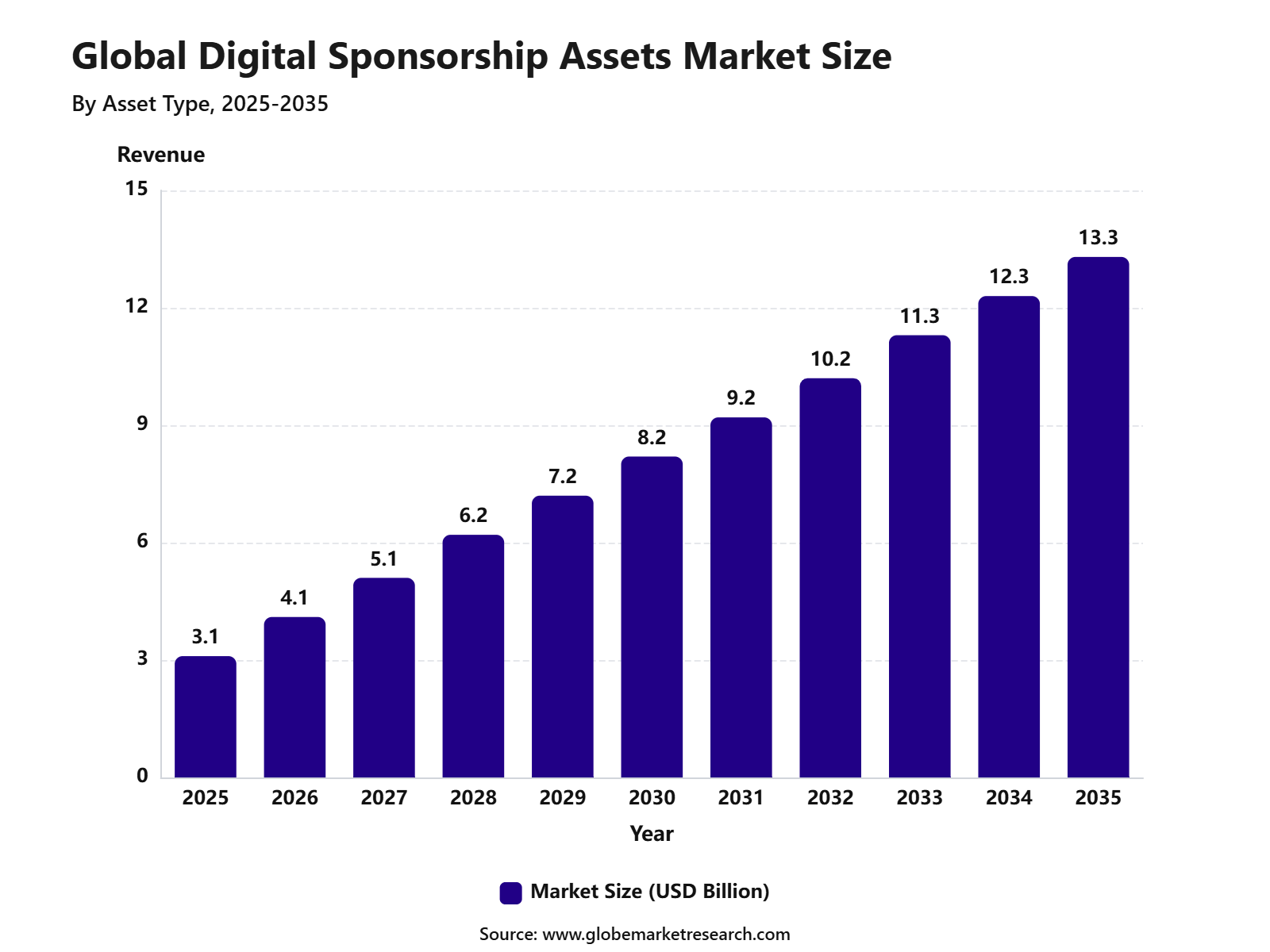

Revenue, 2025

$3.1 Bn

Forecast, 2035

$13.3 Bn

CAGR, 2025-2035

15.7%

Report Coverage

Global

Market Size and Forecast

The Global Digital Sponsorship Assets Market was worth USD 3.1 billion in 2025 and is expected to reach USD 13.3 billion by 2035, growing at a CAGR of 15.7% from 2025 to 2035. North America held the largest regional share of 39.3% in 2025, supported by strong digital advertising spending, high sports and entertainment sponsorship activity, advanced fan engagement platforms, and wider use of branded digital content across streaming, social media, esports, and live event channels.

