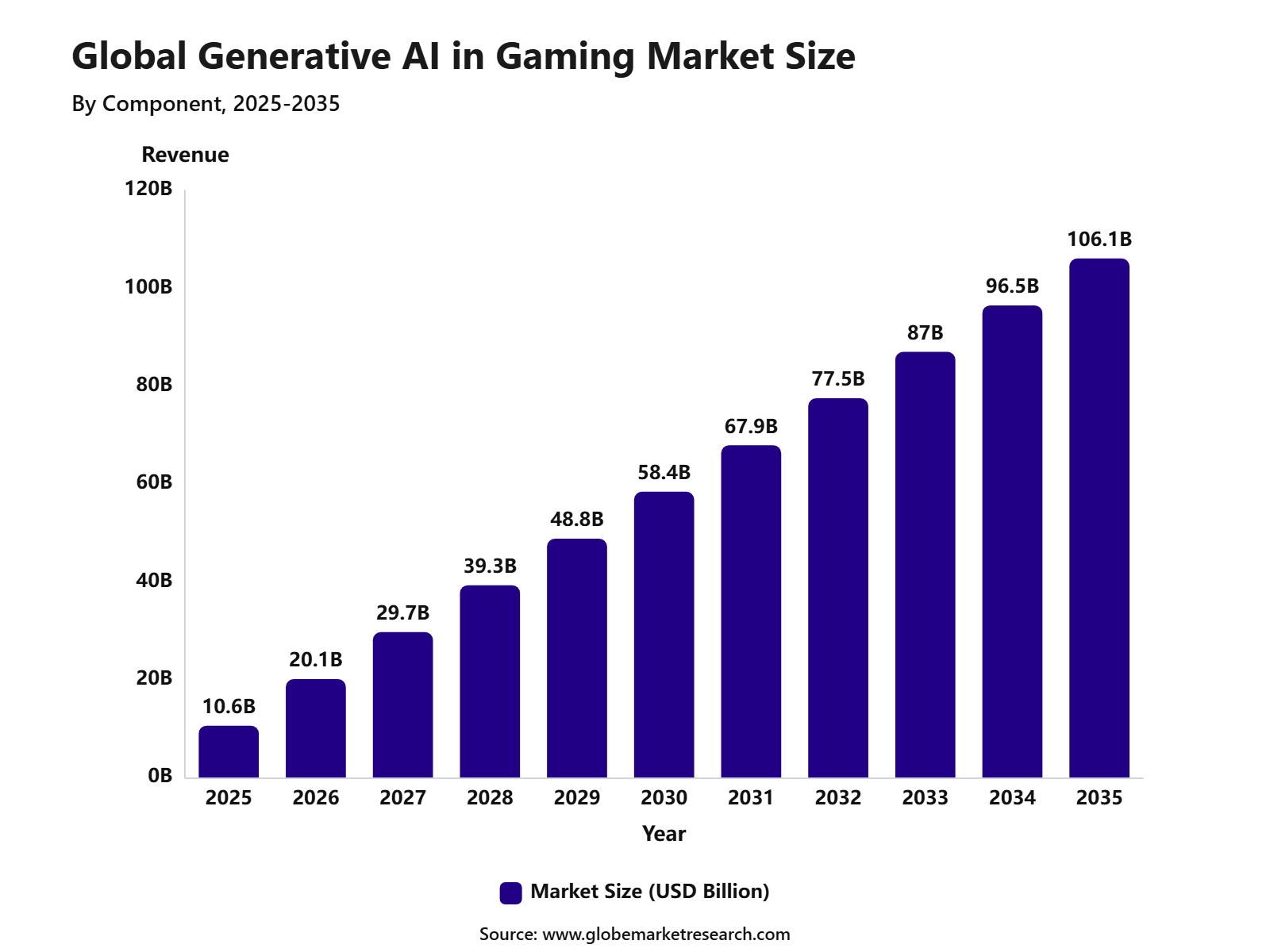

Revenue, 2025

$10.6 billion

Forecast, 2035

$106.1 billion

CAGR, 2025-2035

25.9%

Report Coverage

Global

Market Size and Forecast

The Generative AI in Gaming Market reached USD 10.6 billion in 2025 and is expected to grow to USD 106.1 billion by 2035, registering a CAGR of 25.9% . North America accounted for 41% share in 2025. The market growth is supported by the rising use of AI for game asset creation, character design, story and dialogue generation, procedural content development, and player experience personalization, as gaming studios focus on reducing development time, improving content quality, and creating more immersive gameplay experiences.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 10.6 Billion |

