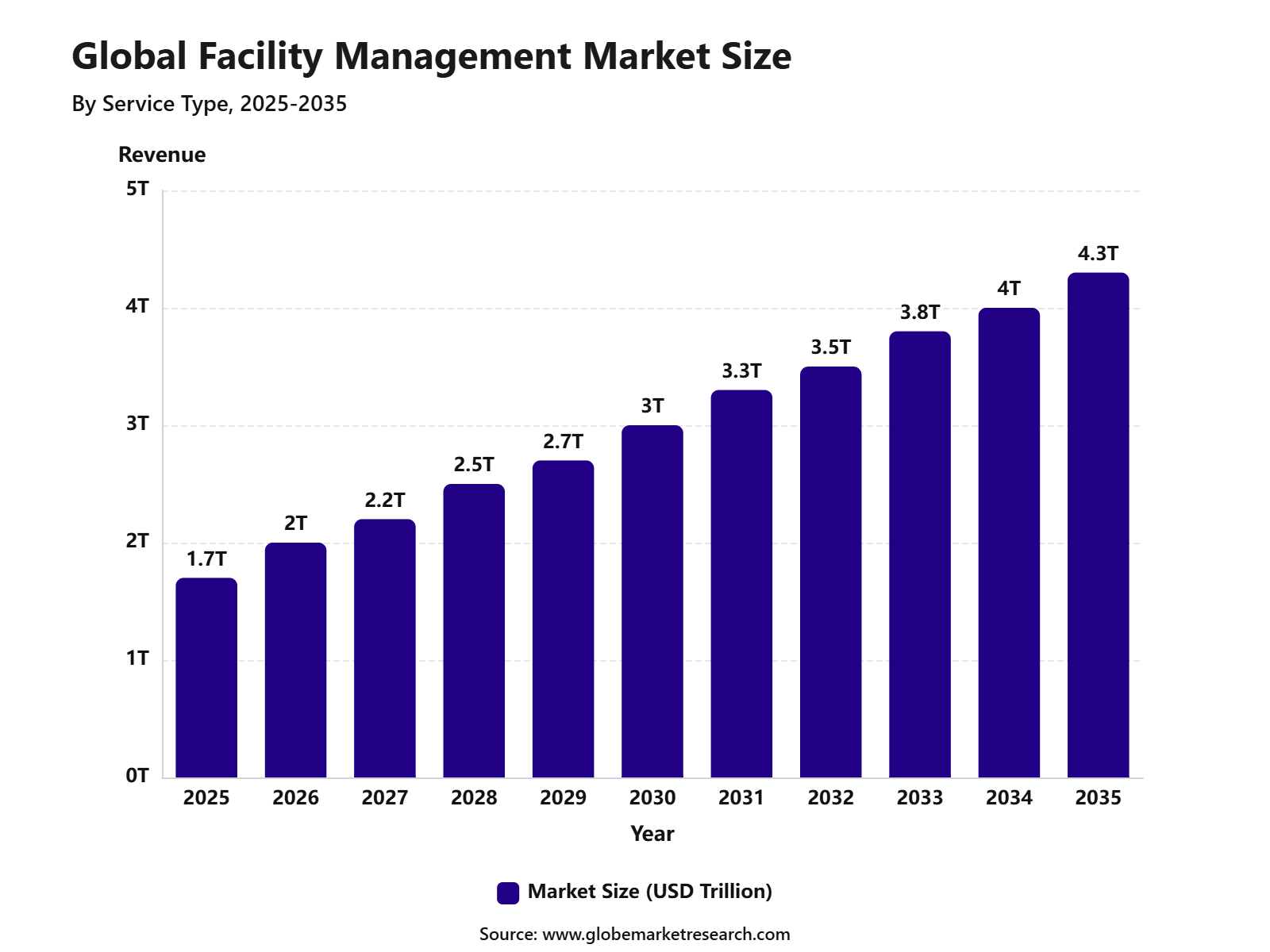

Revenue, 2025

$1.7 Trillion

Forecast, 2035

$4.3 Trillion

CAGR, 2025-2035

9.5%

Report Coverage

Global

Market Size and Forecast

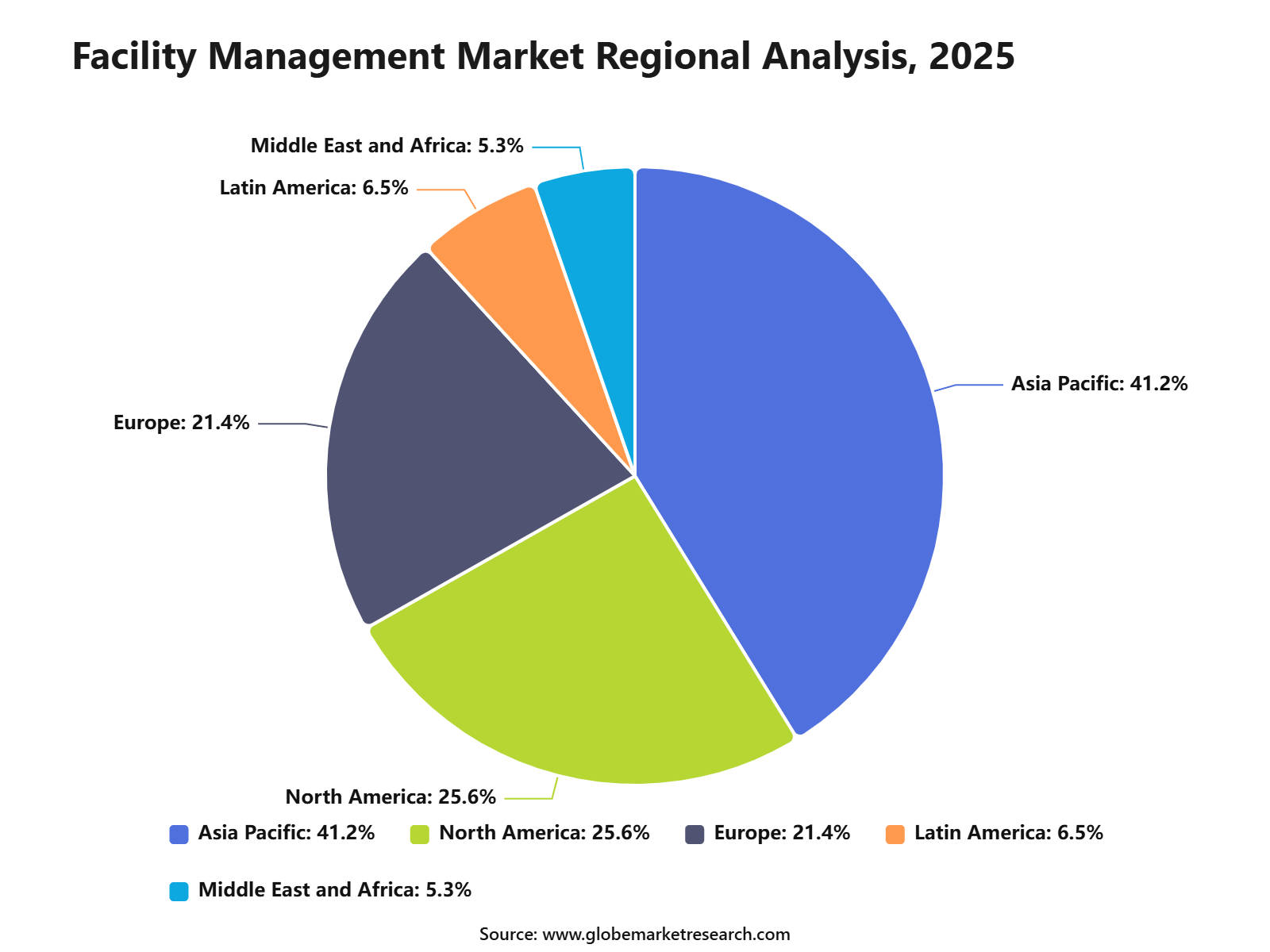

The Global Facility Management Market was worth USD 1.7 trillion in 2025 and is expected to reach USD 4.3 trillion by 2035, growing at a CAGR of 9.5% from 2025 to 2035. Asia Pacific held the largest regional share of 41.2% in 2025, supported by rapid urban development, expanding commercial infrastructure, rising industrial activity, and growing demand for outsourced facility services across offices, factories, hospitals, airports, retail spaces, and smart buildings.

The Facility Management Market includes services used to manage, maintain, and improve buildings, assets, workplaces, and operational environments. These services include hard facility management such as HVAC, electrical, plumbing, fire safety, and maintenance, along with soft services such as cleaning, security, waste management, catering, landscaping, and space management. The market is closely linked with real estate operations, workplace safety, energy efficiency, sustainability compliance, and digital building management systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe market outlook remains strong as organizations continue to focus on cost control, asset performance, employee safety, and efficient workplace operations. Growth can be attributed to rising demand for integrated facility management, increasing adoption of smart building technologies, and wider outsourcing by commercial and industrial users. The expansion of IoT-enabled monitoring, predictive maintenance, energy management systems, and sustainability-focused building services is expected to support long-term market growth.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 1.7 Trillion |

Forecast Revenue (2035) | USD 4.3 Trillion |

CAGR (2025-2035) | 9.5% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Key Market Insights

Hard services led the service type segment with 55.1% share, supported by strong demand for building maintenance, HVAC systems, electrical services, plumbing, safety systems, and asset upkeep.

