Market Size and Growth Forecast

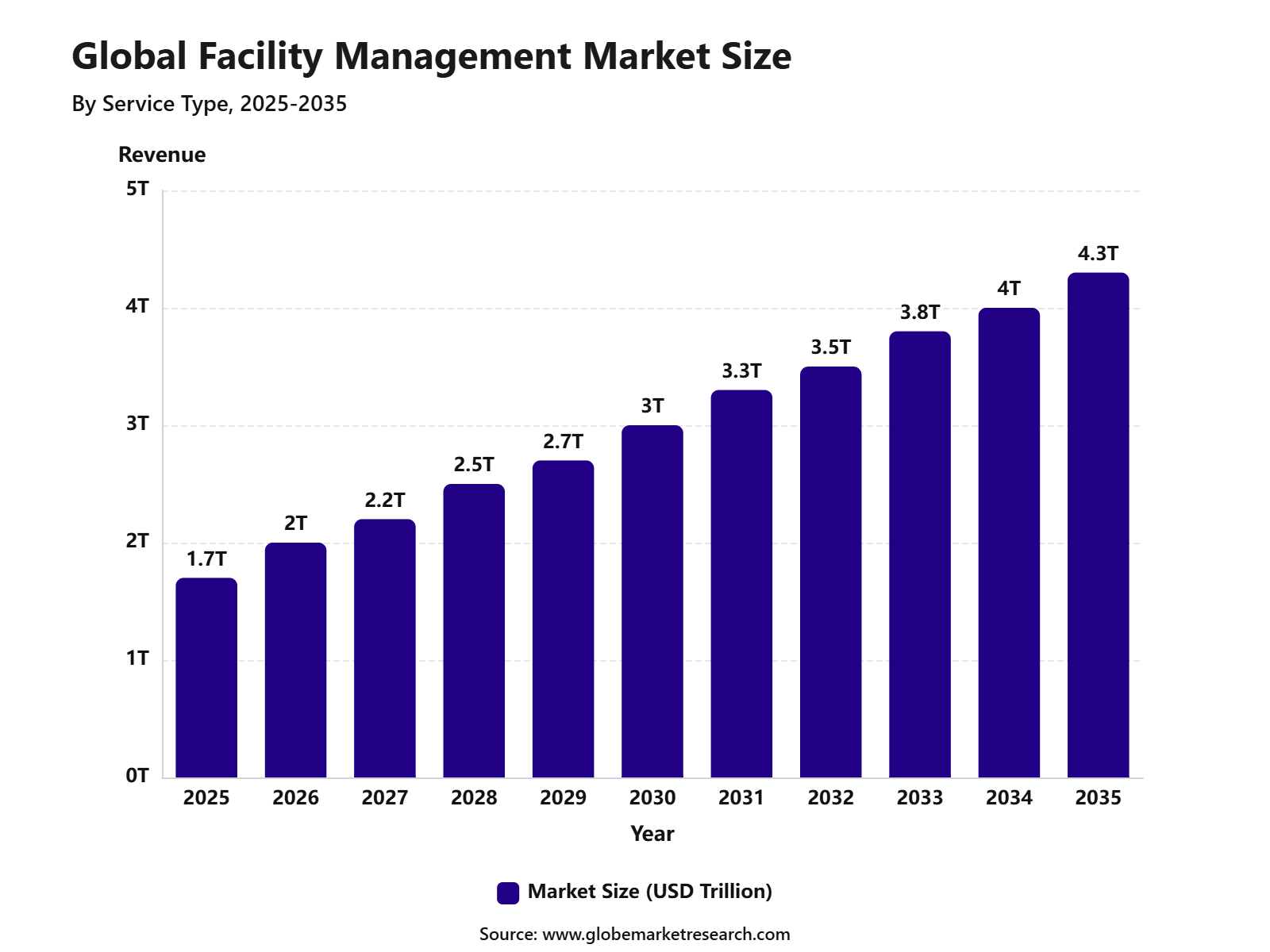

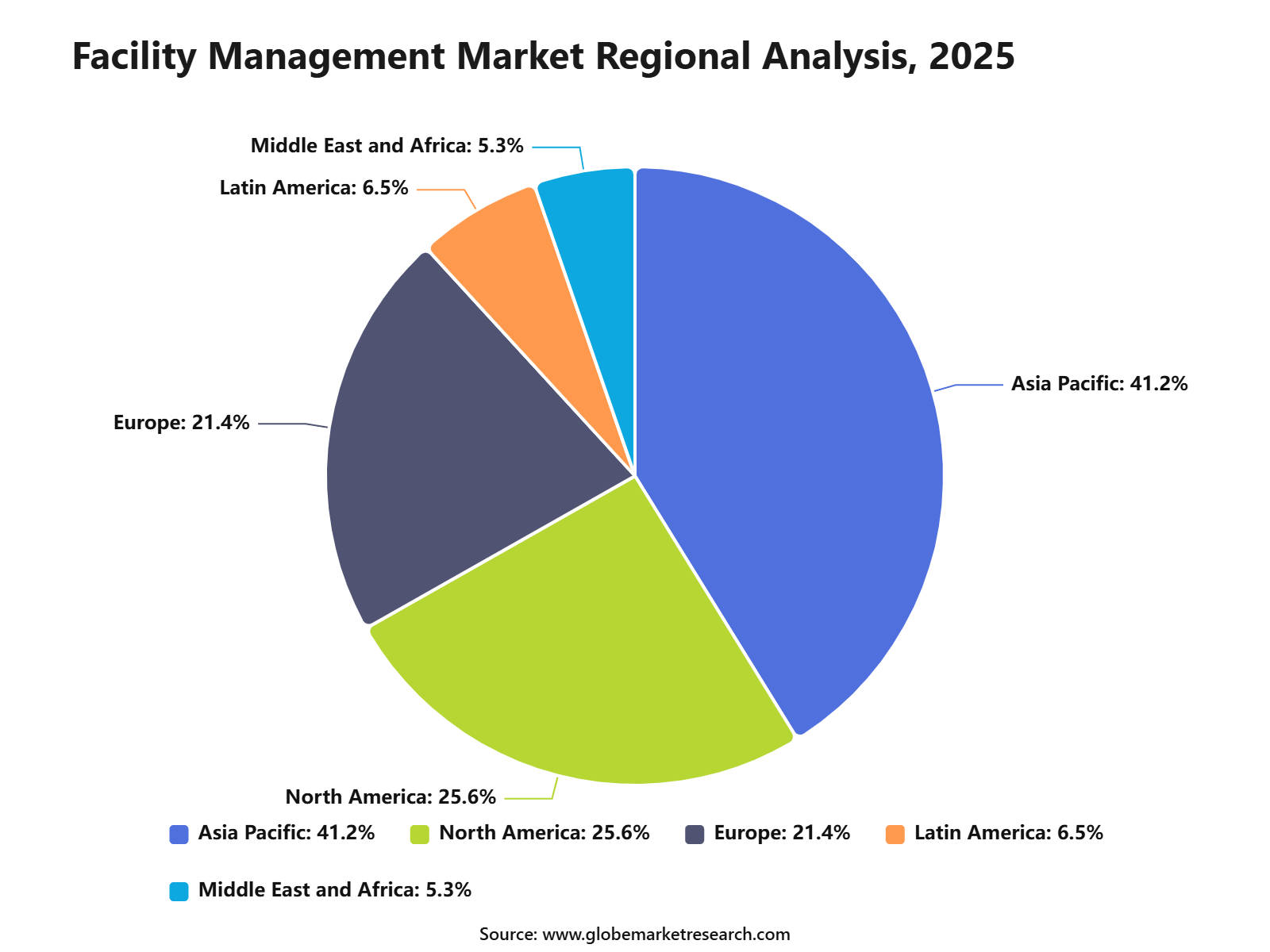

According to Globe Market Research, the global facility management market was worth USD 1.7 trillion in 2025 and is expected to reach USD 4.3 trillion by 2035, growing at a 9.5% CAGR. Asia Pacific led the market with 41.2% share in 2025, supported by urban development, commercial infrastructure expansion, industrial activity, and growing demand for organized facility services across offices, factories, hospitals, airports, retail spaces, and smart buildings.