The Digital Sponsorship Assets Market includes online and virtual sponsorship inventory used by brands to increase visibility across digital platforms. These assets include branded video content, social media placements, livestream overlays, virtual signage, digital banners, sponsored posts, in-app branding, esports sponsorship assets, and fan engagement activations. The market is closely linked with sports leagues, media rights holders, event organizers, digital publishers, creator platforms, and advertising technology providers.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains strong as brands shift more sponsorship spending toward measurable and interactive digital channels. Growth can be attributed to rising live streaming consumption, increasing social media engagement, expanding esports audiences, and stronger demand for data-based sponsorship performance tracking. The development of virtual events, connected TV advertising, digital fan experiences, and AI-supported audience targeting is expected to support long-term market demand.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 3.1 billion |

Forecast Revenue (2035) | USD 13.3 billion |

CAGR (2025-2035) | 15.7% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Digital activations led the asset type segment with 36.5% share, supported by higher brand engagement, interactive campaigns, and real-time audience participation.

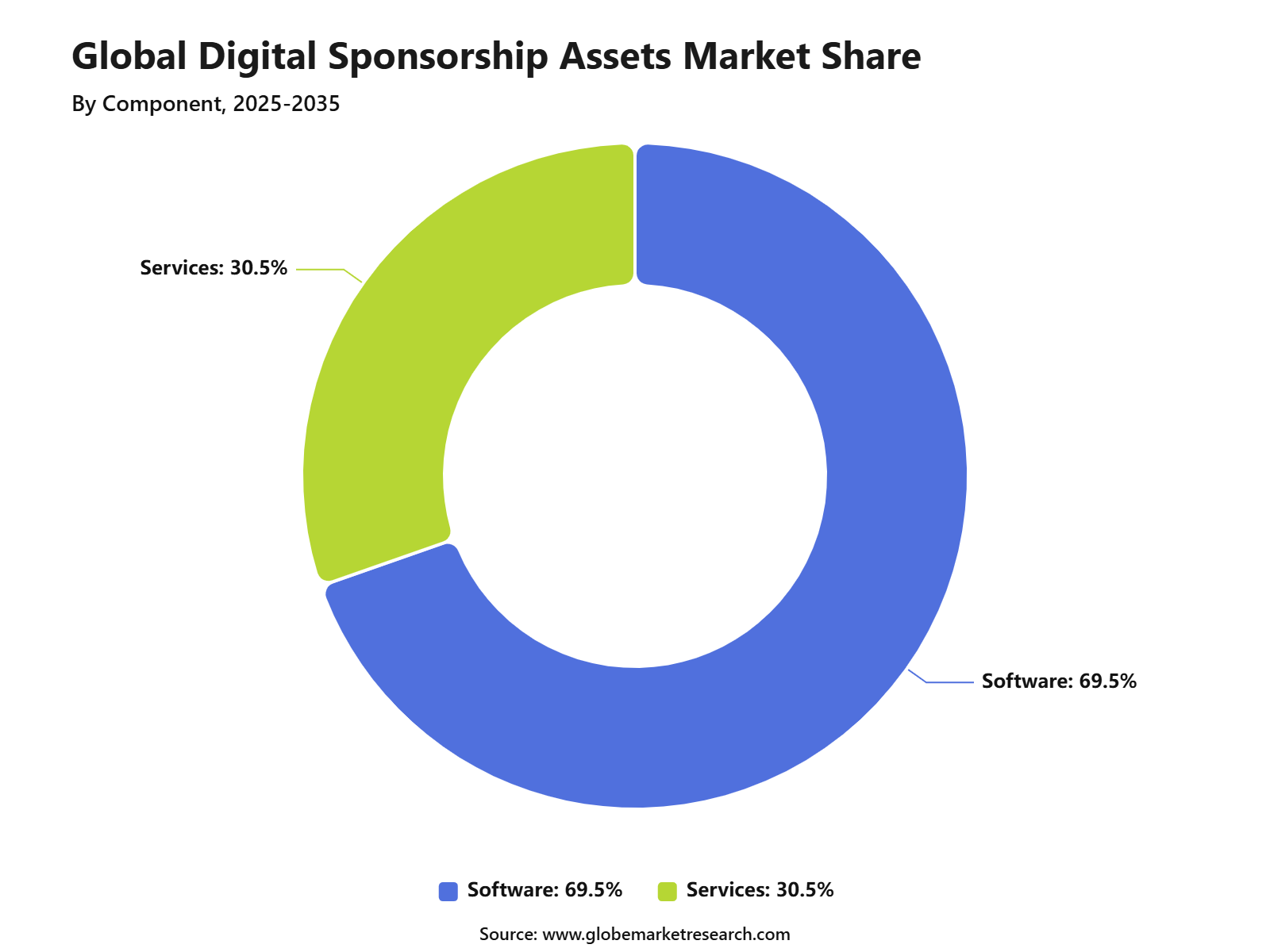

Software accounted for 69.5% share by component, driven by strong demand for sponsorship management, asset tracking, campaign analytics, and performance measurement tools.

Cloud-based deployment held 72.9% share, supported by scalability, remote access, faster campaign execution, and easier integration with digital marketing platforms.

Sports led the application segment with 47.8% share, driven by large fan bases, live event visibility, digital content monetization, and strong sponsor participation.

Brands accounted for 40.9% share by end user, supported by rising investment in digital sponsorship assets to improve reach, engagement, and campaign returns.

