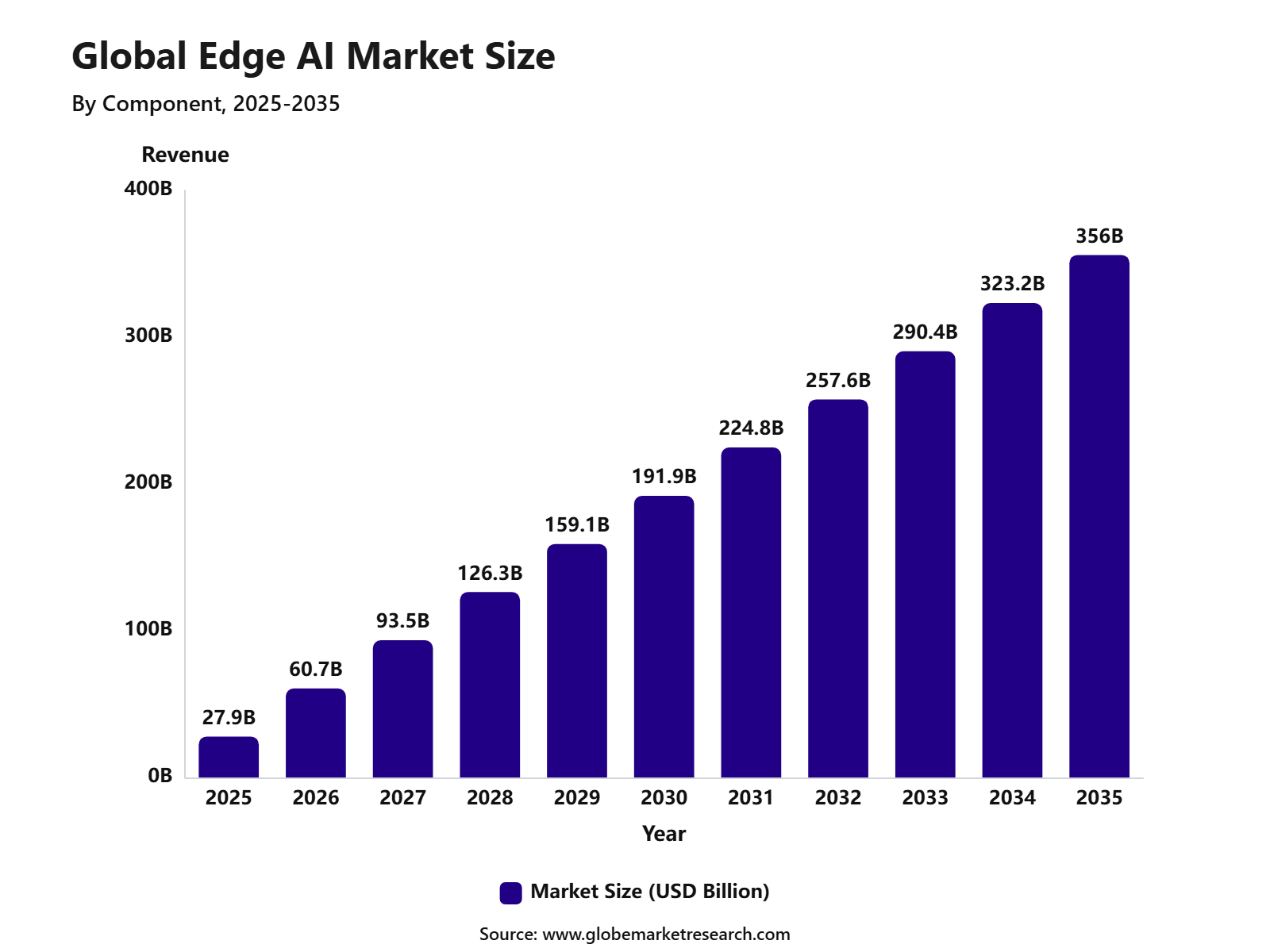

Revenue, 2025

$27.9 billion

Forecast, 2035

$356 billion

CAGR, 2025-2035

29%

Report Coverage

Global

Market Size and Forecast

What is the Edge AI Market Size?