Key Parameter | Report Details |

|---|---|

Market Revenue, 2025 | USD 1,700 Billion |

Projected Revenue, 2035 | USD 4,300 Billion |

CAGR, 2025-2035 | 9.5% |

Largest Region | Asia Pacific, 41.2% Share |

Market Concentration | Medium |

Base Year | 2025 |

Forecast Period | 2025-2035 |

Facility management includes the services used to manage buildings, workplaces, assets, equipment, safety systems, cleaning, maintenance, energy use, space planning, and daily site operations. These services are usually divided into hard services such as HVAC, electrical, plumbing, fire safety, and repairs, and soft services such as cleaning, security, catering, landscaping, waste management, and workplace support.

The market is becoming more strategic because buildings are no longer being managed only for basic maintenance. Clients are now looking for cost savings, asset performance, workplace safety, energy efficiency, compliance, sustainability reporting, and digital building visibility. This shift is making facility management an important operating function for commercial real estate, industrial plants, healthcare buildings, airports, data centers, educational campuses, and public infrastructure.

Why is Facility Management Market Growing?

The growth of the facility management market can be attributed to rising demand for professional building operations, outsourced services, technical maintenance, energy management, and workplace support. Organizations are under pressure to reduce operating costs while improving building uptime, safety, employee experience, and asset life. This is increasing demand for structured facility management contracts instead of fragmented vendor-based service models.

The global facilities management industry is also moving toward larger managed service models. Total FM spending is projected to surpass USD 3 trillion by 2026, while 84% of FM leaders identified escalating operating costs and budget constraints as their top concern. This shows that cost control is now one of the strongest reasons companies are reviewing their facility management strategy.

Public and institutional infrastructure is also creating recurring service demand. In May 2026, U.S. public construction spending reached a seasonally adjusted annual rate of USD 541.2 billion, while educational construction stood at USD 113.4 billion. These assets require ongoing cleaning, maintenance, safety checks, energy management, and lifecycle upgrades, creating stable demand for facility management providers.

Hard Services Remain the Leading Service Type

Hard services led the facility management market with 55.1% share in 2025. These services include HVAC maintenance, electrical systems, plumbing, fire safety, elevators, building repairs, mechanical systems, and energy infrastructure. Their leadership is supported by the essential role these services play in keeping buildings safe, compliant, and operational. Demand for hard services is rising because commercial buildings, hospitals, factories, airports, logistics facilities, and data centers cannot afford technical failures.

A breakdown in HVAC, power, plumbing, or safety systems can directly affect business continuity, tenant satisfaction, worker safety, and regulatory compliance. The segment is also gaining importance as clients shift from reactive repair to preventive maintenance. Planned inspection, condition monitoring, and asset lifecycle management help reduce downtime and emergency repair costs. This makes hard services a high-priority area for facility managers and building owners.