Projected Revenue, 2035 | USD 106.1 Billion |

CAGR, 2025-2035 | 25.9% |

Largest Region | North America, 41.0% Share |

U.S. Market Revenue, 2025 | USD 3.5 Billion |

U.S. CAGR | 25.9% |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

The U.S. Generative AI in Gaming Market was valued at approximately USD 3.5 billion in 2025 and is projected to expand at a CAGR of 25.9% from 2025 to 2035 , driven by rising adoption of AI-based game asset creation, procedural content generation, character design, dialogue generation, game testing, and player experience personalization. The growth of the market can be attributed to the strong presence of gaming studios, advanced cloud infrastructure, high levels of AI investment, and the increasing use of generative tools to reduce development time, improve creative output, and support immersive gaming experiences.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Insights

Software led the component segment with 67.4% share. Demand was supported by rising use of AI tools for asset creation, animation support, dialogue generation, level design, and faster game development workflows.

Machine learning accounted for 34.8% share by technology. The segment remained important as developers used ML models to improve player behavior analysis, content personalization, non-player character intelligence, and automated testing.

Game assets held 31.6% share by content type. Growth was driven by wider use of generative tools for creating textures, environments, characters, sound effects, and visual elements with shorter production timelines.

Action games captured 28.9% share by game type. The need for dynamic environments, adaptive gameplay, realistic character movement, and faster generation of missions, maps, and combat scenarios supported adoption.

Mobile games led the platform segment with 39.7% share. The segment benefited from high mobile gaming usage, frequent content updates, lower entry barriers for casual players, and rising demand for personalized in-game experiences.

Procedural content generation accounted for 35.2% share by application. Demand increased as studios used generative AI to create levels, quests, maps, scenes, and game variations with improved speed and lower manual effort.