The global Edge AI Market reached USD 27.9 billion in 2025 and is expected to grow to USD 356 billion by 2035, registering a CAGR of 29%. North America accounted for 40% share in 2025. The market growth is supported by the rising adoption of connected devices, increasing demand for real-time data processing, rapid deployment of 5G networks, growing use of AI in autonomous vehicles, smart manufacturing, healthcare, and surveillance systems, and the need to reduce cloud dependency while improving data privacy and low-latency decision-making.

The U.S. Edge AI Market was valued at approximately USD 8.5 billion in 2025 and is projected to expand at a CAGR of 28.5% from 2025 to 2035, driven by the rising adoption of real-time AI processing across manufacturing, automotive, healthcare, retail, surveillance, and smart infrastructure applications. The growth of the market can be attributed to the strong presence of cloud providers, semiconductor companies, AI software developers, and industrial automation firms, along with wider deployment of 5G networks, connected devices, edge servers, AI-enabled cameras, robotics, and autonomous systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFKey Insights

By Component, hardware accounted for 56.8% share, supported by rising use of AI chips, edge processors, sensors, and embedded modules in smart devices.

By Device Type, smartphones held 34.6% share, driven by wider integration of on-device AI for camera processing, voice assistance, security, and real-time personalization.

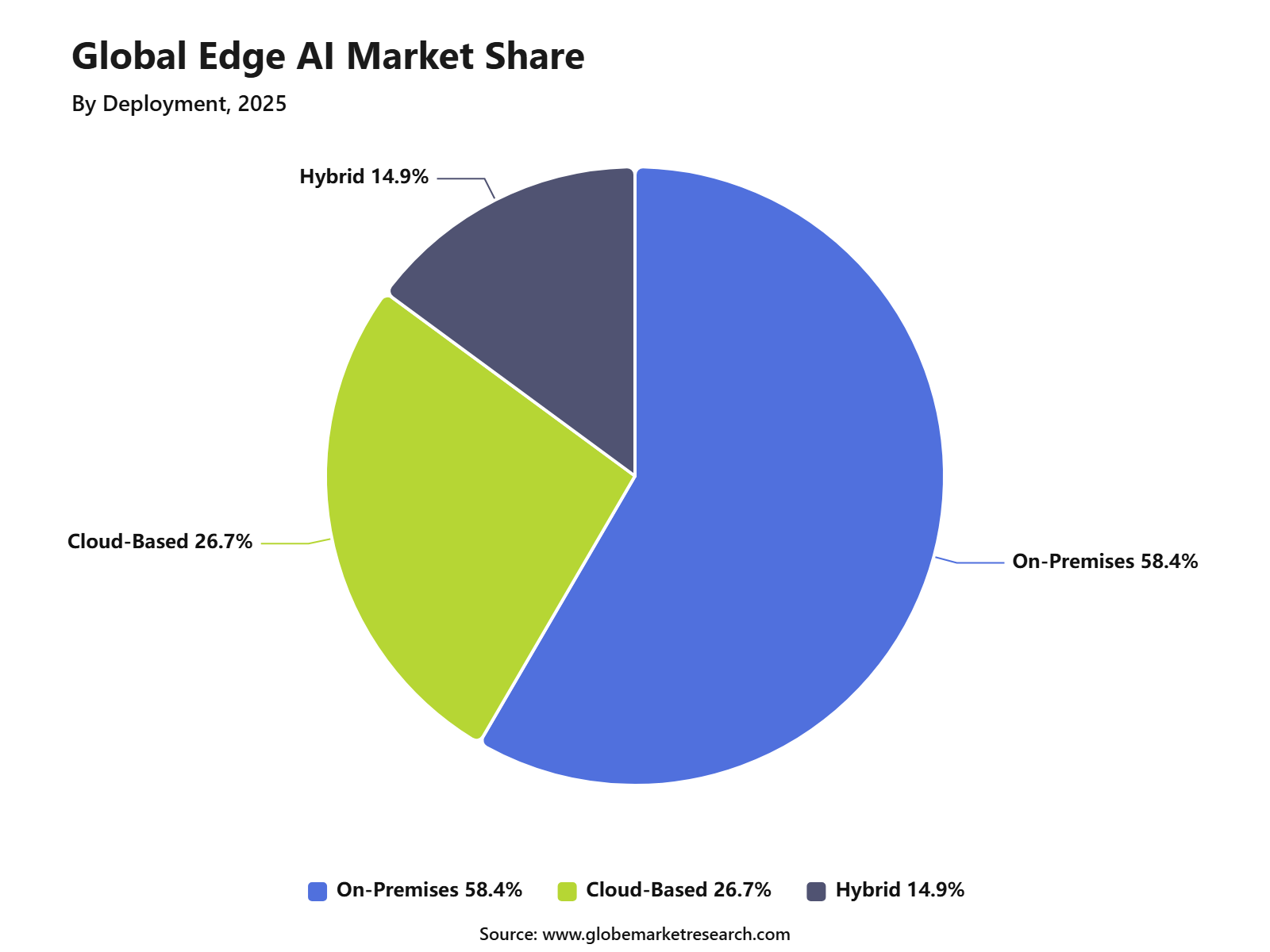

By Deployment, on-premises captured 58.4% share, as enterprises prefer local AI processing to reduce latency, improve data privacy, and support faster decision-making.

By Technology, machine learning represented 39.7% share, supported by its strong role in predictive analytics, image recognition, speech processing, and automated device intelligence.

By End-Use Industry, consumer electronics accounted for 27.9% share, owing to growing demand for smart home devices, wearables, smartphones, cameras, and AI-enabled appliances.

