks, along with increasing demand from food, beverage, pharmaceutical, and personal care applications. Asia Pacific is expected to remain the leading market as manufacturers continue to invest in biomass-based xylose production and value-added sweetener applications.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific market leadership | +2.2% | Asia Pacific, 58.8% share in 2025 | Leads production and demand. |

China feedstock and manufacturing strength | +1.7% | China | Supports large-scale supply. |

North America health ingredient demand | +1.1% | U.S. and Canada | Supports specialty applications. |

Europe clean-label sweetener growth | +1.0% | Germany, UK, France, Italy | Drives premium usage. |

Latin America and MEA emerging adoption | +0.6% | Brazil, Mexico, GCC, South Africa | Builds gradual demand. |

Market Trend Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth of D-xylose usage | +1.6% | Asia Pacific, Europe, North America | Leads product demand. |

Powder-form xylose preference | +1.3% | Global | Supports easy formulation. |

Corncob-based xylose production | +1.2% | China, India, Southeast Asia | Improves raw material supply. |

Clean-label sweetener adoption | +1.0% | Europe, North America, urban Asia | Supports healthier positioning. |

Food and beverage formulation growth | +0.9% | Global | Expands commercial usage. |

Investment Opportunity Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Corncob-based xylose production | +1.5% | Asia Pacific | Offers supply advantage. |

Food-grade xylose manufacturing | +1.3% | Global | Builds high-volume demand. |

Xylitol value-chain integration | +1.2% | China, India, Europe | Improves margin potential. |

Bio-based ingredient platforms | +1.0% | Europe, North America, Asia Pacific | Supports clean-label demand. |

Export-focused refining facilities | +0.8% | Asia Pacific | Strengthens global supply. |

Segment covered in the Report

By Type

D-Xylose

L-Xylose

DL-Xylose

By Form

Powder

Liquid

Granules

By Source

Wood

Corncobs

Sugarcane Bagasse

Others

By Application

Food and Beverage

Cosmetics and Personal Care

Animal Feed

Pharmaceuticals

Biofuel Industry

Others

By Region

Asia Pacific

North America

Europe

Middle East & Africa

Latin America

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for low-calorie sweeteners | +1.8% | Asia Pacific, North America, Europe | Drives food applications. |

Growth in xylitol production | +1.5% | China, India, Japan, South Korea | Supports xylose consumption. |

Increasing use in food and beverages | +1.3% | Global | Expands ingredient demand. |

Growing health-conscious consumer base | +1.1% | Asia Pacific, Europe, North America | Supports sugar alternatives. |

Wider use of corncob-based raw materials | +0.9% | Asia Pacific | Improves feedstock availability. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Raw material price fluctuation | -0.9% | Asia Pacific, global buyers | Pressures production cost. |

Complex extraction and purification process | -0.8% | Global producers | Raises manufacturing cost. |

Competition from other sweeteners | -0.7% | Food and beverage markets | Limits faster adoption. |

Limited awareness in some regions | -0.6% | Latin America, MEA | Slows market penetration. |

Quality consistency challenges | -0.5% | Export markets | Affects buyer confidence. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion of sugar-free food products | +1.7% | Asia Pacific, Europe, North America | Supports ingredient growth. |

Growth in oral care applications | +1.4% | Global | Expands xylitol demand. |

Rising demand for bio-based ingredients | +1.2% | Europe, North America, Asia Pacific | Improves sustainability appeal. |

Increasing use in nutraceuticals | +1.0% | Developed and urban markets | Opens premium demand. |

New applications in fermentation and chemicals | +0.8% | Asia Pacific, Europe | Broadens industrial use. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining cost-efficient production | -0.8% | Global | Affects price competitiveness. |

Dependence on agricultural feedstock | -0.7% | Asia Pacific | Creates supply risk. |

Regulatory compliance for food-grade use | -0.6% | U.S., Europe, Asia Pacific | Raises approval burden. |

Supply chain concentration risk | -0.5% | Asia Pacific-led supply | Impacts global availability. |