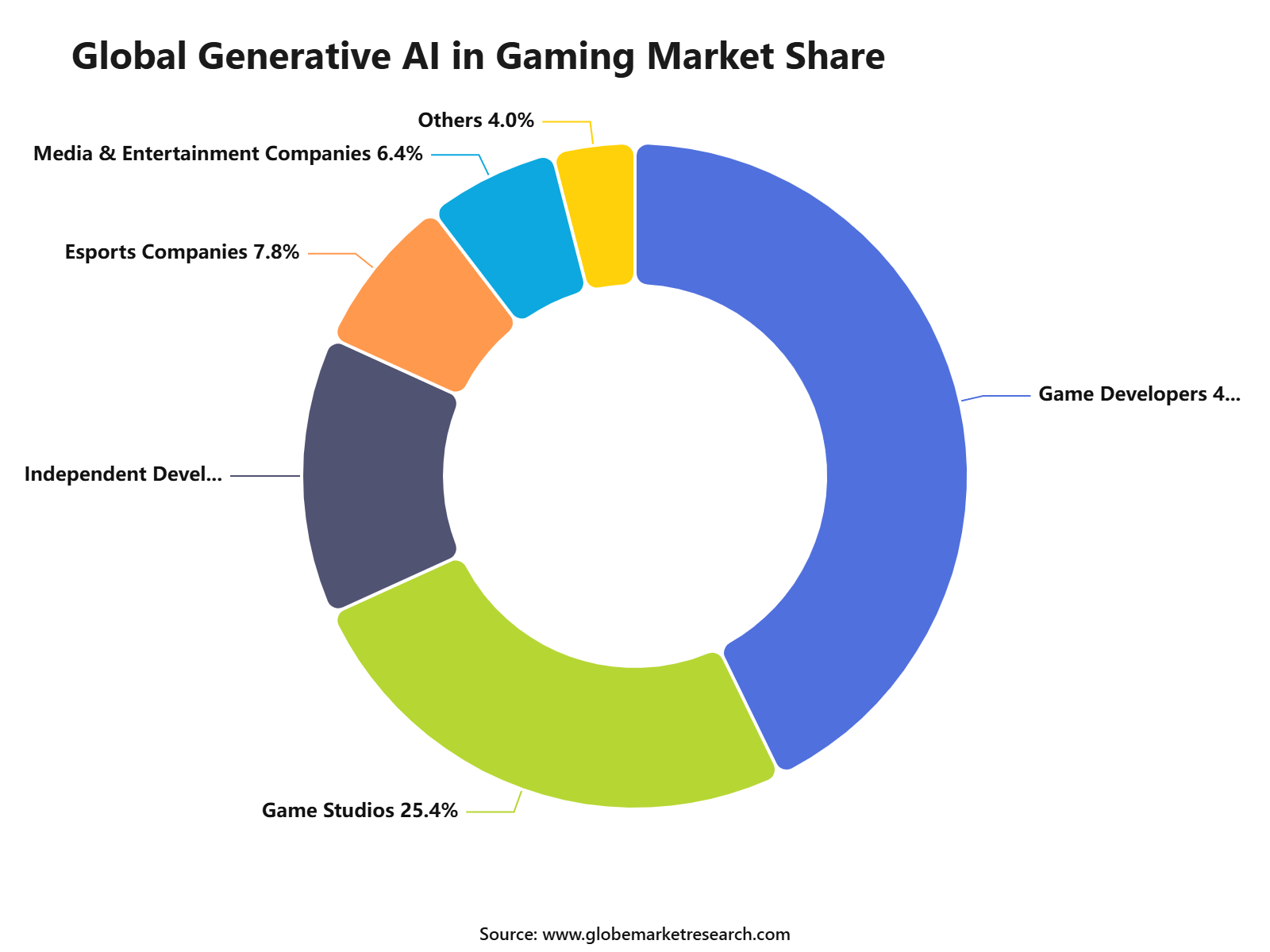

Game developers held 42.8% share by end user. Strong adoption was supported by the need to reduce development time, improve creative output, optimize production costs, and support faster release cycles.

Market Overview

The generative AI in the gaming market refers to the use of artificial intelligence techniques that can autonomously generate game content, narrative elements, character assets, dialogue, environments, and adaptive gameplay components. In contrast to traditional AI that follows scripted responses, generative AI creates new game assets or experiences dynamically, enabling more personalized and immersive interactions for players. These technologies are being adopted by developers to enhance design workflows, streamline production, and provide richer gaming experiences.

Generative AI adoption in gaming relies on technologies such as large language models (LLMs) for narrative and dialogue generation, neural networks for adaptive environment creation, and procedural generation engines for real‑time content variation. These technologies can reduce development time by up to 40% in some workflows, allowing studios to focus more on creative design while AI assists with routine content tasks.

Key driver is improved workflow efficiency for developers, as generative AI tools can automate parts of asset creation and scripting that would normally require extensive manual effort. Surveys from industry reports indicate that over one‑third of game industry professionals (about 36%) reported using generative AI tools as part of their development work, demonstrating growing professional integration of these technologies.

Customer Acquisition Strategy

The generative AI in the gaming market is driven by demand for faster game development, lower content production costs, better player engagement, and more personalized gaming experiences. Game studios are using generative AI for concept art, character design, dialogue support, level ideas, code assistance, testing support, localization, marketing content, and player support. In 2026, 36% of game industry professionals reported using generative AI tools at work, showing that adoption is moving from testing into daily workflows.

Sales economics are supported by the large gaming revenue base. U.S. consumer spending on video games reached USD 60.7 billion in 2025, showing strong demand for games, in-game content, subscriptions, hardware, and digital services. This creates a large commercial base for AI tools that can reduce production time, improve content output, and support live operations.

Tariff Impact

Gaming hardware is one of the most exposed areas. ESA stated that proposed tariffs could increase console prices by at least 40% , which may reduce consumer access to gaming devices and weaken software sales. Higher console, PC, and accessory prices can also slow player spending on games, subscriptions, in-game purchases, and premium content.

Semiconductor tariffs can also affect AI game development economics. U.S. Section 301 actions increased certain semiconductor tariffs to 50% in 2025, which can raise cost pressure across chips, servers, graphics hardware, and AI infrastructure. For generative AI gaming vendors, this may increase cloud computing charges, GPU rental costs, and private AI deployment costs for studios.

Revenue Potential Analysis

Revenue Opportunities

Revenue opportunities are strongest across game development tools, AI-assisted art workflows, code support, procedural content generation, NPC dialogue systems, localization, testing automation, and marketing content. In 2026, 36% of game industry professionals reported using generative AI at work. The most common use cases were research and brainstorming at 81% , code assistance at 47% , and prototyping at 35% , showing that AI is being used mainly to speed up production rather than fully replace creative teams.