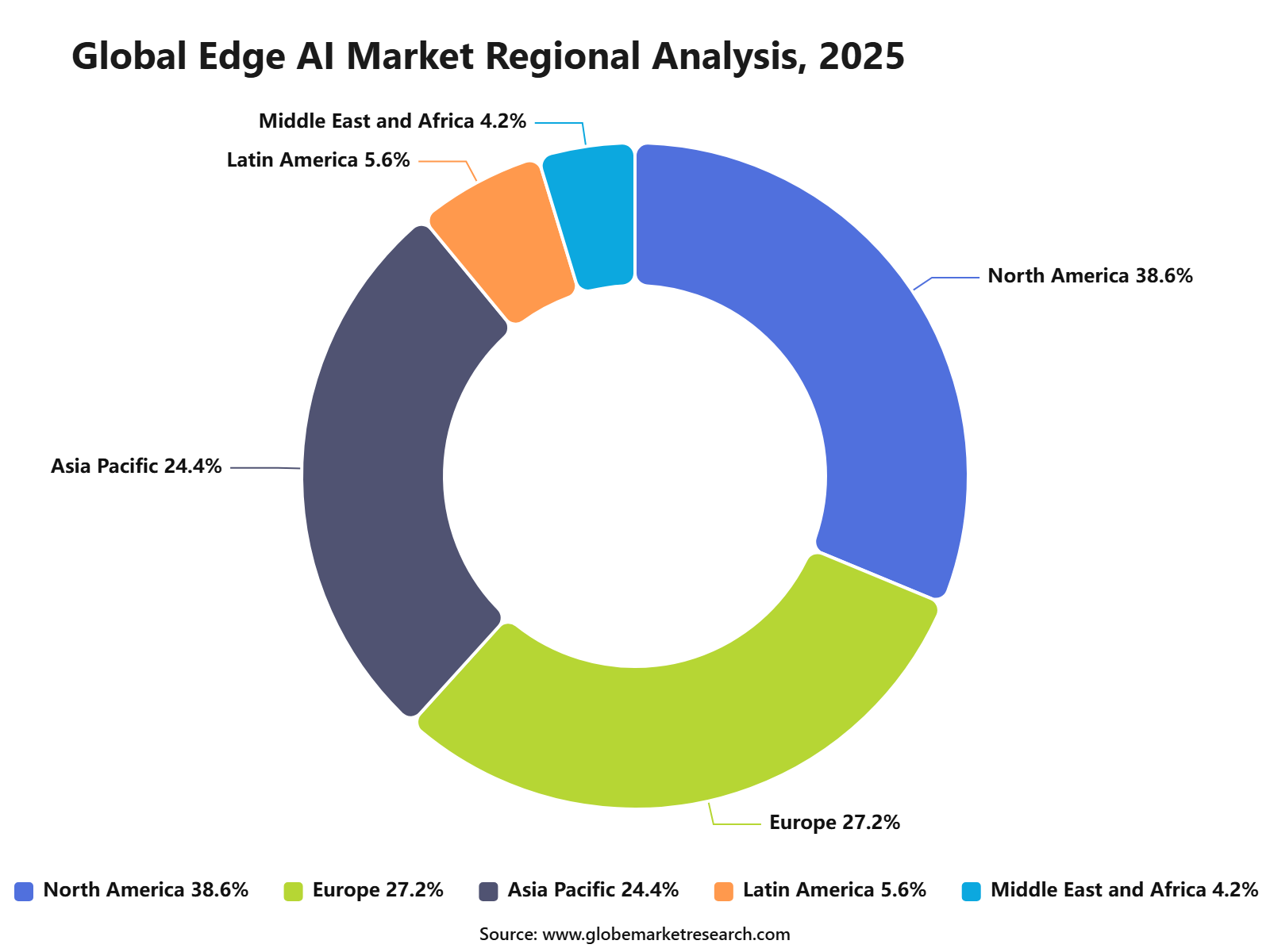

By Region, North America held 38.6% share, supported by strong semiconductor innovation, early AI adoption, advanced cloud-edge infrastructure, and high investment in connected devices.

Market Overview

Edge AI refers to the use of artificial intelligence models directly on local devices such as smartphones, cameras, robots, wearables, sensors, vehicles, and industrial machines. This reduces dependence on cloud-only processing and supports faster decisions closer to where data is produced. IBM defines edge AI as the deployment of AI models on local edge devices, while NVIDIA states that local edge processing helps reduce the need to send data back to the cloud or data centers.

The growth of the market can be attributed to rising demand for real-time AI decisions, low-latency computing, industrial automation, 5G expansion, and privacy-focused data processing. Ericsson reported that global 5G subscriptions had passed 3 billion by the June 2026 Mobility Report, while 5G carried 48% of global mobile data traffic at the end of 2025 and is projected to carry 85% by 2031. These connectivity improvements are supporting edge AI adoption in smart factories, connected vehicles, security cameras, remote healthcare, retail analytics, and autonomous systems.

Key reasons for adopting edge AI include faster response time, lower cloud traffic, improved privacy, better reliability during poor connectivity, and stronger control over operational data. In manufacturing, the need for local intelligence is supported by the rising use of robotics and machine vision. The International Federation of Robotics reported that 542,000 industrial robots were installed worldwide in 2024, with annual installations staying above 500,000 units for the fourth consecutive year. Asia accounted for 74% of new deployments, showing strong automation demand in production environments where edge AI can support defect detection, robot guidance, safety monitoring, and predictive maintenance.

Customer Acquisition

Edge AI vendors can target large enterprises first because AI usage is already stronger among bigger firms. In the U.S., overall business AI use stayed between 17% and 20% from December 2025 to May 2026, while 37% of firms with at least 250 employees reported using AI in business operations. This shows stronger customer acquisition potential in large manufacturing, retail, healthcare, telecom, automotive, and logistics accounts. Enterprise conversion can be supported through pilots and proof-of-concept projects. Among enterprise-scale companies with more than 1,000 employees, 42% had already deployed AI, while another 40% were exploring or testing AI. This creates a strong sales pipeline for Edge AI vendors offering AI chips, smart cameras, gateways, edge servers, and device management software.