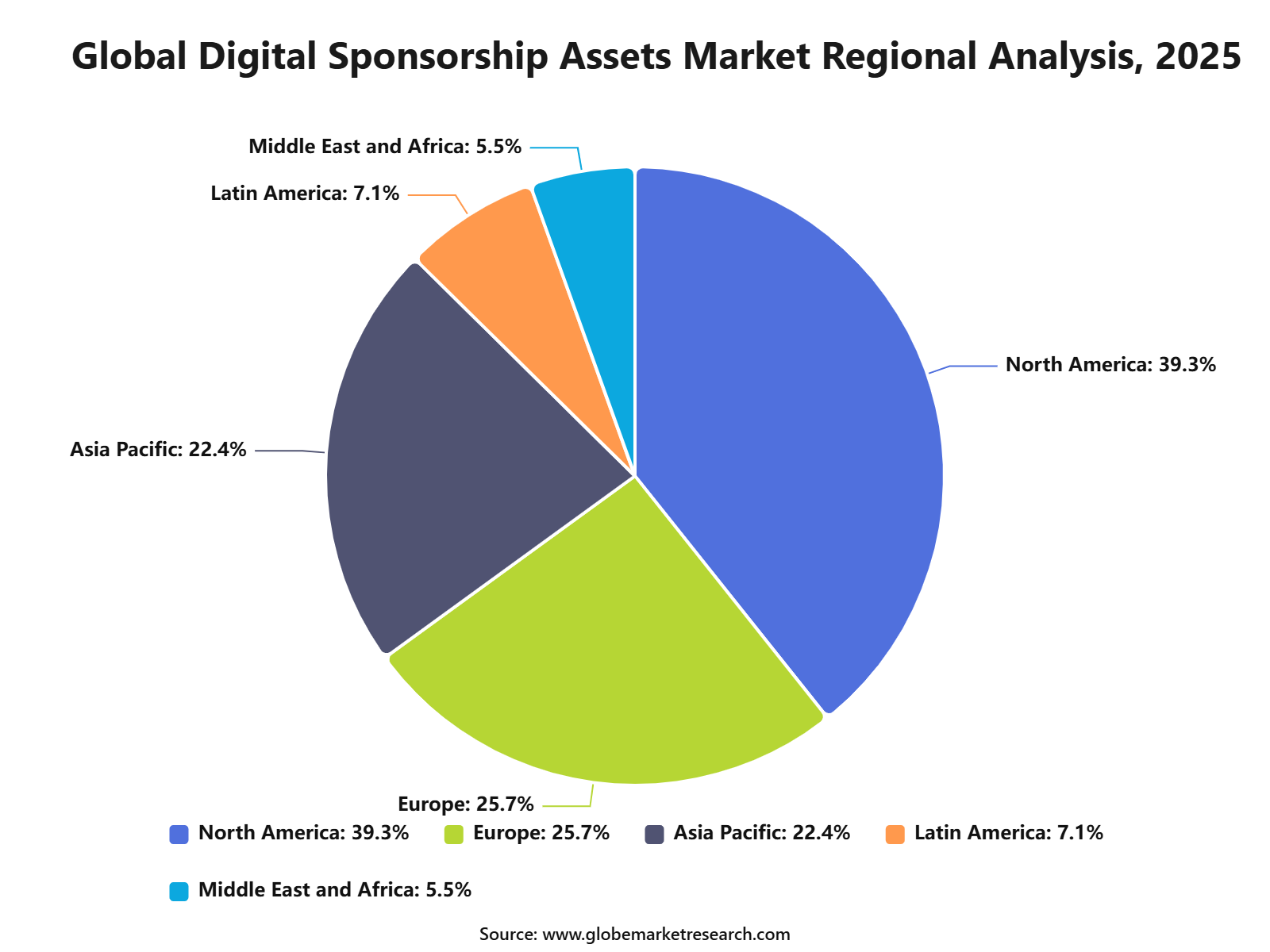

North America led the digital sponsorship assets market with 39.3% share, supported by mature sports media, strong brand spending, advanced digital infrastructure, and high adoption of sponsorship technology.

How AI Impacts the Digital Sponsorship Assets Market?

AI is changing the Digital Sponsorship Assets Market by making sponsorship inventory more measurable, personalized, and performance-driven. Brands are no longer buying only logo placement, static banners, or broad audience exposure. AI helps rights holders and agencies analyze fan behavior, content engagement, audience segments, and sponsor fit before building campaign packages. In sports and entertainment, this is important because 70% of surveyed industry respondents said sponsors now demand more digital content, while 81% of executives expanded their AI use in the past year to improve efficiency and reduce cost.

AI also improves content creation and asset activation across social media, streaming, connected TV, mobile apps, creator campaigns, and virtual events. Sponsorship teams can use AI to generate campaign ideas, customize branded content, test creative formats, translate posts, select creators, and optimize placements for different audience groups. IAB reported that U.S. creator ad spend is expected to reach USD 44 billion in 2026, while three in four brands are already using or planning to use AI for creator marketing-related tasks. This supports stronger use of AI in branded creator content, sponsored posts, influencer-led campaigns, and social sponsorship assets.

AI is also improving sponsorship ROI measurement. It can track engagement, sentiment, watch time, click behavior, conversion signals, audience overlap, and brand lift across multiple digital channels. This helps sponsors compare the value of different assets, such as social reels, livestream overlays, app banners, branded videos, newsletter placements, and creator integrations. IAB stated that only 30% of agencies, brands, and publishers had fully integrated AI across the media campaign lifecycle in 2025, but half of those not yet fully integrated expected to do so by 2026. This shows that adoption is still developing, but the direction is clearly toward AI-assisted planning, activation, and reporting.