Financial Impact

Financial impact is expected to be strongest where AI reduces production time and improves content output. AI tools can lower early-stage concept costs, speed up prototyping, reduce repetitive coding tasks, support localization, and improve customer support workflows. For large studios, the value is linked to scale and productivity. For independent developers, the value is linked to faster development and lower entry barriers.

However, revenue potential depends on trust, rights protection, and quality control. In 2026, 52% of game industry professionals said generative AI is hurting the industry. This shows that buyers may avoid tools that create copyright risk, low-quality assets, unclear ownership, or workforce concerns. Vendors with licensed training data, clear commercial rights, privacy controls, human review features, and game engine integration are expected to capture stronger demand.

Component Analysis

Software led the Generative AI in Gaming Market with 67.4% share, supported by the rising use of AI tools for game design, coding support, asset generation, testing, animation, dialogue creation, and live operations. Software platforms are becoming the core layer that allows studios to apply generative AI across different stages of game development. The segment is gaining strong demand because studios need faster production workflows and better creative support without increasing development complexity.

AI-based software can help teams create early concepts, test design options, generate code snippets, improve localization, and support content updates after launch. Software is expected to remain the leading component as game developers move toward tool-based AI adoption rather than full automation. Solutions that improve productivity while keeping artists, designers, writers, and developers in control are likely to gain stronger acceptance.

Technology Analysis

Machine learning accounted for 34.8% share, making it the leading technology segment in the Generative AI in Gaming Market. Machine learning supports core functions such as player behavior analysis, procedural content generation, NPC behavior, game balancing, recommendation systems, personalization, and automated testing. The growth of this segment can be attributed to the large volume of gameplay data generated across mobile, PC, and console platforms.

Developers are using machine learning to understand player patterns, predict churn, improve difficulty levels, and create more responsive game experiences. Machine learning is expected to remain important because it supports both creative and operational use cases. Its use will continue to grow in adaptive gameplay, automated quality assurance, content personalization, monetization analysis, and real-time player engagement systems.

Content Type Analysis

Game assets held 31.6% share, supported by rising demand for faster creation of characters, environments, textures, objects, concept art, sound elements, animations, and visual references. Generative AI is being used to support early-stage asset ideation and reduce repetitive design tasks. The segment is growing because modern games require large volumes of visual and audio content across multiple platforms and formats.

AI-assisted asset tools can help teams speed up prototyping, create variations, and support smaller studios with limited creative resources. Game asset generation is expected to remain a major use case, but quality control will remain important. Studios are likely to prefer AI tools that support originality, copyright safety, style consistency, human review, and smooth integration with existing game engines.

Game Type Analysis

Action games accounted for 28.9% share, supported by strong demand for fast gameplay, rich environments, interactive characters, dynamic missions, and frequent content updates. These games often require large asset libraries, responsive mechanics, and continuous balancing, which makes AI tools useful in development and testing. The growth of this segment is linked to the need for engaging worlds, smooth combat systems, realistic character movement, and personalized player experiences.

Generative AI can support concept development, enemy behavior design, level variation, animation support, and gameplay testing. Action games are expected to remain a key adoption area because they depend heavily on visual quality, replay value, and player engagement. AI tools that improve development speed while preserving gameplay quality and creative direction are likely to see higher use in this segment.

Platform Analysis

Mobile games led the platform segment with 39.7% share, supported by large smartphone access, wide app store distribution, and strong demand for casual, social, and live-service gaming. Mobile games are well-suited for AI-supported personalization because they generate frequent user interaction data. The segment is expanding as developers use AI to improve player onboarding, in-game offers, content recommendations, difficulty tuning, and live event planning.

Generative AI can also support faster creation of characters, story elements, ad creatives, and seasonal game content for mobile audiences. Mobile games are expected to remain a leading platform because they offer a large reach and faster content cycles. Developers who use AI responsibly to improve retention, personalization, and content updates are likely to benefit from stronger engagement.

Application Analysis

Procedural content generation held 35.2% share, driven by the need to create levels, maps, missions, environments, quests, items, and gameplay variations at scale. This application helps developers produce larger and more replayable game worlds with less manual effort. The segment is gaining traction because players increasingly expect fresh content, open-world depth, and personalized experiences.

AI-supported procedural systems can help generate varied gameplay paths, adaptive challenges, and dynamic in-game environments. Procedural content generation is expected to remain one of the strongest applications for generative AI in gaming. However, human review remains essential to ensure quality, story fit, technical stability, and a consistent player experience.