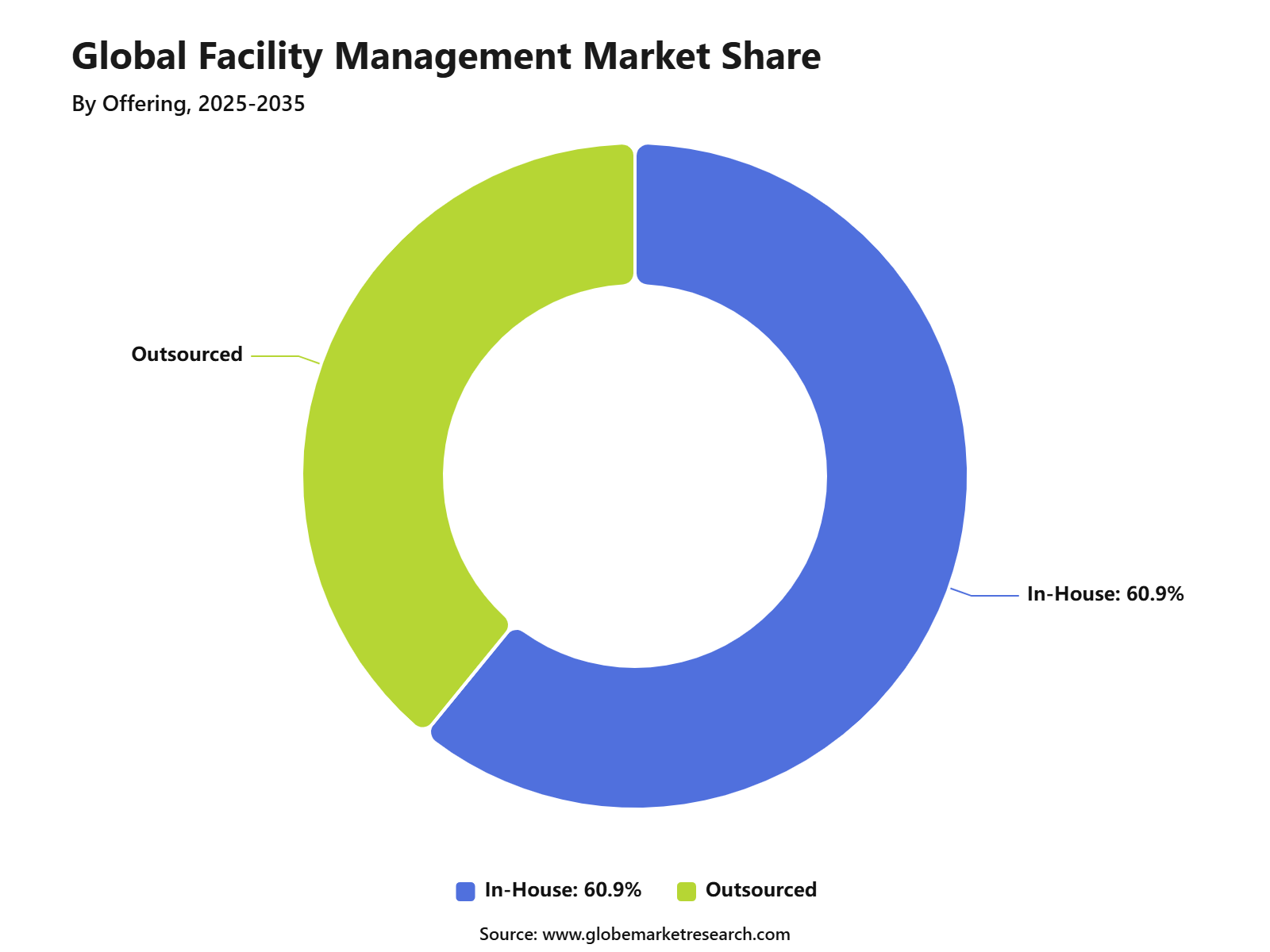

In-house facility management accounted for 60.9% share, driven by stronger operational control, direct workforce supervision, faster response time, and better alignment with internal business needs.

Commercial end users held 35.8% share, supported by high demand from offices, retail spaces, business parks, malls, hospitality facilities, and corporate buildings.

Integrated facility management providers captured 43.4% share, driven by growing preference for single-point service delivery, cost efficiency, centralized operations, and multi-service management.

Annual contracts accounted for 58.7% share, supported by predictable service planning, long-term maintenance needs, budget control, and stable provider-client relationships.

Asia Pacific led the facility management market with 41.2% share, supported by rapid urban development, expanding commercial infrastructure, industrial growth, and rising demand for organized facility services

Top Funding and Investment

Investment in the facility management market is moving toward technical services, mission-critical facilities, smart building software, semiconductor facility support, energy efficiency, and integrated workplace operations. Hard services and technical FM are gaining stronger investor attention, as building maintenance and mechanical and electrical deals increased by 24% in 2025 and represented 50% of FM deal activity, up from around 41% in 2024.

CBRE acquired Pearce Services for an initial cash purchase price of about USD 1.2 billion, with a potential earn-out of up to USD 115 million. Pearce provides design engineering, maintenance, and repair services for digital and power infrastructure. Its expected 2025 revenue mix includes critical power and cooling systems at 34%, renewable energy generation and storage at 30%, wireless and fiber networks at 29%, and EV charging networks at 7%.

Bain Capital agreed to acquire Apleona from PAI Partners in 2025. Apleona is a leading European integrated facility management provider with more than 40,000 employees and EUR 4 billion in turnover. The investment is expected to support organic growth, acquisitions, technical FM expansion, and building decarbonization services. Apleona has already integrated 14 strategic acquisitions across Europe, including Gegenbauer Group in 2023.

ABM entered into an agreement to acquire WGNSTAR for around USD 275 million in cash. WGNSTAR provides managed workforce solutions, equipment support, installation, maintenance, and production tool management for semiconductor and high-technology facilities. The company has more than 1,300 employees and is expected to generate about USD 135 million in 2025 revenue.

Vista Equity Partners made a strategic growth investment in Joblogic, including over GBP 100 million in new primary capital. Joblogic provides field service management software used by contractors and facility managers across HVAC, plumbing, electrical maintenance, building fabric maintenance, and other skilled trades. The funding will support Joblogic’s AI roadmap and European expansion.