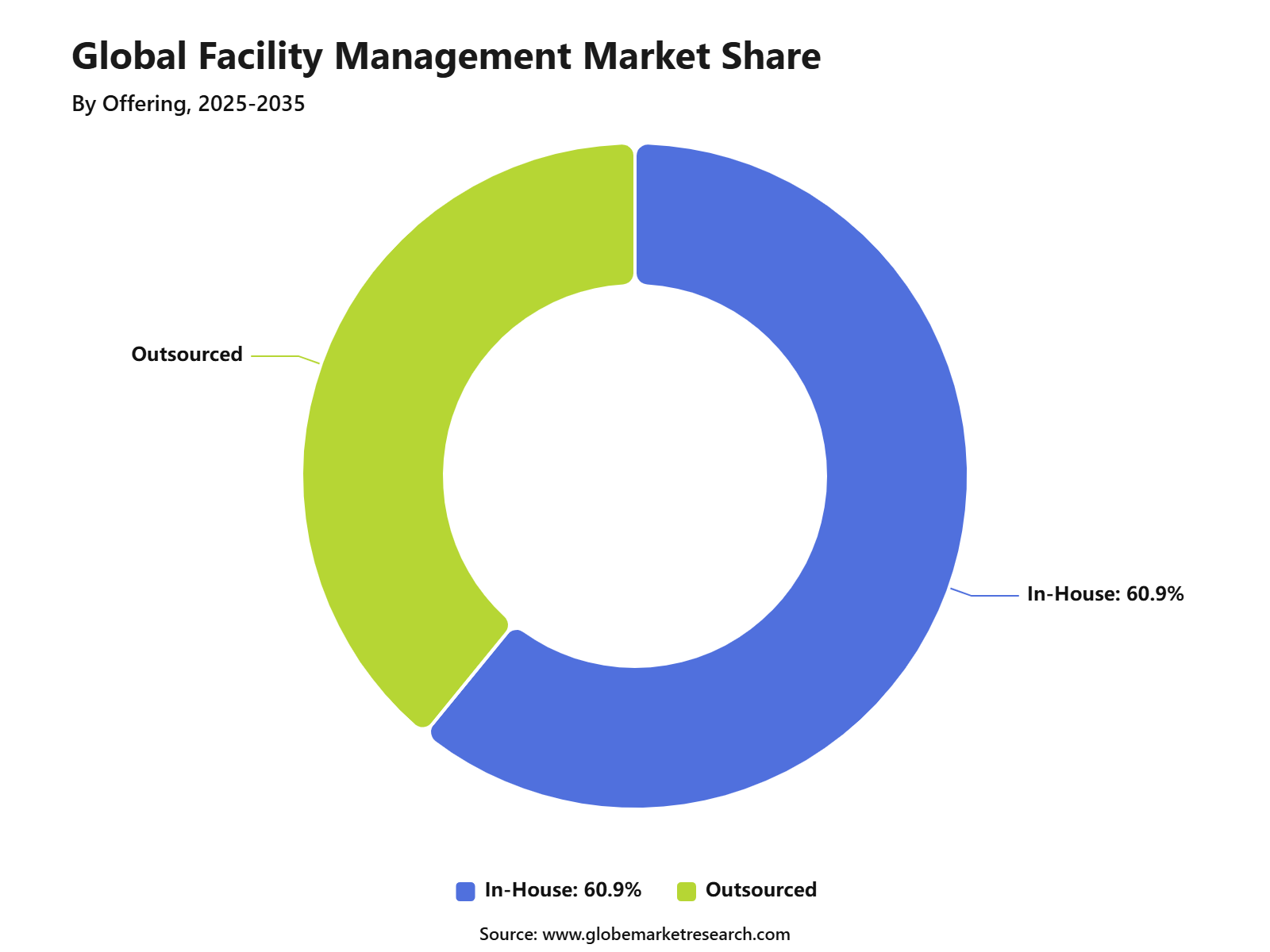

In-House Facility Management Holds the Leading Offering Share

In-house facility management accounted for 60.9% share in 2025, supported by direct operational control, faster response time, internal workforce supervision, and stronger alignment with business needs. Many organizations still prefer in-house teams for sensitive, large, or mission-critical facilities. The in-house model is especially relevant in healthcare, manufacturing, government facilities, corporate campuses, and high-security environments.

These facilities often need close control over staff access, compliance procedures, emergency response, maintenance schedules, and service quality. However, outsourced and integrated models are gaining attention where cost control, service scalability, technology adoption, and multi-site consistency are important. This means the future market is likely to include both in-house control and selective outsourcing based on operational need.

Commercial Facilities Are the Largest End-User Segment

Commercial facilities held 35.8% share of the facility management market in 2025. This includes offices, retail spaces, malls, hospitality properties, mixed-use buildings, business parks, and corporate real estate portfolios. These facilities need continuous cleaning, maintenance, security, energy management, and workplace support services.

The commercial segment is strongly linked with tenant experience and property value. Clean, safe, efficient, and well-maintained buildings can improve occupancy, employee comfort, brand image, and visitor satisfaction. This makes facility management important for both property owners and corporate occupiers.

Commercial buildings are also becoming more technology-enabled. Facility teams are using digital work orders, sensors, asset tracking, energy dashboards, and occupancy tools to improve service response and reduce operating waste. This supports demand for smart facility management solutions.

Integrated Facility Management Providers Are Gaining Preference

Integrated facility management providers led the service provider segment with 43.4% share in 2025. This model brings multiple services such as cleaning, security, maintenance, energy support, workplace services, vendor coordination, and reporting under one managed structure. The growth of this segment can be attributed to demand for simpler vendor management and clearer accountability.