End User Analysis

Game developers accounted for 42.8% share, supported by their direct use of generative AI tools across design, development, testing, localization, and content production. Developers are using AI to reduce repetitive tasks, speed up prototyping, support coding workflows, and improve creative exploration. The segment is growing because studios face rising production costs, longer development cycles, and increasing demand for frequent content updates.

AI tools can help teams improve speed and efficiency, especially in early-stage design, quality testing, documentation, and asset variation. Game developers are expected to remain the leading end-user group, but adoption will depend on trust, transparency, and workflow fit. Tools that protect intellectual property, support human creativity, and provide clear control over outputs are likely to see stronger long-term demand.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Analysis

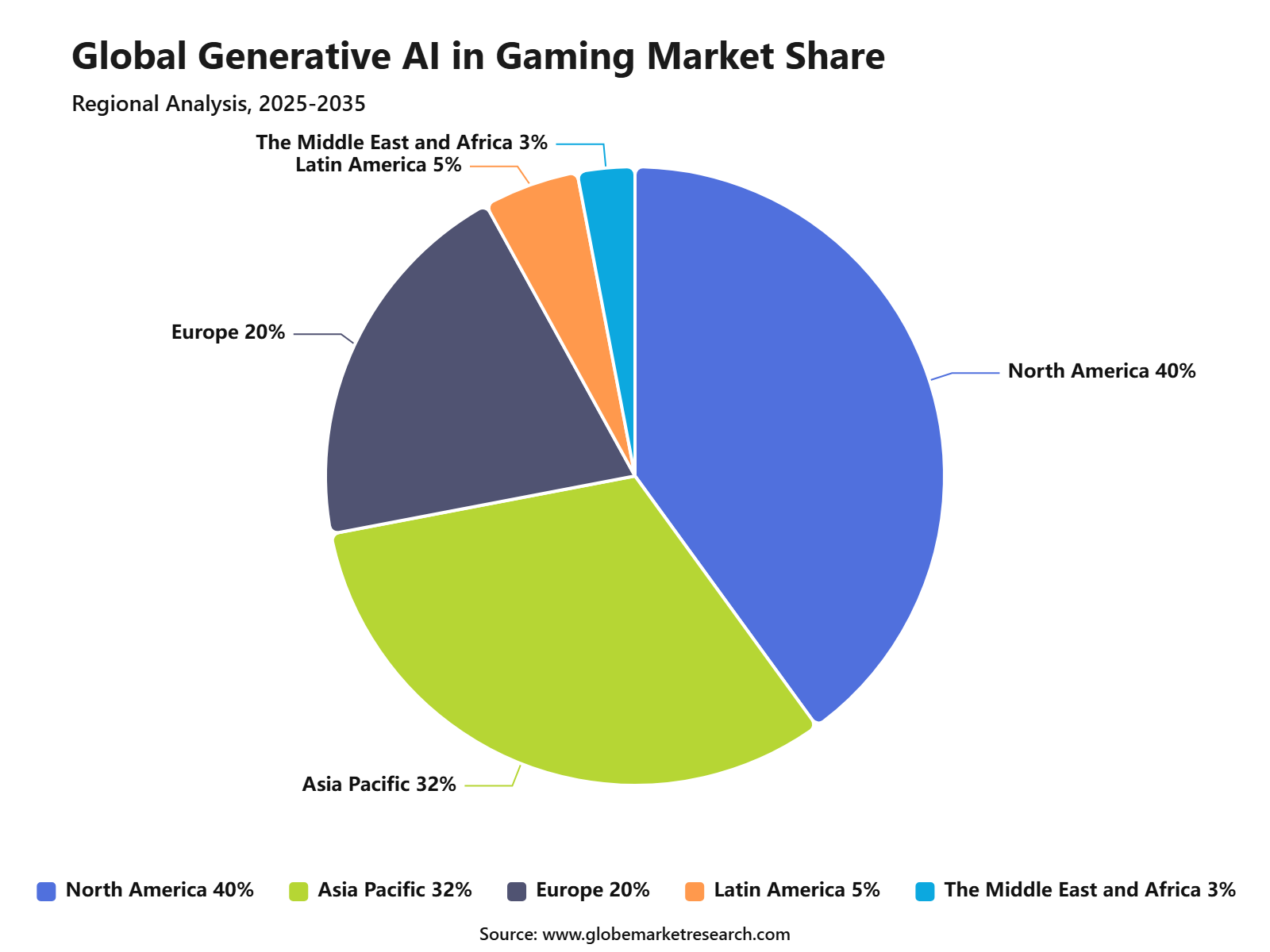

North America held the leading position in the Generative AI in Gaming Market, supported by strong game development studios, cloud computing infrastructure, AI model developers, and early adoption of AI-assisted production tools. Based on a global market value of USD 2.21 billion in 2026, North America is estimated to account for around 40% share, equal to nearly USD 0.88 billion. The region’s growth is supported by the United States, where major gaming, cloud, AI, and content creation companies are actively using generative AI for game assets, dialogue, testing, animation, and player personalization.

Asia Pacific accounted for an estimated 32% share, equal to nearly USD 0.71 billion in 2026, driven by the large gaming population in China, Japan, South Korea, India, and Southeast Asia. The region has a strong mobile gaming base, and Asia Pacific gaming revenue reached about USD 155.8 billion in 2024, showing the scale of the gaming ecosystem available for AI-driven tools. Generative AI adoption is rising across mobile games, anime-style content, real-time translation, NPC behavior, and low-cost asset generation.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFEurope represented around 20% share, equal to nearly USD 0.44 billion in 2026, supported by strong game development clusters in the U.K., Germany, France, Sweden, Finland, and Poland. The region is using generative AI for procedural content creation, localization, story development, art design, and testing workflows. Adoption remains steady as studios balance creative use of AI with copyright, transparency, and regulatory requirements.

Latin America accounted for nearly 5% share, equal to around USD 0.11 billion in 2026, supported by expanding gaming communities, mobile-first game consumption, and growing independent game development activity. Brazil and Mexico are the key contributors, with developers increasingly using AI tools to reduce production time and support content creation at lower cost.