Adoption Indicators and AI Usage Areas

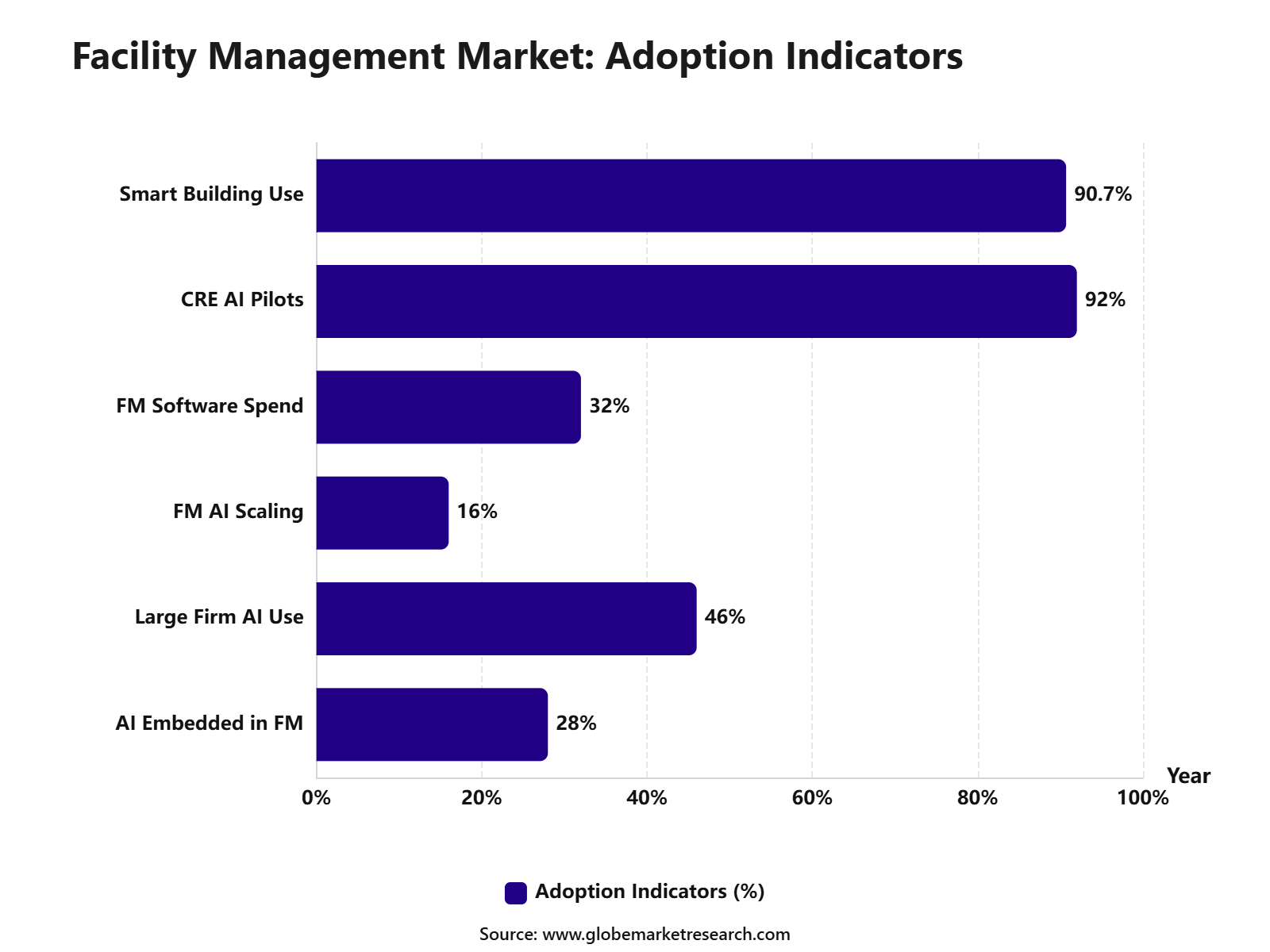

Based on data from JLL, the Facility Management Market is moving toward technology-enabled and AI-supported operations, as 28% of organizations have already embedded AI in FM activities, rising to 46% among very large organizations. Cost pressure remains the main adoption driver, with 84% of FM leaders citing budget constraints and rising operating costs as a top concern, while 81% identify cost efficiency and budget optimization as a leading priority.