Market Entry and Revenue Strategy

The go-to-market strategy for the Digital Sponsorship Assets Market is being shaped by measurable digital inventory across social media, creator content, streaming video, mobile apps, websites, live-event platforms and fan communities. Brands are no longer buying only logo exposure. They are buying trackable assets such as sponsored posts, branded video segments, creator integrations, in-app placements, digital signage, live-stream overlays, shoppable content and data-backed fan engagement campaigns.

The strongest sales route is a bundled sponsorship model, where rights holders, agencies and digital platforms combine media reach, content production, analytics and performance reporting in one package. This approach is supported by the wider digital advertising shift. U.S. digital advertising revenue reached USD 294.6 billion in 2025, rising 13.9% year over year, while social media ad revenue reached USD 117.7 billion with 32.6% annual growth. This shows that sponsor budgets are moving toward channels where engagement, clicks, conversions and audience behavior can be measured clearly.

Digital video is also becoming a core sales channel for sponsorship assets. U.S. digital video ad spending reached USD 78 billion in 2025, while digital video is projected to surpass USD 80 billion in 2026 and exceed 60% of total TV and video ad spend for the first time. This supports higher demand for sponsored streaming assets, branded content slots, connected TV placements, live sports integrations and short-form video activations.

By Asset Type

Digital activations led the asset type segment with 36.5% share, supported by rising brand interest in interactive fan engagement, creator-led campaigns, social media challenges, shoppable content, and live digital experiences. These assets are preferred because they allow sponsors to move beyond static logo placement and track engagement through clicks, shares, sign-ups, views, and conversion signals.