The Middle East and Africa held an estimated 3% share, equal to nearly USD 0.07 billion in 2026, supported by rising investment in gaming, esports, digital entertainment, and technology infrastructure. Countries such as Saudi Arabia and the UAE are investing heavily in gaming ecosystems, which is expected to support future use of generative AI in game design, virtual environments, localization, and player engagement.

Risk Factors & Market Barriers

Regulatory & Compliance Risks

The generative AI in the gaming market faces regulatory risks linked to copyright, AI disclosure, data privacy, child safety, player protection, and content moderation. Game companies must confirm whether AI-generated assets, dialogue, code, music, and character designs can be used commercially without infringing third-party rights. This is important because games contain many protected creative elements, including artwork, sound, scripts, voice, characters, and software code.

Copyright risk is one of the biggest compliance issues. The U.S. Copyright Office has been reviewing AI-related copyright questions, including AI-generated works and the use of copyrighted materials in AI training. For game developers, this creates uncertainty around ownership, licensing, training data, and whether AI-assisted assets can receive strong copyright protection.

Market Adoption Barriers

Creative resistance is a major adoption barrier. In 2026, 52% of game industry professionals said generative AI is having a negative impact on the industry. Many developers are concerned about originality, job displacement, low-quality output, copyright risk, and loss of creative identity. This means vendors must position AI as an assistive tool, not as a replacement for artists, writers, designers, and programmers.

Quality control is another barrier. Generative AI output can be inconsistent, repetitive, inaccurate, or unsuitable for production use. Game assets must meet technical needs such as polygon limits, animation quality, texture quality, performance standards, engine compatibility, and art direction. Poor output can increase review time instead of reducing workload.

Key Market Segment

By Component

Software

Services

By Technology

Machine Learning

Deep Learning

Natural Language Processing

Computer Vision

Reinforcement Learning

Generative Adversarial Networks

Others

By Content Type

Game Assets

Character Design

Story and Dialogue Generation

Level and Environment Design

Music and Sound Generation

Animation Generation

Others

By Game Type

Action Games

Role-Playing Games

Simulation Games

Strategy Games

Sports Games

Adventure Games

Others

By Platform

PC Games

Console Games

Mobile Games

Cloud Gaming

AR and VR Games

By Application

Procedural Content Generation

Non-Player Character Behavior

Game Testing and Quality Assurance

Player Experience Personalization

In-Game Asset Creation

Narrative and Dialogue Generation

Others

By End User

Game Developers

Game Studios

Independent Developers

Esports Companies

Media and Entertainment Companies

Others

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Faster creation of game assets and design concepts | +3.2% | High in North America, Europe, China, Japan, South Korea, and India | Reduces early production time for concept art, character ideas, environments, textures, and prototype assets. |