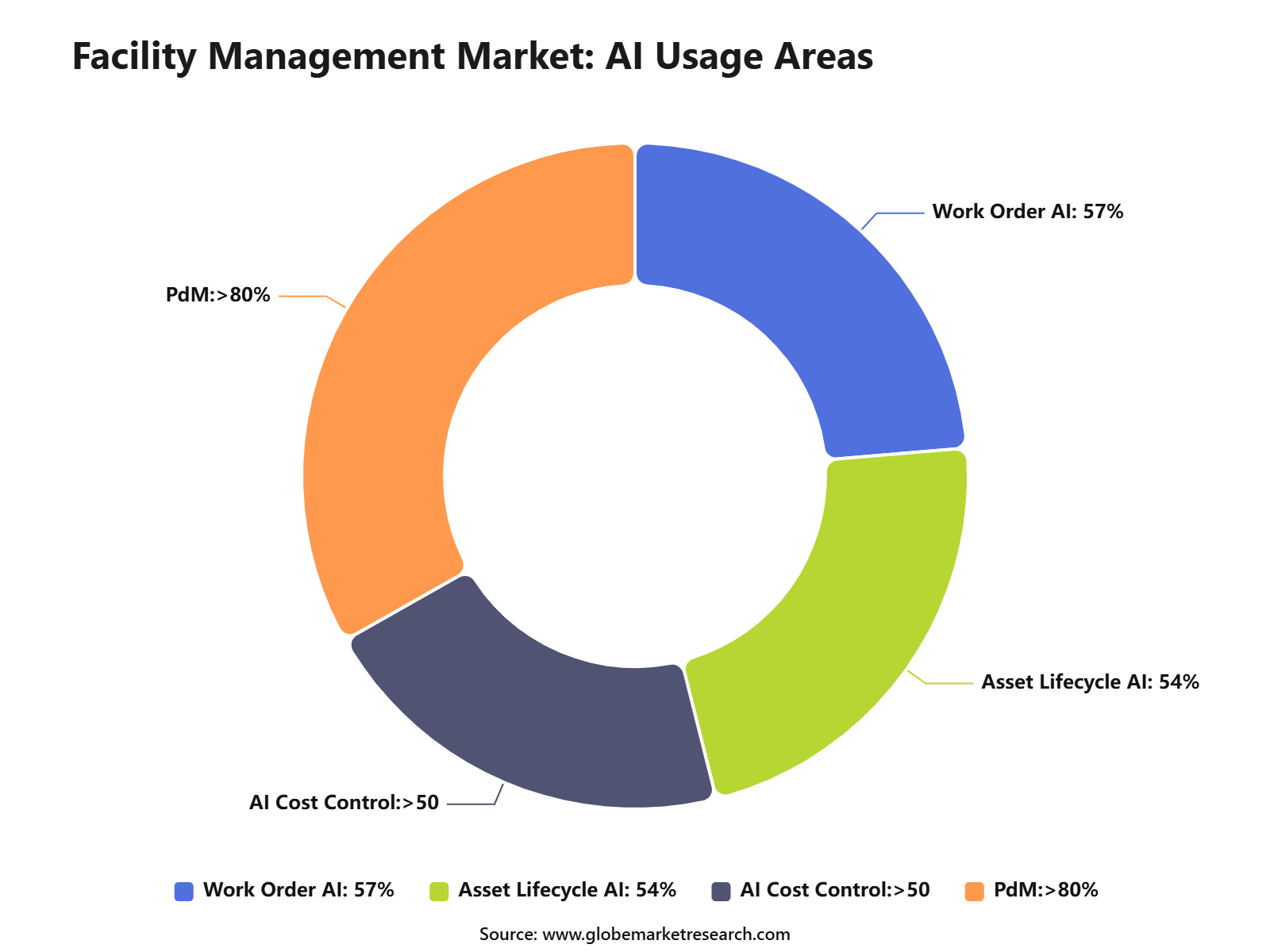

Technology spending is also becoming more focused, as 32% of organizations plan to increase FM software investment, with work order management leading software priorities at 57%. These trends show that facility management is shifting from routine service delivery to predictive maintenance, automated workflows, asset lifecycle visibility, and data-based cost control.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFHow AI Impacts the Facility Management Market?

AI is changing the Facility Management Market by moving operations from reactive service handling to predictive and data-led building management. Facility teams are using AI to monitor HVAC systems, lighting, elevators, pumps, access control, cleaning schedules, work orders, energy use, and occupancy patterns. In a 2026 Johnson Controls survey, 65% of business leaders and 67% of facility managers said their organizations already use AI to improve facility operation, utilization, and maintenance.

AI has the strongest impact on predictive maintenance. Instead of waiting for equipment failure, AI can analyze sensor data, vibration, temperature, runtime, pressure, fault history, and service records to detect early warning signs. Johnson Controls reported that among organizations already using AI, 47% of facility managers use it for predictive maintenance, while 52% of facility managers planning new AI adoption in the next year are prioritizing predictive maintenance. This helps reduce emergency repair costs, downtime, tenant complaints, and asset failure risk.

Energy management is another major area of impact. Buildings account for around 30% of global final energy consumption and 26% of global energy-related emissions, according to the IEA. AI can help facility managers reduce energy waste by adjusting HVAC, lighting, ventilation, and equipment use based on occupancy, weather, utility prices, and operating schedules. This is especially useful for offices, hospitals, schools, airports, malls, hotels, factories, and mixed-use buildings where energy demand changes throughout the day.

By Service Type

Hard services led the service type segment with 55.1% share, supported by the essential role of technical building operations. These services include electrical systems, HVAC maintenance, plumbing, fire safety, elevators, building repairs, and energy systems that are required to keep facilities safe and functional.

The growth of this segment can be attributed to the rising need for reliable infrastructure performance across commercial buildings, industrial sites, hospitals, airports, educational campuses, and retail spaces. Hard services are usually treated as critical because failure in these systems can directly affect safety, compliance, and daily operations.

Hard services also remain highly important because building owners are placing more focus on preventive maintenance and asset life extension. Regular inspection, planned servicing, and technical support help reduce breakdowns, improve energy use, and maintain business continuity.