Customer acquisition is also supported by connected device growth. Cisco estimated USD 29.3 billion networked devices and USD 14.7 billion machine-to-machine connections by 2023, showing a large base for edge-based AI processing in factories, vehicles, homes, cities, and industrial sites. Telecom partnerships can improve customer reach because 5G is becoming a key enabler for distributed AI. Global 5G subscriptions reached 3.1 billion in Q1 2026 and are forecast to reach 6.4 billion by the end of 2031, supporting stronger demand for low-latency Edge AI applications.

Revenue Potential Analysis

Revenue Opportunities

Industrial edge deployment offers strong revenue potential because 87% of enterprises adopting private wireless and on-premise edge reported ROI within one year. This supports demand for Edge AI in predictive maintenance, machine vision, safety monitoring, digital twins, and real-time production analytics.

Cost-saving use cases can improve sales conversion. In industrial edge and private wireless deployments, 81% of enterprises found setup costs lower than other options, while 86% reported reduced ongoing costs. This gives vendors a clear value message for manufacturers, logistics firms, energy companies, and transport operators.

AI-enabled industrial applications are expanding. About 94% of surveyed industrial enterprises had deployed on-premise edge with private wireless, and 70% used it to support AI-driven applications such as predictive maintenance and real-time monitoring.

5G network slicing creates new revenue opportunities for telecom-linked Edge AI services. Commercial 5G standalone network slicing offerings increased from 65 to 84 within six months, supporting premium services for smart factories, ports, warehouses, utilities, and public safety networks.

Financial Impact

Edge AI can reduce long-term operating costs by processing data locally instead of sending all data to the cloud. This is important for video analytics, robotics, smart cameras, autonomous equipment, and IoT systems, where high data transfer costs and latency can affect business performance.

Cybersecurity-led Edge AI can also reduce financial exposure. IBM reported the global average data breach cost at USD 4.4 million in 2025, while extensive use of AI in security was linked with USD 1.9 million in cost savings compared with organizations that did not use these solutions.

Vendor revenue quality can improve when hardware sales are combined with software, monitoring, cybersecurity, model updates, and maintenance contracts. This supports recurring revenue instead of relying only on one-time device sales.

By Component

Hardware led the Edge AI Market with a 56.8% share, supported by rising demand for AI chips, processors, sensors, cameras, accelerators, and embedded modules that can process data directly on devices. The segment is growing because enterprises and device makers need faster decision-making, lower latency, reduced cloud dependency, and improved data privacy at the edge.

Hardware adoption is especially strong in smartphones, smart cameras, vehicles, robotics, industrial machines, and connected consumer devices. The need for real-time AI processing in image recognition, voice control, predictive maintenance, and autonomous systems continues to support strong demand for edge AI hardware.

By Device Type

Smartphones accounted for the leading share of 34.6% in the Edge AI Market, driven by the growing use of on-device AI for cameras, voice assistants, translation, personalization, security, and battery optimization. Smartphone brands are increasingly adding AI processors and neural processing units to improve user experience without sending every task to the cloud.

The segment is also supported by rising demand for generative AI features, real-time photo enhancement, biometric authentication, and offline AI functions. As consumers expect faster and more private digital experiences, smartphones remain one of the most important devices for edge AI deployment.

By Deployment

On-premises deployment held the largest share at 58.4%, mainly due to the need for stronger data control, faster response time, and secure processing within enterprise environments. Many industries prefer on-premises edge AI because sensitive data from cameras, machines, sensors, and connected devices can be processed locally without depending fully on external cloud systems.