Rising use of AI tools by game developers | +2.8% | Strong in mature gaming markets and large studio hubs | Increases adoption of AI-assisted coding, testing, level design, dialogue generation, and production planning. |

Demand for lower development cost and shorter production cycles | +2.5% | High across independent studios, mobile gaming firms, and mid-sized developers | Supports wider use of generative AI for repetitive creative and technical tasks that normally require large production teams. |

Growth of procedural content generation | +2.2% | Strong in PC, console, mobile, and live-service game ecosystems | Enables larger game worlds, repeatable missions, dynamic environments, and personalized gameplay experiences. |

Expansion of AI-supported player engagement tools | +1.9% | High in North America, Asia Pacific, and Europe | Supports personalized quests, AI NPCs, adaptive difficulty, automated moderation, and real-time content updates. |

Restraint Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Copyright and intellectual property concerns | -2.4% | High in North America, Europe, Japan, and South Korea | Slows adoption where studios need clear ownership of AI-generated assets, scripts, music, and visual content. |

Resistance from artists, developers, and gaming communities | -2.1% | Strong in Western markets and premium game development communities | Creates reputational risk when players or creative teams reject AI-generated content as low-quality or unethical. |

Inconsistent quality of AI-generated content | -1.8% | Common across all regions | Requires human review, editing, and quality control, which reduces some of the expected productivity benefit. |

High computing and tool subscription cost | -1.5% | Higher impact on small studios and independent developers | Limits large-scale use of advanced models for real-time generation, 3D content, animation, and voice production. |

Lack of clear internal governance | -1.3% | High across studios experimenting with AI tools | Creates risk around data leakage, tool misuse, brand consistency, licensing, and production approval workflows. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

AI-assisted game prototyping for small studios | +2.9% | High in India, Southeast Asia, Latin America, Europe, and North America | Helps smaller teams test ideas faster, create early playable versions, and reduce dependence on large production budgets. |

Generative AI for NPC behavior and dialogue | +2.6% | Strong in RPG, simulation, open-world, and live-service game markets | Enables more dynamic characters, adaptive conversations, and personalized story experiences. |

Automated testing and bug detection | +2.3% | High in large studios, mobile gaming, and live-service platforms | Improves quality assurance speed and supports faster release cycles for frequent updates. |

Personalized game content and adaptive gameplay | +2.0% | Strong in mobile, online, cloud gaming, and subscription-based platforms | Supports player retention through tailored missions, difficulty levels, rewards, and content recommendations. |

AI tools for localization and global publishing | +1.7% | High in Asia Pacific, Europe, Latin America, and multilingual gaming markets | Reduces time and cost for translation, dubbing support, subtitles, and cultural adaptation. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing creative control with AI automation | -2.2% | High in North America, Europe, Japan, and South Korea | Requires studios to maintain artistic direction while using AI for support tasks without weakening game identity. |

Managing disclosure and transparency expectations | -1.9% | Strong in Western markets and digital game platforms | Creates pressure to clearly disclose AI-generated content and avoid consumer backlash. |

Integrating AI tools into existing game engines and pipelines | -1.7% | Common across large and mid-sized studios | Requires workflow changes across art, design, engineering, QA, localization, and publishing teams. |

Avoiding bias, unsafe outputs, and inappropriate content | -1.5% | High in online games, children’s games, and global releases | Increases the need for moderation, guardrails, testing, and human approval before content reaches players. |

Protecting jobs and maintaining team morale | -1.3% | High in creative production hubs | Creates internal resistance when teams view AI as a threat to junior roles, creative labor, and long-term skill development. |

Recent Development

NVIDIA Corporation, June 2026 - NVIDIA released RTX Remix 1.5 with RTX IO compression, Smooth Normals, and RTX Remix Skills agents, supporting AI-assisted modding and faster remastering of classic games.

Unity Software Inc., 2026 - Unity continued to expand Unity AI with in-editor assistance, asset generation, workflow automation, AI Gateway support, and MCP Server integration for game developers.

Epic Games, June 2026 - Epic Games increased generative AI use across Fortnite asset workflows and Unreal Engine development tools, which also created debate among developers over AI-assisted creative production.

Roblox Corporation, 2026 - Roblox continued to strengthen its creator ecosystem as a user-generated gaming platform, with AI tools increasingly positioned around faster content creation, coding support, and creator productivity.