By Offering

In-house facility management held the leading offering share of 60.9%, supported by direct control over facility operations, service quality, and staff coordination. Many organizations prefer in-house teams because they understand internal workflows, building requirements, and operational priorities more closely.

The segment is also supported by the need for faster response in large facilities where service delays can affect productivity. In-house teams can manage daily maintenance, housekeeping coordination, vendor supervision, and emergency issues with better internal alignment.

In-house facility management remains preferred where security, compliance, and sensitive operations are important. Sectors such as healthcare, manufacturing, government facilities, and corporate campuses often retain internal teams to maintain stronger control over performance and accountability.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy End User

Commercial facilities accounted for 35.8% share by end user, supported by strong demand from offices, retail spaces, malls, hospitality properties, business parks, and mixed-use buildings. These facilities require continuous cleaning, maintenance, security, energy management, and workplace support services.

The commercial segment is driven by the need to maintain safe, comfortable, and efficient workspaces. Facility management helps property owners and tenants improve building performance, reduce downtime, and provide better experiences for employees, visitors, and customers.

Commercial buildings also require consistent service quality because occupancy, brand image, and tenant retention are closely linked to building condition. This keeps facility management services important across both premium properties and large multi-tenant assets.

By Service Provider

Integrated facility management providers led the service provider segment with 43.4% share, supported by demand for bundled services under one coordinated model. These providers manage multiple functions such as maintenance, cleaning, security, energy support, workplace services, and vendor coordination.

The segment is gaining preference because integrated models reduce complexity for building owners and corporate occupiers. Instead of managing many separate contractors, clients can work with a single provider that offers centralized reporting, standardized service levels, and clearer accountability.

Integrated facility management also supports better cost control and operational planning. By combining services under one contract structure, organizations can improve coordination, reduce service duplication, and create a more consistent facility experience across multiple sites.

By Contract Type

Annual contracts led the contract type segment with 58.7% share, supported by the recurring nature of facility operations. Buildings require regular maintenance, cleaning, safety checks, repairs, and support services throughout the year, making annual agreements practical for both clients and providers.

The segment is preferred because annual contracts provide predictable service coverage and better budget planning. They allow organizations to define service levels, response times, reporting formats, and compliance responsibilities in advance.

Annual contracts also help service providers plan staffing, equipment, schedules, and vendor resources more efficiently. This improves service continuity and allows facility managers to focus on long-term performance instead of repeated short-term procurement.

By Region

Asia Pacific led the regional segment with 41.2% share, supported by rapid urban development, expanding commercial construction, and rising demand for professional building management. The region has strong activity across offices, industrial parks, transport hubs, healthcare facilities, retail centers, and residential complexes.

The regional lead is also driven by growing outsourcing and professionalization of facility services. As buildings become more complex, owners and occupiers are relying more on structured facility management to improve safety, efficiency, hygiene, and asset performance.

Asia Pacific remains highly attractive because large cities are expanding their built infrastructure and service expectations are rising. Demand is supported by commercial growth, industrial expansion, smart building adoption, and the need for better maintenance standards across high-traffic facilities.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Asia Pacific is expected to remain a strong growth region due to urbanization, infrastructure development, manufacturing expansion, and rising demand for professional facility services. China, India, Japan, Singapore, Australia, and Southeast Asia are important markets for commercial and industrial facility operations.

North America and Europe are mature markets with higher adoption of outsourced services, smart buildings, energy management, and compliance-led facility operations. The Middle East is also gaining importance through large infrastructure, hospitality, airport, healthcare, and commercial real estate projects.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Asia Pacific urban and industrial expansion | +2.5% | China, India, Southeast Asia | Builds future demand. |

North America outsourcing maturity | +1.9% | U.S. and Canada | Supports stable contracts. |

Europe sustainability-driven FM | +1.7% | Germany, UK, France, Nordics | Drives energy services. |

Middle East infrastructure growth | +1.3% | UAE, Saudi Arabia, Qatar | Supports hard services. |

Latin America professional FM adoption | +0.9% | Brazil, Mexico, Chile | Creates gradual growth. |

Go-to-Market and Sales Economics

The go-to-market approach for the Facility Management Market should focus on integrated service delivery, workplace reliability, cost control and compliance-led operations. Buyers are moving away from fragmented vendor management and are looking for bundled solutions across cleaning, maintenance, security, catering, energy management, space planning and technical services. JLL reported that global FM spending is projected to surpass USD 3 trillion by 2026, showing that facility management has become a strategic operating function rather than only a support service.

Sales economics are being shaped by rising operating costs and tighter client budgets. In JLL’s 2025 Global State of Facilities Management Report, 84% of FM leaders identified budget constraints and escalating operational costs as their main concern. This makes outcome-based contracts, self-delivery models, energy savings, service-level agreements and technology-enabled monitoring important for winning enterprise accounts.

The strongest selling model is expected to be integrated facilities management, where one provider manages multiple services under a single performance structure. JLL reported that 58% of organizations are consolidating contracts and suppliers, 52% are prioritizing providers with stronger self-delivery capability, and 37% are working with service partners to identify shared cost-saving opportunities. This supports larger, multi-site contracts with measurable savings and stronger client retention.