The strength of digital activations can also be linked to the faster shift toward creator and social-first advertising. In 2025, nearly 48% of creator ad buyers viewed creators as a "must buy", while creator advertising was reported to be growing much faster than overall media spending, showing how brands are giving more weight to digital engagement formats.

By Component

Software dominated the component segment with 69.5% share, as sponsorship teams increasingly rely on platforms for asset tracking, audience measurement, content scheduling, valuation, campaign reporting, and rights-holder management. The segment benefits from the need to measure digital assets in real time, especially across social media, streaming, websites, apps, and virtual events.

The software-led position is also strengthened by automation and AI use in advertising workflows. Public video advertising data shows that 86% of buyers were already using or planning to use generative AI for video ad creative, while advertisers were also using AI for audience versions, visual changes, and context-based creative updates.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Deployment Mode

Cloud-based deployment led the deployment mode segment with 72.9% share, supported by easier access, faster campaign updates, remote collaboration, and lower internal infrastructure requirements. Cloud platforms allow sponsors, agencies, rights holders, and event organizers to manage campaigns across social media, streaming, mobile apps, websites, and live-event channels from a shared system.

The preference for cloud deployment is supported by wider enterprise technology adoption. Flexera’s 2026 State of the Cloud Report stated that 73% of organizations use hybrid cloud environments, combining public and private cloud systems. This shows that cloud-based operating models have become common for organizations managing digital workloads across several business functions.

Cloud platforms are also becoming more important because AI-driven campaign tools require scalable computing and real-time data access. Flexera reported that GenAI had become the third most widely used public cloud service in 2026, rising to 58% from 50% in the previous year. This supports cloud-based sponsorship systems that depend on automated reporting, campaign optimization, content testing, and audience analytics.

By Application

Sports led the application segment with 47.8% share, supported by strong fan loyalty, live-event visibility, athlete influence, digital streaming, fantasy sports, social media communities, and sponsor demand for measurable engagement. Sports sponsorship assets work well in digital formats because fans interact before, during, and after events across apps, online video, creator content, team pages, and fan communities.

The segment is supported by high digital participation among sports fans. Deloitte Digital reported in 2025 that 71% of professional athlete or sports team fans engage in online communities, 57% interact with creators within fandoms, and 50% seek out fan-created media. These figures show why sports properties are using digital sponsorship assets to deepen fan relationships beyond stadium signage and broadcast exposure.

Sports sponsorship also has a direct link with consumer buying behavior. A 2025 Sports Business Journal survey found that 66% of consumers were more likely to purchase from companies that sponsor sports they like, up from 59% in 2022. This supports sports as the leading application area because well-aligned sponsorships can influence brand preference, purchase intent, and customer loyalty.

By End User

Brands held the largest end-user share at 40.9%, driven by their need to improve visibility, build audience trust, activate sponsorship rights, and connect marketing spending with clear outcomes. Brands are using digital sponsorship assets across social media, connected TV, live events, creator campaigns, branded content, and fan engagement programs.

Brand demand is being shaped by the move toward automated and performance-led media buying. IAB reported that programmatic advertising rose 20.5% year over year in 2025 to USD 162.4 billion, gaining USD 27.6 billion in new spending. This matters for digital sponsorship because brands increasingly expect sponsorship inventory to be measurable, targetable, and connected to campaign performance data.

Brands are also expanding sponsorship activity through digital video and creator-linked formats. IAB reported in 2026 that two in three digital video buyers were live, testing, or planning to use agentic AI for digital video campaigns, while another 28% were actively investigating it. This supports the use of software-enabled digital sponsorship assets that can adapt creative, targeting, and reporting more quickly.

By Region

North America led the regional segment with 39.3% share, supported by a mature sponsorship ecosystem, strong sports media culture, advanced digital advertising infrastructure, and high adoption of performance-based marketing tools. The region has deep participation from brands, agencies, sports leagues, entertainment properties, streaming platforms, and event organizers.

The region’s leadership is being strengthened by major live sports activity in 2026. FIFA states that the 2026 World Cup is the first edition with 48 teams, hosted across Canada, Mexico, and the United States. This creates a large activation window for sponsors across host cities, stadiums, fan zones, broadcast platforms, and social media communities.