This deployment model is widely used in manufacturing, healthcare, banking, retail, automotive, and defense-related applications where privacy, compliance, and real-time operations are critical. On-premises edge AI also helps reduce network load, lower data transfer costs, and support continuous operations even when cloud connectivity is limited.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Technology

Machine learning led the technology segment with a 39.7% share, supported by its wide use in predictive analytics, object detection, speech recognition, anomaly detection, quality inspection, and automated decision-making. Machine learning models are increasingly being optimized to run on edge devices, allowing faster insights close to where data is generated.

The segment benefits from growing use across consumer electronics, industrial automation, smart cities, healthcare devices, and connected vehicles. Machine learning remains central to edge AI because it enables devices to learn from patterns, improve performance, and support intelligent actions without constant cloud processing.

By End-Use Industry

Consumer electronics accounted for 27.9% share, making it the leading end-use industry in the Edge AI Market. Demand is being supported by rapid adoption of AI-enabled smartphones, smart speakers, wearables, laptops, home cameras, televisions, and connected appliances.

The growth of this segment is driven by rising consumer preference for personalized, responsive, and privacy-focused devices. Edge AI allows consumer products to deliver faster voice commands, better image processing, health tracking, gesture control, and smart home automation while reducing reliance on cloud-based processing.

By Region

North America led the Edge AI Market with a 38.6% share, supported by strong AI infrastructure, advanced semiconductor development, high adoption of connected devices, and early use of edge computing across enterprises. The region has strong demand from consumer electronics, automotive, healthcare, industrial automation, retail, and defense applications.

The growth of North America is further supported by investments in AI chips, 5G networks, smart factories, autonomous systems, and cloud-edge platforms. The United States remains a key contributor due to its strong technology ecosystem, presence of major AI hardware and software companies, and rapid enterprise adoption of real-time intelligent systems.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRisk Factors & Market Barriers

Regulatory & Compliance Risks

AI regulation is becoming stricter. The EU AI Act entered into force on August 1, 2024, and full application is set for August 2, 2026, with high-risk rules for certain systems applying later. This increases compliance work for Edge AI used in biometrics, critical infrastructure, healthcare, transport, and safety systems.

Non-compliance can create major financial risk. Under the EU AI Act, prohibited AI practice violations can lead to fines of up to EUR 35 million or 7% of worldwide annual turnover, while other key obligations can carry fines up to EUR 15 million or 3% of turnover.

AI governance gaps can affect enterprise trust. IBM reported that 63% of organizations lacked AI governance policies, and 97% of organizations with an AI-related security incident lacked proper AI access controls. This makes compliance, access control, and auditability important buying criteria for Edge AI platforms.

Market Adoption Barriers

Skills shortages remain a major barrier. IBM found that limited AI skills and expertise affected 33% of companies, data complexity affected 25%, and ethical concerns affected 23% of companies exploring or deploying AI. These barriers can slow Edge AI adoption because deployments require AI engineers, embedded systems expertise, cybersecurity teams, and integration support.

Adoption is still uneven across business sizes. In U.S. Census data, less than 20% of firms with four or fewer employees reported using AI, compared with 37% among firms with at least 250 employees. This indicates that smaller customers may need lower-cost, packaged Edge AI solutions before adoption becomes widespread.

Security concerns can delay purchasing decisions. IBM reported a USD 4.4 million global average cost of a data breach in 2025, which makes buyers cautious about deploying AI at the edge without strong encryption, device identity, access control, monitoring, and incident response.

Key Market Segment

By Component

Hardware

Software

Services

By Device Type

Smartphones

Cameras

Robots

Wearables

Smart Sensors

Others

By Deployment

On-Premises

Cloud-Based

Hybrid

By Technology

Machine Learning

Computer Vision

Natural Language Processing

Generative AI

Others

By End-Use Industry

Consumer Electronics

Automotive

Manufacturing

Healthcare

Retail

BFSI

Others

By Region

North America

Europe

Asia Pacific

Latin America

Middle East and Africa

Driver Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for real-time AI processing | +3.8% | North America, Europe, Asia Pacific | Increases adoption in smart devices, vehicles, cameras, and industrial systems. |