Revenue Potential Analysis

Revenue Landscape Across

Revenue potential is spread across hard services, soft services, integrated facility management, workplace services, energy management, sustainability reporting, asset maintenance, security, cleaning, food services and technical operations. Large outsourcing providers are showing stable demand. ISS reported 4.3% organic growth in 2025, while its operating margin before other items stood at 5.0%, supported by pricing actions, volume growth and operational improvements.

Corporate real estate and workplace services remain major revenue pools because large occupiers need consistent service quality across offices, industrial sites, healthcare buildings, universities and retail networks. CBRE reported USD 40.6 billion in total revenue for 2025, up 13%, with resilient business revenue also rising by 13%. This indicates that outsourced workplace and facilities-related services are benefiting from recurring demand even when transaction markets fluctuate.

Public buildings, education, healthcare and infrastructure also support long-term demand. In April 2026, U.S. public construction spending reached a seasonally adjusted annual rate of USD 532.7 billion, while educational construction stood at USD 113.7 billion. These assets require ongoing maintenance, cleaning, energy management, compliance checks and lifecycle upgrades, creating recurring service opportunities for facility management providers.

Financial Impact

The financial impact of facility management is mainly linked to lower operating costs, longer asset life, reduced downtime and improved building performance. Buildings account for around 30% of global energy demand, while commercial and public buildings represent about 30% of total building energy use. This makes energy management, HVAC optimization, preventive maintenance and building automation important financial levers for FM providers and property owners.

Technology adoption is becoming a direct margin driver. JLL stated that the FM industry is projected to expand by more than USD 800 billion globally by 2030, but labor shortages are expected to pressure service delivery. This creates a strong financial case for AI-based work order management, predictive maintenance, sensor-led monitoring, digital twins and workforce scheduling tools that can improve productivity without raising headcount at the same pace.

Labor availability remains one of the key cost risks. IFMA’s 2025 labor shortage analysis noted that more than 68% of U.S. facility operators and technicians are above age 45, while 21% remain active beyond retirement age. This may increase wage pressure, training cost and knowledge-transfer risk, but it also strengthens demand for managed services, remote monitoring, cross-training programs and digital facility documentation.

Segment Covered in the Report

By Service Type

Hard Services

Soft Services

By Offering

In-House

Outsourced

By End User

Commercial

Industrial

Government and Public Sector

Residential

Institutional

Others

By Service Provider

Single Service Providers

Integrated Facility Management Providers

Bundled Service Providers

By Contract Type

Annual Contracts

Flexible Contracts

Performance-Based Contracts

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Drivers Impact Analysis

The Facility Management Market is driven by rising demand for outsourced building operations, professional maintenance, energy management, cleaning, security, and workplace support services. Organizations are focusing more on cost control, asset life extension, employee safety, and operational efficiency across commercial, industrial, healthcare, education, and public infrastructure facilities.

Demand is also increasing as buildings become more complex and technology-enabled. Large enterprises, real estate owners, hospitals, airports, malls, manufacturing plants, and data centers are using facility management providers to manage hard services, soft services, compliance, and workplace experience under structured service contracts.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising outsourcing of facility services | +2.6% | North America, Europe, Asia Pacific | Drives contract growth. |

Growth in commercial infrastructure | +2.1% | Asia Pacific, Middle East, North America | Expands service demand. |

Increasing demand for hard services | +1.8% | Industrial, healthcare, commercial sites | Supports maintenance needs. |

Focus on energy efficiency | +1.5% | Europe, North America, developed Asia | Reduces operating cost. |

Rising workplace safety standards | +1.2% | Global | Improves compliance demand. |

Restraints Impact Analysis

The market faces restraints from high labor dependency, rising wage costs, and intense price competition among service providers. Many facility management contracts operate on tight margins, especially in cleaning, security, housekeeping, and basic maintenance services.

Another restraint is the fragmented vendor landscape in several regions. Small and mid-sized service providers often face challenges in technology adoption, service standardization, skilled workforce availability, and contract scalability, which can limit service quality and customer retention.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High labor dependency | -1.3% | Global service markets | Pressures margins. |

Rising wage and compliance costs | -1.1% | North America, Europe, Asia Pacific | Increases operating burden. |

Intense service price competition | -1.0% | Global | Reduces profitability. |

Shortage of skilled technicians | -0.8% | Developed and urban markets | Limits service capacity. |

Fragmented vendor ecosystem | -0.7% | Emerging markets | Affects service quality. |

Opportunities Impact Analysis

Major opportunities are emerging in integrated facility management, smart building services, predictive maintenance, energy optimization, and sustainability-linked facility operations. Clients are increasingly shifting from multiple single-service vendors to bundled service models that improve accountability and operational visibility.

The market also benefits from rising demand in data centers, healthcare, logistics, airports, manufacturing, and large commercial campuses. Providers that combine technical maintenance, digital reporting, compliance support, and workplace services can capture higher-value contracts.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Integrated facility management expansion | +2.5% | Global enterprise clients | Builds contract value. |

Smart building service adoption | +2.1% | North America, Europe, Asia Pacific | Improves operational control. |

Predictive maintenance demand | +1.8% | Industrial, healthcare, data centers | Reduces downtime. |

Energy management services | +1.6% | Europe, U.S., Japan, Australia | Supports efficiency goals. |

Growth in data center facility services | +1.3% | U.S., Europe, Asia Pacific | Adds technical demand. |

Challenges Impact Analysis

The key challenge for facility management providers is maintaining consistent service quality across multi-site operations. Large clients expect quick response times, trained staff, safety compliance, reporting accuracy, and measurable cost savings.