North America also has a strong audience base for digital sponsorship growth. Reuters reported in June 2026 that soccer fandom in North America grew 10.9% over five years to more than 136 million fans, while 72% of fans access content through TV or streaming and social media remains an important secondary channel. This supports the region’s strong position in digital sponsorship assets across sports and connected fan experiences.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRevenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across social media assets, streaming and OTT sponsorship, creator-led campaigns, sports digital activations, website and app sponsorships, virtual event assets and performance-linked brand partnerships. Social media remains one of the largest pools because sponsored content can be targeted, tested and measured faster than traditional sponsorship formats. In 2025, social media accounted for USD 117.7 billion of U.S. digital ad revenue, equal to 40.0% of total digital ad revenue.

Creator partnerships are becoming a high-value revenue layer within digital sponsorship assets. U.S. creator ad spend is projected at USD 37.1 billion in 2025, up 26% year over year, and is expected to reach USD 44.1 billion in 2026. Nearly 48% of creator ad buyers now treat creators as a "must-buy" media channel, which indicates that brands are using creator content not only for awareness but also for conversion, product launch support and community building.

Sports and entertainment rights holders are also expanding digital sponsorship inventory. In 2025, NFL team sponsorship revenue reached USD 2.7 billion, up 8% from the previous season, with SponsorUnited tracking more than 3,700 deals and 36,000 social posts across the NFL and its athletes. Women’s sports also created new digital sponsorship opportunities, with more than 5,300 sponsorship deals tracked across major women’s sports properties in 2025 and 17.5% year-over-year growth, excluding NIL.

Financial Impact

The financial impact of digital sponsorship assets is visible in higher monetization per fan, stronger reporting for sponsors and better pricing power for rights owners. Digital assets can be sold as standalone inventory or added to larger sponsorship packages, improving total deal value. Programmatic advertising revenue reached USD 162.4 billion in 2025, growing 20.5% year over year, which shows that automated buying and measurable digital placements are becoming important for sponsorship pricing and campaign delivery.

For brands, the financial benefit comes from clearer performance tracking. Sponsored digital assets can be linked to website visits, app installs, product sales, sign-ups, ticket purchases, merchandise sales and audience retargeting. In sports-focused social engagement, 76% of media and entertainment brands said social is very or extremely important to their digital marketing strategy, and social media efforts contributed to an average 11.3% year-over-year rise in B2C revenue. Social-first brands saw an even stronger 14.1% average revenue increase.

For rights holders and event owners, digital sponsorship assets reduce dependence on fixed physical inventory such as venue boards and printed branding. Social communities, creator partnerships and live-stream content can create repeatable revenue before, during and after an event. Deloitte’s 2025 sports social research found that 42% of social media users follow sports and recreation topics, 53% of fans on social media are part of communities around athletes, teams, gaming or esports, and 54% of brands identify creator partnerships or paid social campaigns as the most effective tactics for driving live-event viewership.

Segment Covered in the Report

By Asset Type

Digital Activations

Social Media Assets

Streaming and OTT Assets

Website and App Sponsorship Assets

Virtual Event Assets

NFT and Blockchain Sponsorship Assets

Others

By Component

Software

Services

By Deployment Mode

Cloud-Based

On-Premises

By Application

Sports

Entertainment

Corporate

Non-Profit

Others

By End User

Brands

Agencies

Rights Holders

Event Organizers

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Driver Analysis

Shift Toward Digital Video, Social Media, and Streaming Assets

The Digital Sponsorship Assets Market is being driven by the rapid shift of brand spending toward digital video, social media, and connected TV formats. IAB projected that U.S. digital video ad spending will surpass USD 80 billion in 2026, growing 11% year over year and nearly 20% faster than the total ad market. Digital video is also expected to exceed 60% of total TV and video ad spend in 2026, which strengthens demand for sponsor-branded video assets, OTT placements, social clips, and livestream integrations.

This driver is important because sponsorship value is no longer limited to stadium signage, event naming, or broadcast exposure. Brands now expect rights holders, teams, events, and creators to deliver measurable digital assets across YouTube, Instagram, TikTok, apps, websites, streaming platforms, and fan communities. IAB also noted that social video is growing faster than CTV, supported by AI personalization and rising creator economy investment.

Restraint Analysis

Measurement Gaps and Fragmented Digital Inventory

A major restraint for the Digital Sponsorship Assets Market is the difficulty of measuring value across many platforms. Sponsorship assets can appear across social posts, app banners, streaming overlays, virtual signage, branded content, creator integrations, and live event content. Each format may use different metrics, such as views, reach, engagement, watch time, click-through rate, brand lift, and conversion. This makes it harder for sponsors to compare asset value and justify renewal decisions.