Growth of connected devices and IoT networks | +3.4% | Asia Pacific, North America, Europe | Expands demand for local data processing and low-latency intelligence. |

Increasing need for data privacy and security | +2.9% | Europe, North America, Japan | Supports on-device AI as sensitive data can be processed locally. |

Wider use of AI in consumer electronics | +2.7% | China, South Korea, Japan, U.S. | Drives demand through smartphones, wearables, smart home devices, and cameras. |

Expansion of industrial automation and smart manufacturing | +2.4% | Germany, China, U.S., Japan | Strengthens use in predictive maintenance, quality inspection, robotics, and process control. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High cost of AI chips and edge hardware | -2.6% | Asia Pacific, Latin America, Middle East and Africa | Slows adoption among price-sensitive manufacturers and smaller enterprises. |

Limited processing power in small edge devices | -2.2% | Global | Restricts deployment of advanced AI models on low-power devices. |

Integration complexity with existing systems | -2.0% | North America, Europe, Asia Pacific | Increases deployment time and technical cost. |

Shortage of skilled edge AI developers | -1.8% | India, Southeast Asia, Latin America, Africa | Limits large-scale implementation across enterprises. |

Cybersecurity risks at distributed endpoints | -1.6% | Global | Raises concerns over device-level attacks and data protection. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth of AI-enabled smartphones and wearables | +3.5% | China, India, South Korea, U.S. | Creates high-volume demand for edge AI processors and software. |

Rising adoption in autonomous and connected vehicles | +3.2% | U.S., Germany, China, Japan | Supports use in driver assistance, in-cabin monitoring, navigation, and safety systems. |

Expansion of smart cities and surveillance systems | +2.8% | Asia Pacific, Middle East, Europe | Increases use of edge AI cameras, sensors, and traffic systems. |

Healthcare adoption of edge-based diagnostics | +2.5% | North America, Europe, Japan, India | Enables faster imaging, monitoring, and patient-care decisions near the point of use. |

Development of energy-efficient AI models | +2.3% | Global | Improves adoption in battery-powered and low-power devices. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Balancing AI accuracy with low power use | -2.4% | Global | Creates design challenges for compact and battery-based devices. |

Fragmented hardware and software ecosystem | -2.1% | North America, Europe, Asia Pacific | Makes deployment less uniform across platforms and industries. |

Data governance and compliance pressure | -1.9% | Europe, North America, Asia Pacific | Increases documentation, testing, and compliance burden. |

Model update and maintenance complexity | -1.7% | Global | Adds long-term operating cost for deployed edge systems. |

Competition from cloud-based AI processing | -1.5% | Global | Limits edge AI use where latency and privacy needs are lower. |

Recent Development

Advanced Micro Devices, Inc., March 2026 - AMD expanded its Ryzen AI Embedded P100 Series for edge AI applications, offering up to 80 TOPS and ROCm support for industrial, robotics, and embedded AI systems. The launch strengthened AMD’s position in low-power edge inference, computer-on-modules, single-board computers, and intelligent systems.

Google LLC, April 2026 - Google updated its Gemini Nano developer documentation for Android on-device AI, highlighting that Gemini Nano runs through Android’s AICore system service. The model uses device hardware to support low-latency inference, enabling AI features to run locally on compatible Android devices.

Samsung Electronics Co., Ltd., March 2025 - Samsung showcased its mobile AI strategy at MWC 2025, covering Galaxy AI, the Galaxy S25 series, new Galaxy A devices, software-centric networks, and Project Moohan. The company positioned on-device AI as a core feature across smartphones, tablets, wearables, and connected devices, with Galaxy AI supported from the S24 series onward.