Instead of managing many separate contractors, clients can work with one provider that offers centralized reporting, service-level agreements, and coordinated delivery across multiple sites. Integrated facility management also supports better cost control. Contract consolidation can reduce service duplication, improve staffing efficiency, standardize processes, and create stronger operational visibility. This is why large enterprises, real estate portfolios, hospitals, universities, and industrial operators are increasingly reviewing integrated service models.

Annual Contracts Support Stable Service Planning

Annual contracts accounted for 58.7% share of the facility management market in 2025. Buildings require recurring cleaning, maintenance, safety checks, repairs, and support services throughout the year, making annual agreements practical for both clients and providers. Annual contracts help clients plan budgets, define service levels, set response times, and maintain stable operating coverage.

They also reduce the need for repeated short-term procurement, which can create service gaps and inconsistent quality. For providers, annual contracts support workforce planning, equipment allocation, route scheduling, and vendor coordination. This improves service continuity and allows facility managers to focus on long-term building performance instead of only short-term issue handling.

AI and Digital Tools Are Changing Facility Management

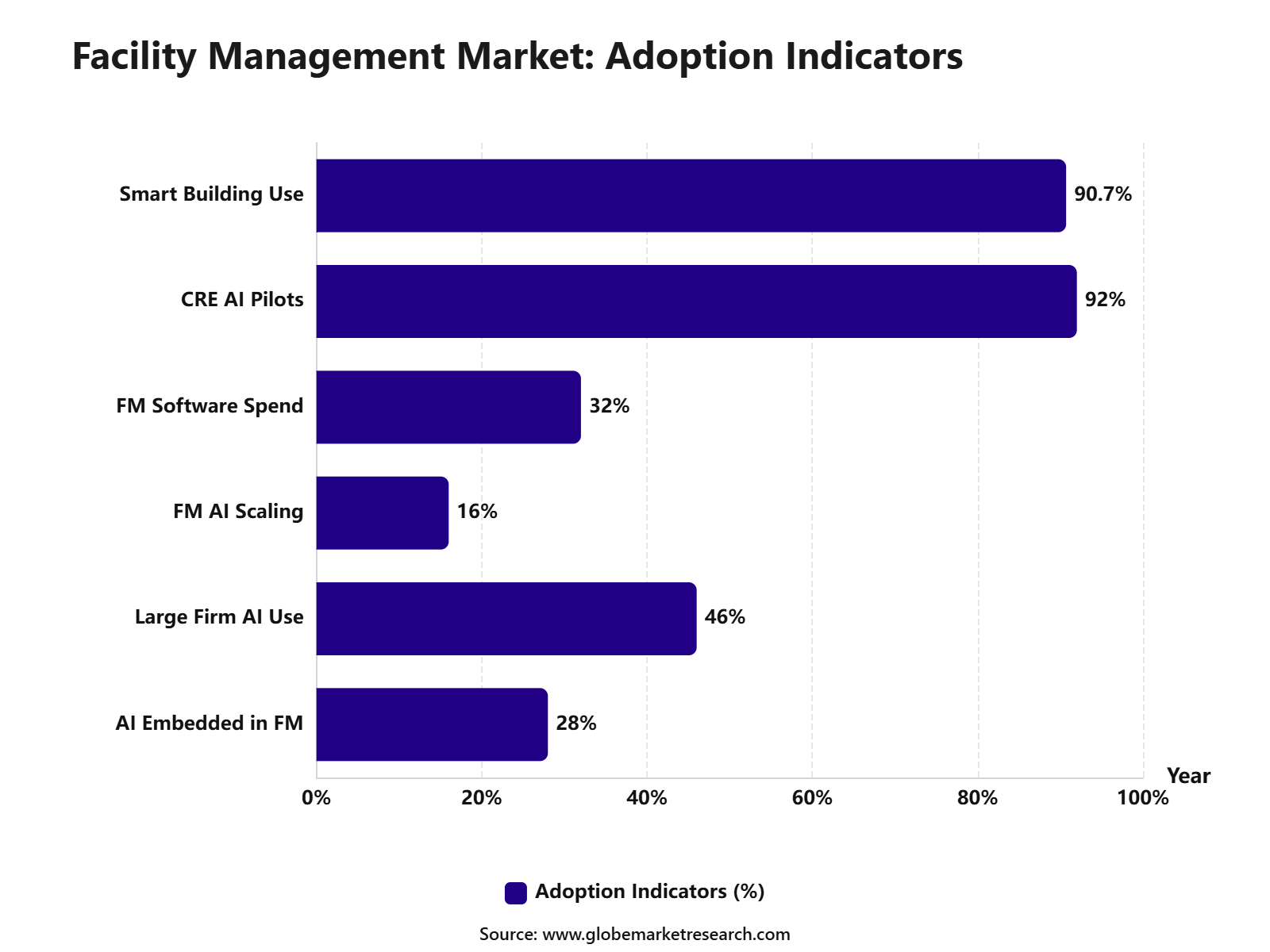

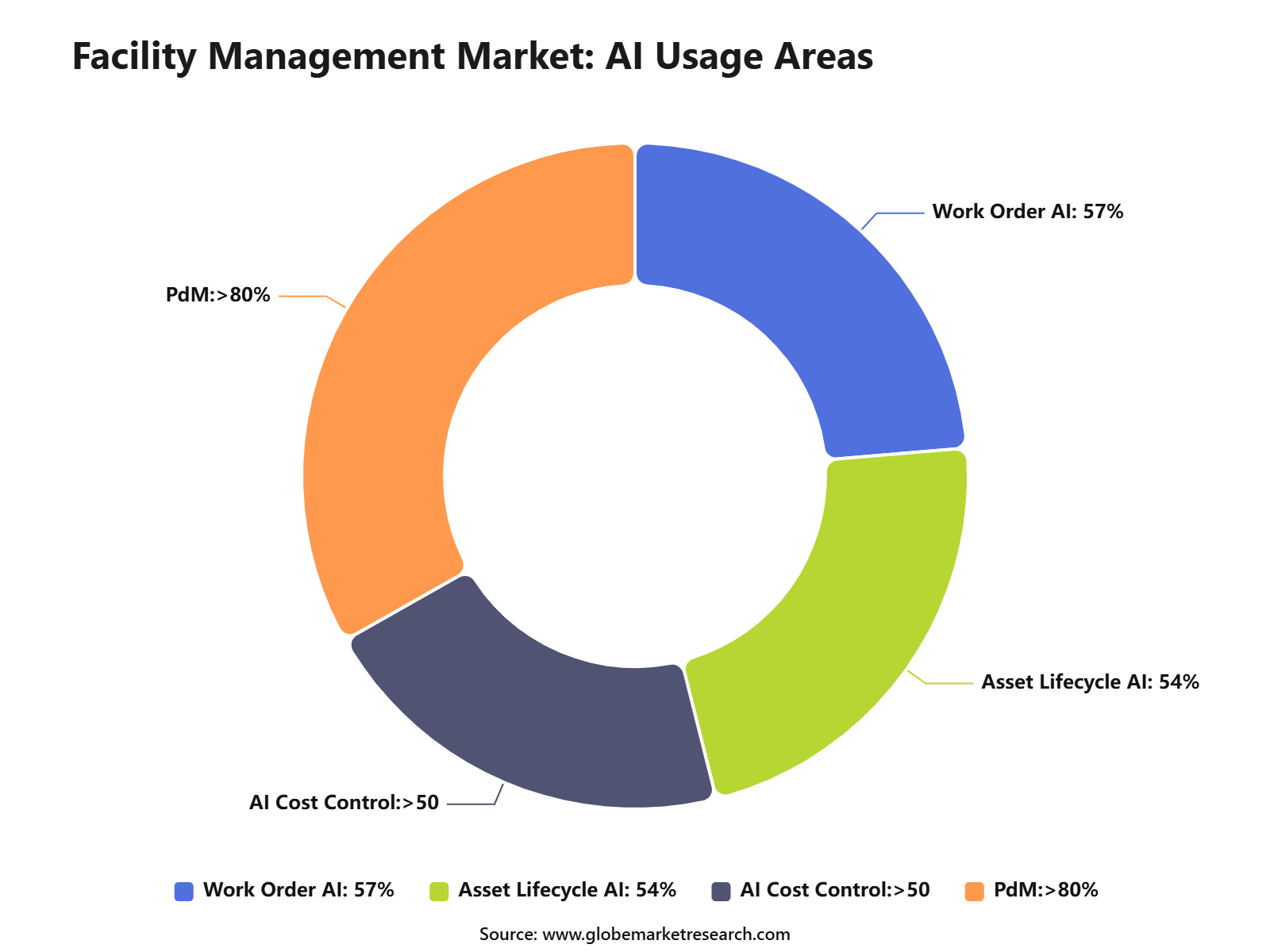

AI is becoming a practical tool in facility management. In a 2026 survey, 65% of business leaders and 67% of facility managers said their organizations already use AI to improve facility operation, utilization, and maintenance. Another 65% of business leaders and 61% of facility managers said they plan to implement or expand AI tools over the next year. AI is being used in predictive maintenance, energy optimization, work order automation, cleaning schedules, space utilization, security monitoring, and asset performance tracking.

Predictive maintenance is especially important because it helps identify early warning signs before equipment failure occurs. Technology spending is also becoming more focused. The report data shows that 32% of organizations plan to increase FM software investment, while work order management leads software priorities at 57%. This indicates that facility management is moving from manual coordination to data-based building operations.