Measurement complexity is increasing as sponsorship moves deeper into CTV and streaming. IAB Tech Lab stated that CTV growth has created new ad formats and that standardization is needed across formats such as pause ads, menu ads, screensavers, in-scene ads, squeezebacks, and overlays. Without common standards, advertisers can face inconsistent reporting, rendering issues, and weaker campaign accountability.

Opportunity Analysis

Creator-Led Sponsorship and Women’s Sports Growth

A strong opportunity is emerging from creator-led sponsorship assets and athlete-driven digital content. SponsorUnited reported that the 2025 NFL season included more than 3,100 brands, 3,700 deals, and 36,000 social posts across the league and its athletes. This shows that digital sponsorship assets are becoming a core part of sports partnerships, especially where athletes, teams, and leagues can extend sponsor visibility beyond matchday.

Women’s sports also present a strong growth opportunity for digital sponsorship assets. SponsorUnited reported a 12% rise in women’s sports sponsorships in 2024 to 2025, covering more than 4,700 brands, 6,700 deals, and 11,000 social posts across selected leagues and athletes. This creates new scope for brands to use digital activations, player content, behind-the-scenes media, short-form video, and community-led sponsorship campaigns.

Challenge Analysis

Brand Safety, Fraud Risk, and Trust in Digital Assets

The key challenge for the Digital Sponsorship Assets Market is maintaining trust as digital inventory becomes more automated and distributed. IAB noted that digital video buyers are facing issues such as signal loss and non-human traffic, while targeting has become a top investment criterion for TV and video buying. This means sponsors need stronger verification, cleaner data, and trusted reporting before increasing budgets across digital assets.

Brand safety and ad fraud risks also create pressure for platforms, rights holders, and agencies. IAB Tech Lab states that its standards focus on areas such as brand safety, ad fraud, identity, privacy, ad experiences, measurement, and programmatic effectiveness. For market participants, the challenge is to prove that sponsored digital assets are viewable, brand-safe, accurately measured, and linked to real fan engagement.

Recent Developments

In June 2026, Omnicom launched Acxiom Fan Graph, a sports marketing intelligence tool designed to help brands understand sports audiences more deeply. The tool combines media, commerce, and consumer engagement signals, which can support better targeting for digital sponsorship assets, fan campaigns, and partnership planning. This development shows that sponsorship value is increasingly being judged through audience data, not only through logo visibility.

In July 2025, PubMatic launched an AI-powered Live Sports Marketplace with FanServ as its first major partner. The platform allows advertisers to target specific live game moments across streaming platforms and gives access to NBA, WNBA, MLB, NHL, NWSL, and local sports inventory. This is important for digital sponsorship assets because brands can now align campaigns with high-attention sports moments in real time.

In September 2025, Madhive and FOX Television Stations expanded the Local Live Sports Marketplace for local advertisers. The marketplace gives access to more than 16 premium live sports products, including College Gameday, Monday Night Football, NFL, NBA, NHL, MLB, and NCAA programming. This development supports the shift toward connected TV, live sports inventory, and measurable digital sponsorship placements for regional advertisers.

Mergers

In September 2025, Fubo shareholders approved the company’s planned merger with Hulu + Live TV. The transaction remained subject to regulatory approvals, and Disney was expected to own about 70% of Fubo after closing. For the digital sponsorship assets market, this merger is significant because live sports streaming platforms are becoming larger, more structured channels for digital sponsorship inventory, branded content, and targeted advertising.

In February 2025, Outbrain completed its acquisition of Teads, and the combined company began operating under the Teads brand. The deal created a larger open-internet advertising platform that combines branding, performance marketing, premium media, video, and AI-led targeting. Although this is an adtech merger rather than a pure sponsorship software deal, it is relevant because digital sponsorship assets increasingly depend on measurable media delivery, connected TV, and cross-screen brand exposure.

Acquisitions

In May 2025, EngageRM acquired Power’d Digital, a first-party channel platform. The acquisition is expected to help sports and entertainment organizations connect branded websites, apps, ticketing, VIP packages, memberships, merchandise, hospitality, and loyalty offerings more directly with fans. This improves the value of digital sponsorship assets by making fan engagement more owned, measurable, and commerce-linked.