Cisco Systems, Inc., January 2025 - Cisco launched AI Defense to help enterprises secure AI applications across development, deployment, and runtime environments. The solution supports the broader edge AI market by addressing model safety, visibility, validation, and protection risks as AI workloads move closer to enterprise networks and connected devices.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 27.9 Bn |

Forecast Revenue (2035) | USD 356 Bn |

CAGR (2025-2035) | 29% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI market impact analysis, market surveys, trade analysis, Industry & competitive intelligence, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends, Strategic Consultation & Advisory Services |

Segments Covered | By Component (Hardware, Software, Services), By Device Type (Smartphones, Cameras, Robots, Wearables, Smart Sensors, Others), By Deployment (On-Premises, Cloud-Based, Hybrid), By Technology (Machine Learning, Computer Vision, Natural Language Processing, Generative AI, Others), By End-Use Industry (Consumer Electronics, Automotive, Manufacturing, Healthcare, Retail, BFSI, Others), By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), By Regional Insights, Business plan and and project report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035. |

Regional Analysis | North America - US, Canada; Europe - Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific - China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America - Brazil, Mexico, Rest of Latin America; Middle East & Africa - South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc., Qualcomm Incorporated, Microsoft Corporation, Amazon Web Services, Inc., Google LLC, IBM Corporation, Cisco Systems, Inc., Samsung Electronics Co., Ltd. |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Qualcomm Incorporated

Microsoft Corporation

Amazon Web Services, Inc.

Google LLC

IBM Corporation

Cisco Systems, Inc.

Samsung Electronics Co., Ltd.

Other Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Sayali brings more than 5 years of experience to Globe Market Research, supporting the accuracy, clarity, and relevance of research content across multiple industries. She reviews market data, segment analysis, competitive insights, and industry trends to ensure each report meets strong quality standards and provides practical value to business decision-makers. Her expertise spans healthcare, information technology, consumer goods, and diverse cross-industry domains. With a strong focus on data reliability, structured analysis, and clear presentation, Sayali helps ensure that each research output delivers well-reviewed insights for clients, investors, consultants, and industry stakeholders.

Frequently Asked Questions

Related Reports

More in Information and Technology

5G RAN Market Size to hit USD 108.5 billion by 2035

Global 5G RAN Market Size, Go-to-Market and Sales Strategy Analysis By Component (Hardware, Software, Services), By Architecture Type (Traditional RAN, Open RAN), By Deployment (Public Networks, Private Networks), By End Use (Telecom Operators, Enterprise and Industrial Users), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Online Dating Market Size to hit USD 29.5 Bn by 2035

Global Online Dating Market Size, Go-to-Market Strategy Analysis By Type (Paying Online Dating, Non-Paying Online Dating), By Revenue Model (Subscription, Advertising-Supported, Other Model), By Platform (Web Portals, Applications), By Age Group (Adult, Baby Boomer, Generation X, Generation Z, Millennials), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

AI In Interior Design Market Size to hit USD 37.7 billion by 2035

Global AI In Interior Design Market Size, Go-to-Market Strategy Analysis By Component (Solution, Service), By Deployment (Cloud, On-Premises), By User Type (Homeowners, Real Estate Developers, Interior Designers, Architects, Corporate Clients), By Design Style (Traditional, Modern, Contemporary, Minimalist, Eclectic), By Technology Integration (3D Visualization Tools, Virtual Reality Solutions, Augmented Reality Applications, CAD Software, Machine Learning Algorithms), By Application (Residential Design, Commercial Design, Hospitality Design, Retail Spaces, Office Spaces), By Pricing Strategy (Subscription-Based, Freemium Model, Pay-Per-Use, One-Time License, Enterprise Licensing, Project-Based Pricing), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Facility Management Market Size to hit USD 4.3 Trillion by 2035

Global Facility Management Market Size, Go-to-Market Strategy Analysis By Service Type (Hard Services, Soft Services), By Offering (In-House, Outsourced), By End User (Commercial, Industrial, Government and Public Sector, Residential, Institutional, Others), By Service Provider (Single Service Providers, Integrated Facility Management Providers, Bundled Service Providers), By Contract Type (Annual Contracts, Flexible Contracts, Performance-Based Contracts), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035