Energy Efficiency Is Becoming a Core FM Priority

Energy management is one of the most important facility management trends. Buildings account for around 30% of global energy demand and have contributed around 20% of the growth in total energy demand since 2019. Commercial and public buildings represent around 30% of total building energy demand, making energy efficiency a major area of focus for facility managers. Facility managers can reduce energy waste through HVAC optimization, lighting control, equipment scheduling, building automation, smart sensors, and occupancy-based operations.

These actions can lower utility costs while improving comfort and operational performance. Energy efficiency is also linked with sustainability reporting and compliance. As more companies set carbon reduction targets, facility management providers are expected to support energy audits, asset monitoring, maintenance planning, and performance reporting.

Asia Pacific Leads the Facility Management Market

Asia Pacific led the facility management market with 41.2% share in 2025. The region is supported by rapid urban development, commercial construction, industrial expansion, smart building adoption, and rising demand for professional facility services. China, India, Japan, Singapore, Australia, and Southeast Asia remain important markets for commercial and industrial facility operations.

The regional opportunity is strong because buildings are becoming larger, more complex, and more service-intensive. Offices, transport hubs, factories, logistics parks, hospitals, malls, and residential complexes require structured maintenance, cleaning, safety, security, and energy services. North America and Europe remain mature markets with higher adoption of outsourcing, smart buildings, compliance-led operations, and sustainability services. The Middle East is also gaining importance through large investments in hospitality, airports, healthcare, public infrastructure, and commercial real estate.

Analyst Perspective

What the Data Is Telling Facility Management Companies?