Consumer confusion with other sweeteners | -0.4% | Global | Slows product positioning. |

Recent Developments

In January 2026, USDA ARS advanced corn fiber-based xylose recovery research. The USDA Agricultural Research Service published a peer-reviewed study on January 21, 2026, showing that recovered whole and degermed corn kernel fibers, after sodium carbonate pretreatment, achieved over 70% total sugar conversion during enzymatic hydrolysis. The study also found that corn mixtures with 10% and 20% solids generated additional xylose and arabinose while maintaining consistent ethanol yield, supporting wider use of corn biorefinery residues as xylose-rich feedstock.

In February 2026, the European Commission updated its food enzyme register involving xylose isomerase. The updated register includes D-xylose aldose-ketose-isomerase, also listed as xylose isomerase, with entries from Streptomyces murinus and Streptomyces rubiginosus. This is important for the xylose value chain because xylose isomerase is used in sugar conversion processes, although the Commission clearly states that the register is not a final EU authorisation list.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 3.6 Billion |

Forecast Revenue (2035) | USD 7.0 Billion |

CAGR (2025-2035) | 6.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Type (D-Xylose, L-Xylose, DL-Xylose), By Form (Powder, Liquid, Granules), By Source (Wood, Corncobs, Sugarcane Bagasse, Others), By Application (Food and Beverage, Cosmetics and Personal Care, Animal Feed, Pharmaceuticals, Biofuel Industry, Others) |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | International Flavors & Fragrances Inc., Zhejiang Huakang Pharmaceutical Co., Ltd., Shandong Longlive Bio-Technology Co., Ltd., Futaste Co., Ltd., Anyang City Yuxin Xylitol Technology Co., Ltd., Danisco, Shandong Xieli Bio-Technology Co., Ltd., Toyota Tsusho Corporation, Xylitol Canada Inc., Healtang Biotech Co., Ltd. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

International Flavors & Fragrances Inc.

Zhejiang Huakang Pharmaceutical Co., Ltd.

Shandong Longlive Bio-Technology Co., Ltd.

Futaste Co., Ltd.

Anyang City Yuxin Xylitol Technology Co., Ltd.

Danisco

Shandong Xieli Bio-Technology Co., Ltd.

Toyota Tsusho Corporation

Xylitol Canada Inc.

Healtang Biotech Co., Ltd.

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Chemical and Material

Oxygen Market to Exceed USD 171.1 Billion by 2035

Global Oxygen Market Size, Share Analysis By Form (Gas, Liquid, Solid), By Type (Industrial, Medical), By Application (Metals and Mining, Chemical Industry, Oil and Gas, Healthcare, Pharmaceutical, Other Applications), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Tannin Market to Hit USD 9.8 Billion by 2035

Global Tannin Market Size, Share and Go-to-Market Strategy Analysis By Source (Plant, Brown Algae), By Product Type (Hydrolysable Tannins, Condensed Tannins, Phlorotannins, Others), By Application (Food and Beverage, Pharmaceutical and Nutraceutical, Leather Industry, Wood Industry, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Printing Ink Market to Hit USD 30.6 Billion by 2035

Global Printing Ink Market Size, Go-to-Market Strategy Analysis By Type (Solvent-Based, Water-Based, Oil-Based, UV, UV-LED, Others), By Process (Lithographic Printing, Flexographic Printing, Gravure Printing, Digital Printing, Others), By Application (Packaging, Commercial and Publication, Textiles, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

Methanol Market to Exceed USD 64.1 Billion by 2035

Global Methanol Market Size By Feedstock (Natural Gas, Coal, Biomass and Renewables), By Derivative (Formaldehyde, Acetic Acid, MTBE, DME, Gasoline Blending, Biodiesel, MTO/MTP, Solvent, Others), By Sub-derivatives (Gasoline additives, Olefins, UF/PF resins, VAM, Polyacetals, MDI, PTA, Acetate Esters, Acetic anhydride, Fuels, Others), By Application (Construction, Automotive, Electronics, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035