Amazon Web Services, Inc., March 2025 - AWS highlighted generative AI-powered game development solutions at GDC 2025, including Miro-based mood boards for character and world design and AI-driven game ad personalization.

Research Methodology

Step 1: Primary Research - Primary research is conducted through direct discussions with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. These interviews help understand real market demand, pricing movement, supply chain conditions, production trends, and customer requirements.

Step 2: Secondary Research - Secondary research is carried out using company filings, annual reports, regulatory databases, government publications, trade association data, and verified industry sources. This step helps collect reliable background information and supports the overall market assessment.

Step 3: Data Validation - Collected data is validated through source triangulation, historical trend review, demand-side checks, and supply-side assessment. Multiple sources are compared to reduce errors and improve the accuracy of the final insights.

Step 4: Market Estimation - Market estimation is completed using both bottom-up and top-down approaches. Product demand, regional consumption, company presence, application-level usage, and end-use industry adoption are reviewed to estimate the market size and structure.

Step 5: Forecasting Approach - Market forecasts are prepared by studying regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. This approach helps identify future growth patterns and possible market changes.

Step 6: Quality Review - The final data and findings are reviewed by analysts through peer validation, outlier checks, internal consistency checks, and final publication approval. This ensures that the report maintains accuracy, clarity, and research quality.

Step 7: AI Policy - AI is not used as a primary data source. All published insights are checked against human-verified evidence, and final conclusions are reviewed by analysts before publication.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

NVIDIA Corporation

Unity Software Inc.

Epic Games, Inc.

Electronic Arts Inc.

Ubisoft Entertainment SA

Roblox Corporation

Microsoft Corporation

Sony Interactive Entertainment LLC

Tencent Holdings Limited

NetEase, Inc.

Amazon Web Services, Inc.

Google LLC

Meta Platforms, Inc

Adobe Inc.

Stability AI Ltd.

OpenAI

Inworld AI

Others

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

AI Visual Inspection System Market Revenue to Hit USD 315.2 billion by 2035

Global AI Visual Inspection System Market Size, Growth Analysis By Offering (Hardware Systems, Industrial Cameras, Sensors and Imaging Hardware, Software Platforms, AI Inspection Software, Vision Analytics Tools, Services), By Technology (Deep Learning-Based Vision Systems, Machine Learning Algorithms, Traditional Computer Vision Systems, Edge AI Vision Processing, Other AI Vision Technologies), By Application (Defect Detection & Quality Control, Assembly Verification, Measurement & Gauging, Packaging & Label Inspection, Other Industrial Inspection Applications), By Industry Vertical (Electronics & Semiconductor Manufacturing, Automotive Industry, Pharmaceuticals & Healthcare, Food & Beverage Manufacturing, Logistics & Warehousing, Other Industrial Verticals), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Cloud Computing Market Size to Surpass USD 17.5 Trillion by 2035

Global Cloud Computing Market Size, Share Analysis By Type (Public Cloud, Private Cloud, Hybrid Cloud), By Service Model (Software as a Service, Infrastructure as a Service, Platform as a Service), By Enterprise Type (Large Enterprises, Small and Medium Enterprises), By Industry (BFSI, IT and Telecommunications, Government, Consumer Goods and Retail, Healthcare, Manufacturing, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI For Financial Services Market Size to Reach USD 315.5 billion by 2035

Agentic AI For Financial Services Market Size, Share Segmented by Application (Fraud Detection and Anti-Money Laundering, Virtual Assistants and Chatbots, Credit Assessment, Risk and Compliance Management, Investment Advisory, Claims Processing, and Others), By Component (Solutions and Services), By Deployment Mode (Cloud, On-Premise, and Hybrid), By End-User (Commercial Banks, Investment Banks, Asset Management Firms, and Other Financial Institutions), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI in HR & Recruitment Market Size to Reach USD 120.5 billion by 2035

Global Agentic AI in HR & Recruitment Market Size, Go-to-Market and Sales Strategy Analysis By Deployment Mode (Cloud-Based, On-Premises), By Enterprises (Small and Medium Enterprises (SMEs), Large Enterprises), By Application (Talent Acquisition & Recruitment, Employee Onboarding, Employee Engagement & Retention, Workforce Analytics, Others), By End-User Industry (IT & Telecommunications, Healthcare, Retail & E-commerce, BFSI, Manufacturing, Education, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035