From an analyst perspective, the data shows that facility management is shifting from basic service delivery to performance-led building operations. A market value of USD 1.7 trillion in 2025 and a projected value of USD 4.3 trillion by 2035 indicate strong long-term demand, but future growth will favor providers that can prove cost savings, service quality, and technical capability.

The strongest signal is the rise of hard services, integrated providers, and annual contracts. Hard services held 55.1% share, integrated facility management providers captured 43.4% share, and annual contracts accounted for 58.7% share, showing that clients want reliable, structured, and accountable facility operations.

What Opportunities Are Emerging?

The biggest opportunity is in integrated facility management and smart building services. Clients are looking for one accountable provider that can manage maintenance, cleaning, security, energy use, compliance, and reporting through a coordinated service model. Predictive maintenance and energy management are also strong opportunities.

Buildings account for around 30% of global energy demand, which makes energy optimization a practical financial and sustainability priority for building owners and occupiers. Data centers, healthcare facilities, airports, industrial sites, and commercial campuses are attractive high-value segments. These facilities require technical support, fast response, strong compliance, and continuous uptime, which can support larger and more stable contracts.

What Risks Should Companies Be Aware Of?

The biggest risk is margin pressure caused by labor dependency, rising wages, and service price competition. Facility management providers must manage workforce productivity carefully because many services still depend on trained technicians, cleaners, security staff, and site supervisors.

Service inconsistency is another risk. Multi-site clients expect the same quality, reporting, safety standards, and response time across all locations. Providers that cannot standardize delivery may face contract loss or lower renewal rates.

Technology risk is also rising. Smart buildings create operational benefits, but they also introduce cybersecurity, integration, and data management challenges. Providers must strengthen digital skills and security controls before scaling connected facility services.