Another challenge is moving beyond low-value service delivery. Providers need to invest in digital tools, skilled technicians, asset monitoring, customer dashboards, and sustainability reporting to stay competitive in larger enterprise and government contracts.

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Maintaining service consistency | -1.2% | Multi-site enterprise clients | Affects retention. |

Managing large workforce operations | -1.0% | Global | Raises execution risk. |

Integrating legacy building systems | -0.9% | Older commercial assets | Slows digital adoption. |

Proving measurable cost savings | -0.8% | Corporate and public sectors | Impacts renewals. |

Cybersecurity risk in smart buildings | -0.6% | Connected facility portfolios | Raises technology concern. |

Recent Developments

In May 2026, Mitie secured a £27 million, three-year facilities management contract with Kingston and Richmond NHS Foundation Trust. The contract covers cleaning, portering, and waste management at Kingston Hospital. Mitie will use AI-driven task management and smartphone-based tracking to improve porter allocation, response time, and operational visibility.

In April 2026, CBRE reported strong momentum in critical infrastructure services, with revenue increasing 71% year over year, supported by Data Center Solutions and the contribution from Pearce Services. This shows that facility management demand is expanding beyond offices into data centers, power infrastructure, and mission-critical technical environments.

In May 2026, Cushman & Wakefield reported USD 2.5 billion in first-quarter revenue, up 11% year over year. Its Services revenue increased 9%, led by higher facilities management and project management revenue. This indicates that large enterprises are still outsourcing building operations, project delivery, and multi-site facility support to integrated service providers.

In May 2026, Compass Group was selected as the University of Kentucky’s preferred enterprise services partner. The planned long-term agreement brings together dining, hospitality, facilities, and healthcare support services across campus, healthcare, and athletics operations, with implementation scheduled to begin in July 2026.

Research Methodology

Methodology Area | Coverage Details |

|---|---|

Primary Research | Interviews with manufacturers, suppliers, distributors, consultants, procurement teams, and industry experts. |

Secondary Research | Company filings, annual reports, regulatory databases, government publications, trade associations, and verified industry sources. |

Data Validation | Cross-verification through source triangulation, historical trend review, demand-side checks, and supply-side assessment. |

Market Estimation | Bottom-up and top-down analysis based on product demand, regional consumption, company presence, and application-level usage. |

Forecasting Approach | Forecasts based on regulatory shifts, infrastructure investment, technology adoption, pricing trends, industrial expansion, and end-use demand. |

Quality Review | Analyst review, peer validation, outlier checks, internal consistency review, and final publication approval. |

AI Policy | AI is not used as a primary data source. All published insights are reviewed against human-verified evidence. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

CBRE Group, Inc.

Sodexo

Compass Group

ISS A/S

Johnson Controls International PLC

Dussmann Group

ISS World Services A/S

JLL

Compass Group PLC

Cushman & Wakefield

Aramark

Mitie Group plc

EMCOR Group, Inc.

Dussmann Group

Johnson Controls International plc

ENGIE SA

Veolia Environnement S.A.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

5G RAN Market Size to hit USD 108.5 billion by 2035

Global 5G RAN Market Size, Go-to-Market and Sales Strategy Analysis By Component (Hardware, Software, Services), By Architecture Type (Traditional RAN, Open RAN), By Deployment (Public Networks, Private Networks), By End Use (Telecom Operators, Enterprise and Industrial Users), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Online Dating Market Size to hit USD 29.5 Bn by 2035

Global Online Dating Market Size, Go-to-Market Strategy Analysis By Type (Paying Online Dating, Non-Paying Online Dating), By Revenue Model (Subscription, Advertising-Supported, Other Model), By Platform (Web Portals, Applications), By Age Group (Adult, Baby Boomer, Generation X, Generation Z, Millennials), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

AI In Interior Design Market Size to hit USD 37.7 billion by 2035

Global AI In Interior Design Market Size, Go-to-Market Strategy Analysis By Component (Solution, Service), By Deployment (Cloud, On-Premises), By User Type (Homeowners, Real Estate Developers, Interior Designers, Architects, Corporate Clients), By Design Style (Traditional, Modern, Contemporary, Minimalist, Eclectic), By Technology Integration (3D Visualization Tools, Virtual Reality Solutions, Augmented Reality Applications, CAD Software, Machine Learning Algorithms), By Application (Residential Design, Commercial Design, Hospitality Design, Retail Spaces, Office Spaces), By Pricing Strategy (Subscription-Based, Freemium Model, Pay-Per-Use, One-Time License, Enterprise Licensing, Project-Based Pricing), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Earned Wage Access Market Size to Exceed USD 93.5 billion by 2035

Global Earned Wage Access Market Size, Go-to-Market Strategy Analysis By Component (Solutions, Services), By Deployment Mode (Cloud-Based, On-Premises), By Access Type (Employer-Integrated EWA, Direct-to-Consumer EWA), By Pricing Model (Employer-Paid, Employee Transaction Fee, Subscription-Based, Hybrid), By End User (Large Enterprises, Small and Medium Enterprises, Gig Workers, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035