In July 2025, Publicis Groupe acquired Bespoke Sports & Entertainment. Bespoke helps brands identify sports partnership opportunities, execute sponsorship programs, and measure sponsorship outcomes. The acquisition reflects a wider agency move toward sports, creator-led marketing, and measurable brand integration across fragmented media channels.

In September 2025, Minute Media acquired VideoVerse in its largest deal to date. VideoVerse owns Magnifi, an AI-driven tool that can automatically detect key sports moments and create short-form highlight videos in real time. This acquisition matters for digital sponsorship assets because short-form sports clips, social distribution, and branded highlight packages are becoming high-value assets for leagues, teams, publishers, and sponsors.

Funding

In May 2026, SponsorCX raised a multi-million-dollar Series A round led by Kickstart, with participation from BlueprintEquity, Capital Eleven, Frazier Group, Helm Ventures, and returning investors. The company said the funding will be used to expand AI capabilities within its sponsorship management platform. This supports the demand for automated asset tracking, fulfillment, reporting, and sponsorship portfolio management among rights holders.

In April 2025, SponsorCX also announced a USD 4.6 million investment round led by Kickstart. The company positioned the funding around modernizing sponsorship management, which still relies heavily on spreadsheets and fragmented tools across many organizations. This funding signals stronger investor interest in SaaS platforms that bring structure, visibility, and accountability to sponsorship assets.

In July 2025, EngageRM raised A$6 million in Series A funding led by Five V Capital. The funding was planned for team growth, technology expansion, and international market development. EngageRM’s platform is built around CRM, data, analytics, AI, machine learning, and stakeholder intelligence for sports and entertainment organizations, making it closely aligned with digital sponsorship asset management.

In June 2026, Sony Pictures Entertainment invested USD 100 million in Cosm and took a minority stake as lead investor in its Series C financing round. Cosm operates immersive venues that show live sports and entertainment through its Shared Reality technology. This investment is relevant because immersive venues create new premium digital sponsorship surfaces, including branded live-event experiences, venue media, and interactive fan engagement formats.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

KORE Software

SponServe

Hookit

Relo Metrics

StellarAlgo

Catapult

Octagon

Sportsdigita

Sponsoo

SponsorCX

EngageRM

Opendorse

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

5G RAN Market Size to hit USD 108.5 billion by 2035

Global 5G RAN Market Size, Go-to-Market and Sales Strategy Analysis By Component (Hardware, Software, Services), By Architecture Type (Traditional RAN, Open RAN), By Deployment (Public Networks, Private Networks), By End Use (Telecom Operators, Enterprise and Industrial Users), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Online Dating Market Size to hit USD 29.5 Bn by 2035

Global Online Dating Market Size, Go-to-Market Strategy Analysis By Type (Paying Online Dating, Non-Paying Online Dating), By Revenue Model (Subscription, Advertising-Supported, Other Model), By Platform (Web Portals, Applications), By Age Group (Adult, Baby Boomer, Generation X, Generation Z, Millennials), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

AI In Interior Design Market Size to hit USD 37.7 billion by 2035

Global AI In Interior Design Market Size, Go-to-Market Strategy Analysis By Component (Solution, Service), By Deployment (Cloud, On-Premises), By User Type (Homeowners, Real Estate Developers, Interior Designers, Architects, Corporate Clients), By Design Style (Traditional, Modern, Contemporary, Minimalist, Eclectic), By Technology Integration (3D Visualization Tools, Virtual Reality Solutions, Augmented Reality Applications, CAD Software, Machine Learning Algorithms), By Application (Residential Design, Commercial Design, Hospitality Design, Retail Spaces, Office Spaces), By Pricing Strategy (Subscription-Based, Freemium Model, Pay-Per-Use, One-Time License, Enterprise Licensing, Project-Based Pricing), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Facility Management Market Size to hit USD 4.3 Trillion by 2035

Global Facility Management Market Size, Go-to-Market Strategy Analysis By Service Type (Hard Services, Soft Services), By Offering (In-House, Outsourced), By End User (Commercial, Industrial, Government and Public Sector, Residential, Institutional, Others), By Service Provider (Single Service Providers, Integrated Facility Management Providers, Bundled Service Providers), By Contract Type (Annual Contracts, Flexible Contracts, Performance-Based Contracts), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035