What Decisions Should Clients Make Next?

Clients should first decide whether they need in-house control, outsourced support, or an integrated facility management model. The right choice should depend on facility complexity, security needs, cost pressure, service quality, and internal workforce capability.

Second, clients should prioritize energy efficiency and predictive maintenance. These areas can reduce downtime, improve asset life, and support sustainability goals while giving measurable financial benefits.

Finally, clients should select providers based on service consistency, technical skill, digital reporting, compliance strength, and cost transparency. The best facility management partners will be those that can move beyond basic tasks and help improve building performance.

Competitive Landscape

The facility management market is competitive, with established global providers, regional service companies, technical maintenance specialists, workplace service providers, and integrated facility management firms operating across the market. Key companies include CBRE Group, Sodexo, Compass Group, ISS, Johnson Controls, Dussmann Group, JLL, Cushman & Wakefield, Aramark, Mitie Group, EMCOR Group, ENGIE, and Veolia.

Competition is expected to increase as clients demand larger service bundles, better digital reporting, stronger sustainability support, and measurable cost savings. Providers that rely only on basic labor-led services may face pricing pressure, while providers with technical depth and technology capability are likely to be better positioned.

Recent activity also shows that facility management is expanding into more specialized areas. In May 2026, Mitie secured a GBP 27 million, three-year NHS facilities management contract, while Cushman & Wakefield reported USD 2.5 billion in first-quarter 2026 revenue, up 11% year over year, with services revenue supported by facilities management and project management demand.

Recent Developments

Market News

In February 2026, Facilio launched Facilio Atom, an autonomous AI agent suite for facilities management. The platform is designed to automate helpdesk dispatch, compliance workflows, invoice validation, approvals, and reporting, reducing repetitive manual work by up to 40%.

In April 2026, CBRE reported strong momentum in facilities management, with facilities management revenue rising 17%, or 13% in local currency, during Q1 2026. Growth was supported by local facilities management, enterprise FM, technology clients, industrial users, and life sciences customers.

In May 2026, ISS extended its partnership with Deutsche Telekom until the end of 2035. This extension is important because long-term integrated facility services contracts are becoming a key part of revenue stability for large FM providers.

Funding

In February 2025, 75F raised USD 45.1 million in Series B funding led by Accurant International’s Net Zero Alliance, with participation from Carrier Global, Climate Investment, Breakthrough Energy Ventures, Next47, and WIND Ventures. The funding supports AI-driven HVAC automation and energy efficiency solutions for commercial buildings.

In July 2025, MaintainX raised USD 150.1 million in Series D funding to expand AI-powered maintenance, asset management, machine health monitoring, predictive maintenance, and enterprise asset management capabilities. The company said the round took its total funding to USD 254.1 million and valuation to USD 2.5 billion.

In September 2025, Joblogic received a strategic growth investment from Vista Equity Partners, including more than GBP 100.1 million in new primary capital. The investment is focused on AI-led field service management, European expansion, and computer-aided facility management capabilities

Mergers and Acquisitions

In February 2026, SILA acquired a 100% stake in SMS Integrated Facility Services from Samara Capital for INR 270 crore. The acquisition expanded SILA’s facility management footprint across India and strengthened its position in organized business services.

In March 2026, Cintas announced a USD 5.5 billion cash-and-stock deal to acquire UniFirst. The deal is a major consolidation move in North American workwear, uniform rental, cleaning, first-aid, and facility services.

In May 2026, ISS signed an agreement to acquire Tomagruppen, a facility services company operating mainly in Norway and Denmark. Tomagruppen generated about DKK 1.8 billion in 2025 revenue and adds more than 4,000 employees to ISS.

Conclusion

The facility management market is entering a more technology-enabled and performance-driven phase. Growth is being supported by hard services, integrated facility management, annual contracts, smart buildings, energy efficiency, predictive maintenance, and rising demand from commercial, industrial, healthcare, education, public infrastructure, and data center facilities.

Future growth will be led by providers that can combine reliable service delivery with digital tools, skilled technicians, energy management, compliance support, and measurable cost savings. Clients are expected to prioritize facility management partners that improve asset performance, reduce operational risk, and create safer, more efficient buildings.